Picture supply: Getty Pictures

The most effective time to purchase shares is when traders are on the lookout for alternatives elsewhere. And even one of the best companies undergo occasions once they’re out of style with the inventory market.

The unimaginable development Nvidia (NASDAQ:NVDA) has achieved lately isn’t actually displaying indicators of slowing. However with the inventory down because the begin of the 12 months, is it time to have a look?

Dimension

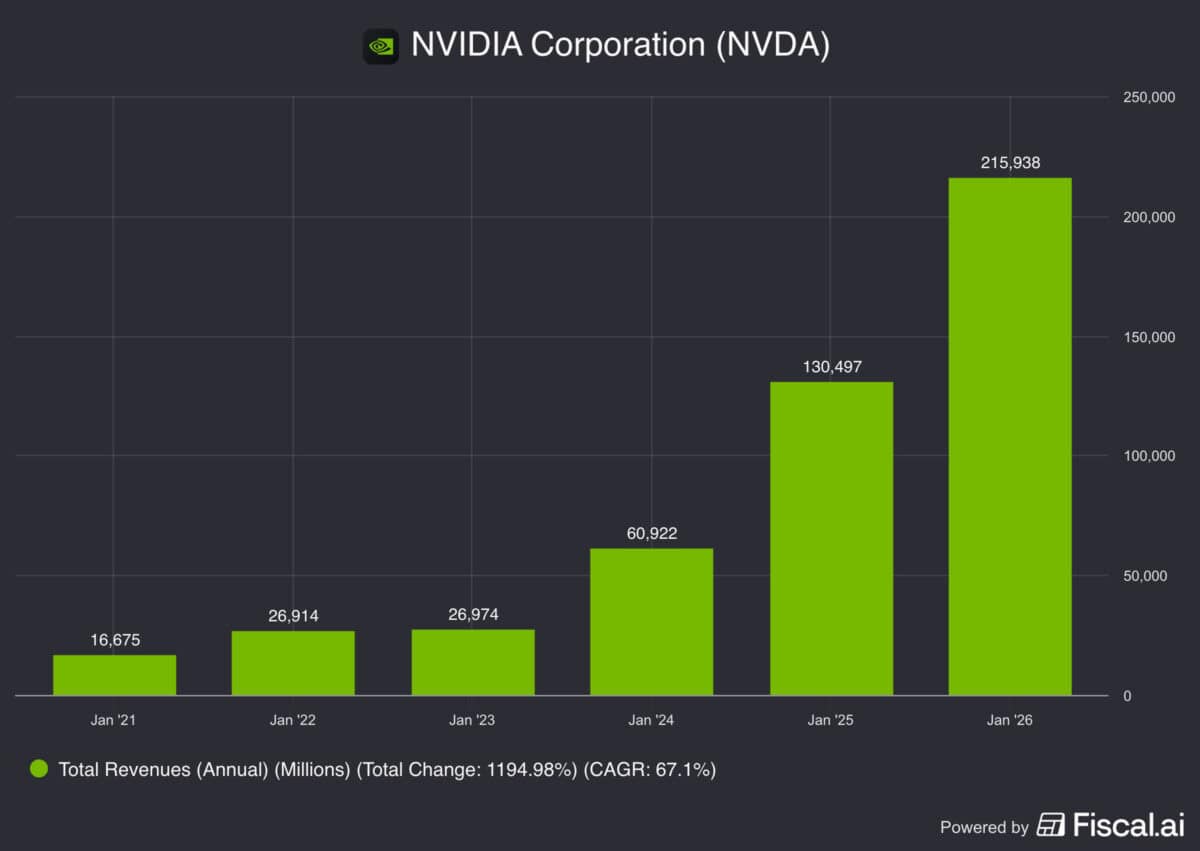

Nvidia’s development since 2021 has been the stuff traders dream of. Revenues have gone from $16.6bn to $215.9bn within the final 5 years, at a mean annual enhance of 67%.

Some traders, although, are beginning to get involved about this. They fear that it will get rather a lot tougher for the corporate to keep up a excessive development charge as its gross sales figures go from massive to very large.

There’s some reality to this, however I don’t assume there’s an actual trigger for alarm. Nvidia’s revenues are nonetheless solely about 50% of what Alphabet and Apple make in annual gross sales, even at $215.9bn.

Meaning the corporate isn’t precisely in uncharted territory, or in actual fact wherever close to it. So I believe there’s nonetheless a solution to go till Nvidia’s measurement will get in the best way of its development prospects.

Valuation

Nvidia isn’t in uncharted territory when it comes to gross sales figures, however it’s with regards to market worth. At $4.4trn, it takes rather a lot to make the inventory go larger from this level.

By itself that’s not a significant concern. There’s no fastened restrict on how excessive a inventory can go and definitely no rule that claims no matter goes up should come down.

Moreover, the share value stagnating as the corporate retains rising means the hole between gross sales and market worth has been closing. That does assist restrict the chance for traders.

Finally, although, the way forward for the inventory goes to depend upon how the underlying enterprise performs. And an enormous a part of that is the demand outlook.

Provide and demand

Funding in AI knowledge centres has been big, nevertheless it isn’t displaying any indicators of slowing down. Earlier this week, Oracle reported a backlog of $553bn – a 325% enhance from final 12 months.

That may solely be good for Nvidia and the inventory is buying and selling at a ahead price-to-earnings (P/E) ratio of 23. That degree implies expectations of robust, however not essentially explosive, development.

The demand aspect of the equation seems robust, however traders must also keep watch over provide. Growing competitors – together with from Nidia’s prospects – is an actual menace to keep watch over.

Common product upgrades have been a key a part of Nvidia’s development story and that is prone to stay the case going ahead. So new options are in all probability the largest menace proper now.

Time to purchase?

I don’t assume there’s any query that Nvidia’s shares are higher worth than they had been firstly of the 12 months. However are they higher worth than different shares available for purchase proper now?

I’m much less satisfied about this. It’s not only a matter of multiples – Nvidia’s don’t look too dangerous to me – however I believe there are extra engaging alternatives elsewhere for the time being.