Picture supply: Getty Photographs

The FTSE 100 rose by round 20% in 2025, its finest 12 months since 2009. A lot of the heavy lifting got here from sturdy performances by treasured metals producers, banks and different monetary shares. With the index having hit the ten,000 mark for some time – and dividend yields falling – traders would possibly fairly wonder if the perfect alternatives have already handed. Nevertheless, I nonetheless see bargains, even amongst shares which have rallied exhausting lately.

Risky inventory

After hitting a three-year low in April, Glencore (LSE: GLEN) has loved a robust rebound, greater than doubling from its lows. But regardless of that rally, the shares rose solely 14% over 2025, leaving the miner properly behind most of the index’s greatest winners.

One cause for that cautious pricing is the lingering concentrate on volatility. Glencore’s earnings have swung sharply with commodity costs for years, and the market seems to imagine that may proceed.

However that framing misses an vital structural level: the corporate’s earnings and money flows have built-in working leverage. In different phrases, the enterprise can profit disproportionately from even modest stabilisation in commodity markets – and we could already be seeing that take form.

Copper costs

Take copper, for instance. The purple steel has loved a powerful run, climbing roughly 40% over the previous 12 months. That rally is being supported on each the demand and provide aspect.

Demand is coming from a number of sources, together with electrification, renewable vitality, industrial exercise and the AI data-centre build-out.

In the meantime, provide stays constrained. Main producing nations reminiscent of Chile have seen flat output, whereas ore grades proceed to say no over time.

Layer on prime of that uncertainty round tariff coverage, international locations stockpiling metals and the specter of export bans, and a potent combine is forming beneath the floor.

However right here’s the important thing level: copper costs don’t have to go parabolic for the miner’s money flows to enhance meaningfully. Value stability, mixed with regular volumes and disciplined price management, could be sufficient to shift the earnings outlook from contraction to growth.

Market mispricing

Crucially, that’s not how the market seems to be pricing Glencore immediately. Many traders proceed to imagine that extended weak spot in coal will swamp any metals upside, leaving earnings range-bound or worse. Because of this, expectations stay muted, whilst share costs get better.

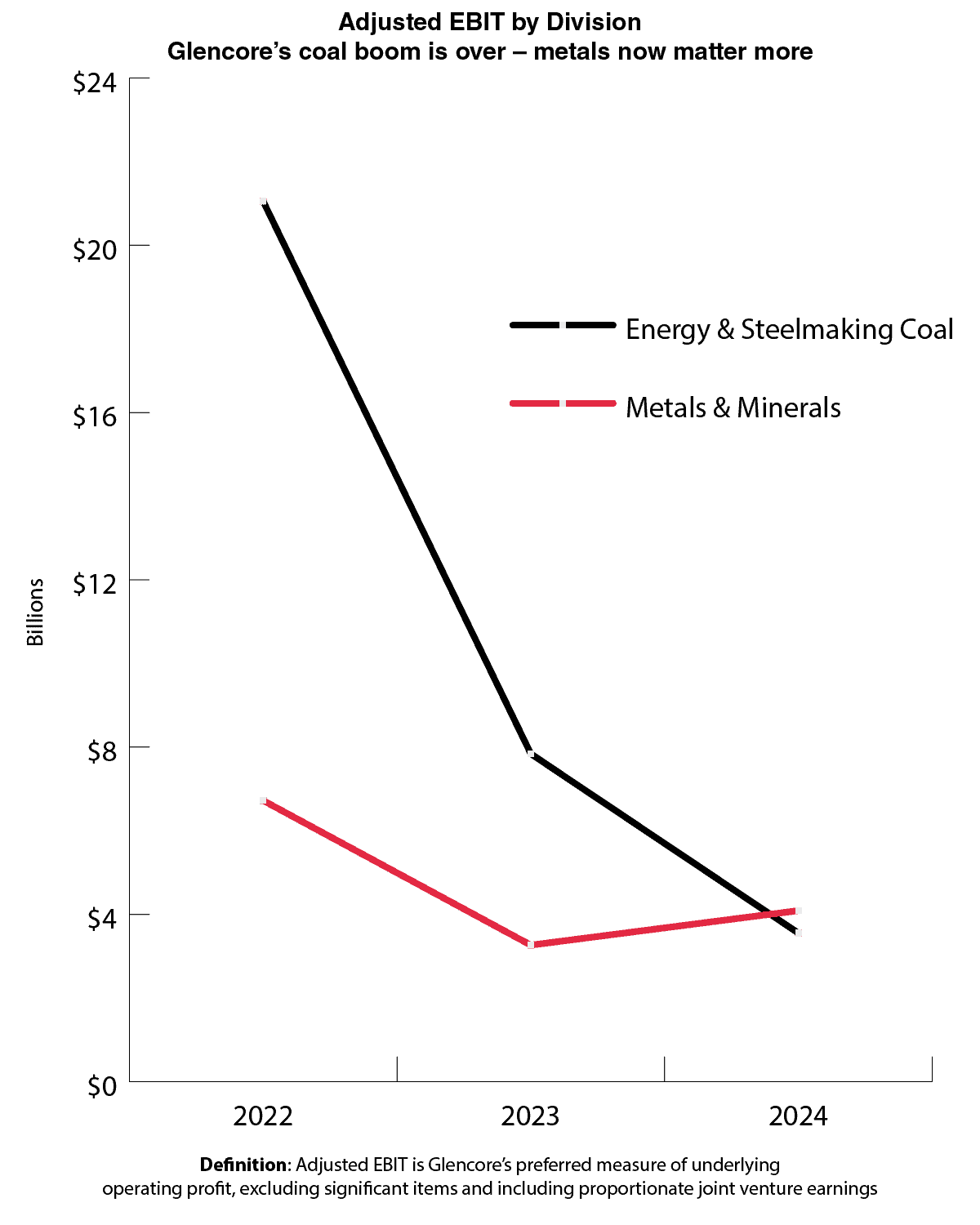

Nevertheless, an adjusted EBIT chart – which strips out one-off accounting objects – tells a unique story. It reveals that, regardless of weak metals costs in 2023 and 2024, the Metals and Minerals division has remained remarkably resilient. In contrast, Vitality and Steelmaking coal earnings have collapsed, now contributing much less to general income than the metals enterprise.

Chart generated by creator

This implies the market could also be underestimating the corporate’s true operational power.

Key dangers

Operational dangers stay, from weather-related disruptions to rising prices as mines go deeper and labour tightens.

The miner’s world footprint additionally exposes it to geopolitical and regulatory uncertainty, together with shifting tariff regimes and authorities intervention in key producing areas. These elements may have an effect on manufacturing and money flows, even when metals demand stays strong.

Backside line

Glencore stays a inventory I proceed to observe intently in my very own portfolio. Its resilient metals earnings and operational flexibility imply that even modest stabilisation may enhance money flows. For traders in search of publicity to long-term commodity developments, it’s price contemplating – significantly because the FTSE 100 sits close to 10,000.