The narrative surrounding the “resilient U.S. consumer,” which has been a serious upside shock in 2025, is now going through vital headwinds, based on the International Funding Committee (GIC) at Morgan Stanley Wealth Administration. Whereas client spending has maintained a gradual nominal development charge of 5% to six%, underpinning a bullish outlook for US equities in 2026, the GIC is expressing warning.

Lisa Shalett, chief funding officer and head of the GIC, warned that though the broader macroeconomic image stays cautiously optimistic, the “K-shaped” economic system calls for higher scrutiny. Particularly, she wrote on Monday that she sees “genuine cracks for mid- to lower-end consumers,” a cohort essential to combination development. They might solely account for 40% of consumption within the economic system, she famous, however they make up the majority of marginal development within the consumption that drives the nationwide economic system. Client spending, in any case, is roughly two-thirds of nationwide GDP, a relationship that has been challenged in 2025 by the huge surge in data-center spending.

Shalett cited Oxford Economics information in arguing that the marginal propensity to spend an incremental greenback of earnings is greater than 6x increased for the lowest-income quintile in comparison with the wealthiest cohort, making the 2026 outlook “increasingly fragile” with out their continued energy. In different phrases, the economic system solely actually grows at a wholesome charge the more cash lower- and middle-income individuals must spend, and that’s increasingly more endangered.

The Fragility of Consumption Progress

Client spending has sustained a strong three-year pattern, Shalet identified, pushed largely by constructive wealth results benefiting the highest two earnings quintiles, who personal 80% of shares. Nevertheless, the decrease 60% of households by earnings are actually going through rising stress, probably altering the outlook for 2026.

She wasn’t alone in voicing concern as two different high Wall Road analysts chimed in on Monday, David Kelly of JPMorgan Asset Administration and Torsten Slok of Apollo International Administration. The Ok-shaped economic system—and the essential situation of affordability—stays an enormous query mark for the nationwide economic system.

Kelly argued in a separate observe that whereas the economic system is doing higher for everybody, it simply doesn’t really feel that method. Likening the economic system to the palms of a clock, he mentioned the information exhibits a narrative of boring, constant development, with the rich doing higher however with the vibes getting rougher.

“The reality of today’s economy is like thirteen minutes past one on an analog clock,” he wrote. “The little hand, representing the fortunes of the top 10%, points sharply upwards and to the right. The big hand, representing the progress of everyone else, is also pointing up, but only mildly so. However, it feels like a twenty past one recession, with the little hand still pointing up but the big hand pointing down.”

Kelly cited the September College of Michigan client sentiment survey, wherein 45% mentioned that they and their households had been worse off than a yr in the past. “More Americans feel that they are going backwards in economic terms than believe they are moving forward.”

He wrote that JPMorgan believes the growth continues to be occurring, with actual GDP probably rising at roughly a 3.0% annual tempo within the third quarter and more likely to continue to grow in 2026, albeit with development slowing near 0% within the fourth quarter. That being mentioned, he highlighted some teams experiencing vital financial stress: federal employees coping with a “tide of downsizing since the start of the year,” youthful People going through excessive housing prices and infrequently vital pupil debt, and the roughly 24 million People on the ACA market going through a doubling of insurance coverage premiums in 2026.

Kelly estimated that 43 million People at the moment have federal pupil mortgage debt with a median steadiness of $39,000, “while the median age of first-time home-buyers is now an astonishing 40. Not coincidently, the median age of first marriage has increased from 22.1 years in 1974 to 29.4 years 50 years later.”

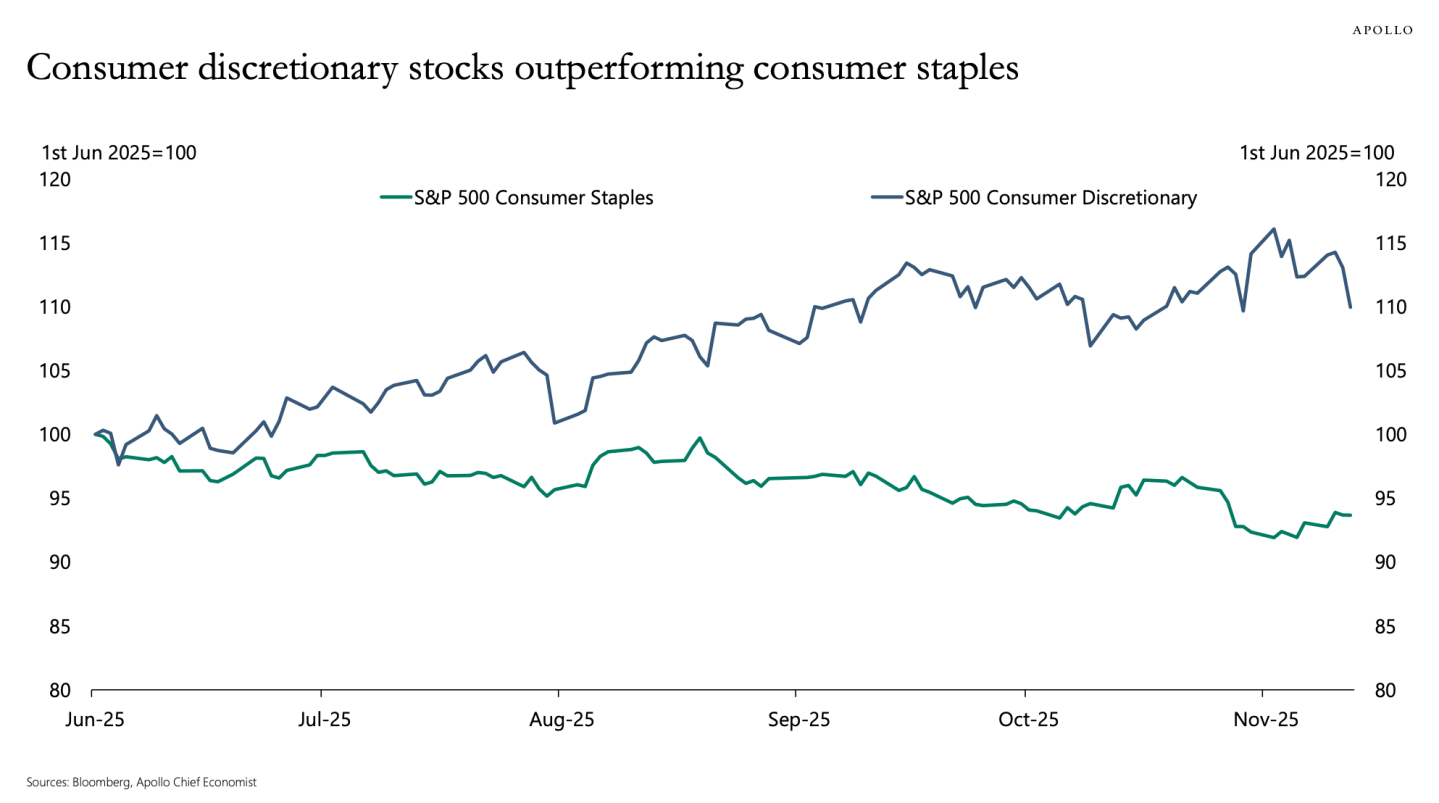

Slok, of Apollo International Administration, wrote in his Every day Spark on Monday that “it is a K-shaped economy for U.S. consumers,” noting that inventory holdings and residential costs have elevated for wealthier People, whereas the money circulate obtained in fastened earnings, together with personal credit score, is close to the best ranges in many years. This energy in higher-income family steadiness sheets could be seen in inventory costs, he famous, with client discretionary shares outperforming client staples in latest months. In different phrases, the stuff the wealthy can purchase is valued increased by Wall Road than the stuff individuals want to purchase.

3 cracks to look at

In keeping with Shalett, the danger of slowing GDP development in 2026 hinges on whether or not the patron begins to “wilt,” an final result instructed by latest information. She added that the GIC is monitoring three key elements highlighting stress within the lower-income brackets.

1. Mounting Credit score Stress and Delinquencies

Credit score stress is starting to “flash yellow” for this cohort. The general financial savings charge has dipped considerably to 4.6%, resting properly beneath the 40-year common of 6.4% and the 80-year common of 8.7%. Concurrently, delinquencies are surging.

In auto lending, subprime 60-day delinquencies have reached 6.7%, marking the best stage since 1994. Though whole family debt grew in keeping with actual disposable earnings (about 4% in Q3 2025), bank card balances grew at twice that tempo, hitting 8%. The newest information exhibits 30-day past-due bank card funds working at 5.3%, an 11-year excessive, alongside surging pupil debt defaults.

2. Affordability Disaster

Mid- to lower-income households are battling an “affordability crisis” catalyzed by persistently excessive worth ranges and a steady 3% inflation charge that conceals a “whack-a-mole” sample of worth spikes. These spikes have particularly impacted requirements like eggs, espresso, electrical energy, auto insurance coverage, and well being care. Compounding this situation, wage development—as tracked by the Certainly Wage Tracker—slowed to 2.5% in September, diminishing customers’ means to outrun inflation.

3. Deteriorating Labor Sentiment

Employment-opportunity sentiment is weakening. Job openings have fallen to 7.2 million, returning to pre-COVID ranges and establishing a 1:1 ratio of openings to job seekers. Moreover, introduced layoffs spiked in October, suggesting the worst year-to-date layoff pattern for the reason that Nice Monetary Disaster.

Client sentiment and job nervousness metrics have been notably troubling. The College of Michigan’s month-to-month survey for November registered one of many lowest general client confidence readings within the final 73 years, and expectations for employment one yr from now noticed the bottom studying since 1980. Anxiousness linked to GenAI job substitute is clearly an element, even amongst high-income employees.

The GIC advises buyers that the premise of 2026 being a yr the place “a rising tide lifts all boats” can not materialize with out energy reaccelerating among the many mid- to lower-end U.S. customers. If the stress on the decrease 60% of households continues to rise, it might result in slowing retail gross sales and actual disposable earnings, presenting a fabric menace to combination spending development.