Picture supply: Getty Photographs

In search of high development shares to purchase at low price? Listed here are two high contenders to think about.

Heading greater

Defence shares like QinetiQ (LSE:QQ.) are surging as European arms budgets sharply enhance. This explicit FTSE 250 contractor — which has soared regardless of a revenue warning in Might — has risen 21% in worth thus far in 2025.

But QinetiQ shares nonetheless look grime low cost, for my part. Metropolis analysts count on earnings to rise 18% within the present monetary yr (to March 2026), leading to a ahead price-to-earnings development (PEG) ratio of 0.9.

Any sub-one ratio signifies {that a} inventory is undervalued.

Latest issues Stateside meant QinetiQ’s earnings fell 11% in monetary 2025. However the enterprise is tipped to ship sustained development from this level on. Backside-line rises of 13% and 10% are additionally being tipped for 2027 and 2028, respectively.

Uncertainty over US defence budgets going forwards stay a menace. However the firm hopes restructuring there — together with the lately introduced sale of its US Federal IT Providers unit — will draw a line below current issues and scale back publicity to extra unstable short-cycle tasks.

On stability, I imagine QinetiQ’s outlook is powerful as broader defence spending amongst NATO and related companions enhance. The corporate’s order guide swelled to £2bn as of March, up 12% yr on yr, as its diversified world footprint helps offset troubles within the US.

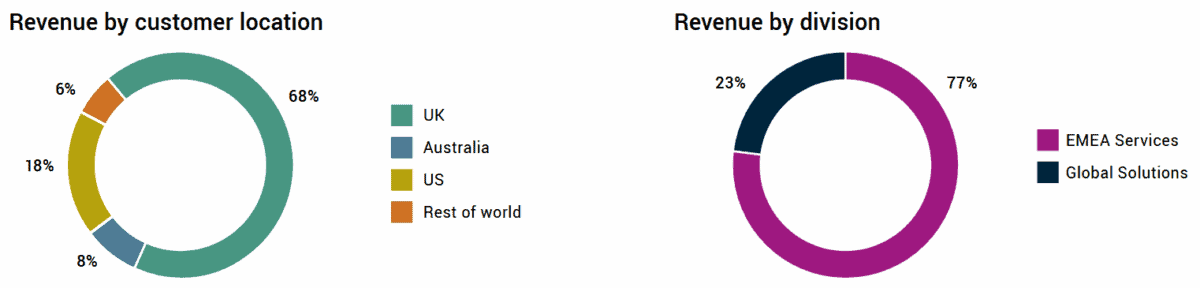

QinetiQ’s gross sales breakdown in monetary 2025. Supply: QinetiQ

QinetiQ’s gross sales breakdown in monetary 2025. Supply: QinetiQ

I believe QinetiQ’s a high option to take into account gaining publicity to the in any other case costly defence sector. It’s additionally value noting the corporate’s ahead price-to-earnings (P/E) ratio is 16.4 occasions, beneath these of FTSE 100 trade gamers BAE Techniques (26.6 occasions), Rolls-Royce (41.5 occasions), and Babcock Worldwide (21.3 occasions).

Doubled in worth

Gold shares are one other asset class I believe development traders want to take a look at. I personally personal an exchange-traded fund (ETF) of a number of steel producers as gold costs soar (they’re up 40% over the past 12 months alone).

Bullion reached new document peaks round $3,700 per ounce simply this week. Additional beneficial properties are tipped as inflationary and development fears climb, and the US greenback faces sustained stress.

One cut-price gold inventory I imagine deserves shut consideration at the moment is Pan African Sources (LSE:PAF).

Metropolis analysts assume earnings will rise 62% in worth this monetary yr (to June 2026) as gold costs rise and the miner’s manufacturing will increase.

The corporate’s thrilling development tasks embody the Mogale Tailings Retreatment (MTR) and Evander tasks in South Africa, and Tennant Mines in Australia. Keep in mind that manufacturing points are a continuing menace that might impression earnings.

At present, Pan African shares commerce on a ahead P/E ratio of seven.1 occasions. In addition they carry a rock-bottom PEG a number of of 0.1. I don’t assume these figures replicate the gold miner’s supreme development prospects, and count on the corporate to proceed rising in worth. Its shares have risen 125% thus far in 2025.