Picture supply: M&S Group plc

Marks & Spencer’s (LSE:MKS) current makeover has boosted each the notion of its model and its shares. Over the previous few years, the British icon has managed to shed its fame for catering just for older prospects and being a bit, properly, middle-of-the-road.

Victoria Wooden, the British comic, as soon as joked: “I know I’m different sizes in different shops, 16 in some, 18 in others. In Marks and Spencer’s, I’m only a size three because they don’t want to upset anybody.”

Then and now

Though those that purchased the retailer’s shares in April 2021 may not be laughing all the best way to the financial institution, they’re in all probability patting themselves on the again.

A £5,000 funding on the time would have purchased 3,185 shares. In the present day (15 April), they’re value (excluding dividends) a powerful £11,498. As an illustration of how properly buyers have finished, the identical funding now would get them 1,800 fewer shares.

However does a 130% rise within the retailer’s share worth imply it’s too late to think about the inventory? Let’s see.

Development alternative

Though the group might be extra talked about for its clothes, it’s the meals aspect of the enterprise that the majority pursuits me.

Over the previous three monetary years, vogue, residence, and sweetness buyer numbers have remained flat. Final 12 months, they have been overtaken by grocery buyers for the primary time. Meals prospects have elevated 9% over the interval and, considerably, they’re making a mean of two.9 extra visits a 12 months to the group’s outlets.

Certainly, the corporate has set itself the goal of doubling the scale of its grocery enterprise over the long run. To realize this, it’s aiming to extend its variety of food-only shops from 328 to 420.

Typically it’s forgotten that, since September 2020, the group’s had a three way partnership with Ocado. Through the 12 weeks to 22 March, it recorded a 2.2% share of the British grocery market. It’s by no means been greater.

Some challenges

Undoubtedly, there was a lack of investor confidence following final 12 months’s cyberattack. This price rather a lot to place proper however, extra considerably, led to some loyal prospects buying elsewhere.

Regardless of this, they got here again and the group’s fame with shoppers seems unhurt. In accordance with polling by YouGov, primarily based on a mixture of notion, high quality, worth, fame, and satisfaction, it stays the nation’s finest model.

In fact, working a sequence of outlets is logistically difficult. And the style trade is notoriously tough to get proper with client tastes altering shortly. That’s one more reason why I consider the emphasis on its less-cyclical meals enterprise is the correct technique.

Closing ideas

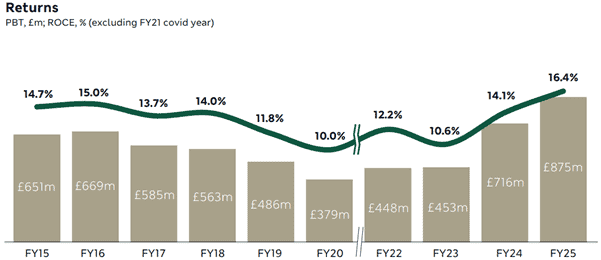

Personally, I believe the group’s made nice strides over the previous 10 years or so, with progress solely interrupted by the pandemic. Each its revenue earlier than tax and return on capital employed are moving into the correct route.

Supply: investor presentation

Supply: investor presentation

And regardless of altering buying habits, it stays an essential a part of Britain’s excessive streets and retail parks.

I like what I see. That’s why I believe it’s a inventory to think about.