Picture supply: Getty Pictures

There are many high-yielding shares round that I consider are price contemplating for inclusion in a Self-Invested Private Pension (SIPP). Right here’s one which I believe might be locked away and forgotten about for years to return.

Who?

With a present (10 April) yield of 8.4%, Authorized & Basic’s (LSE:LGEN) shares are more likely to be on the radar of earnings buyers. Nevertheless, skilled observers of the inventory market know that top yields needs to be handled with warning.

A return almost 3 times greater than that provided by the FTSE 100 might be an indication that the Metropolis’s anticipating a reduce. In impact, buyers are demanding a premium for the perceived further threat related to proudly owning inventory within the financial savings and retirement group.

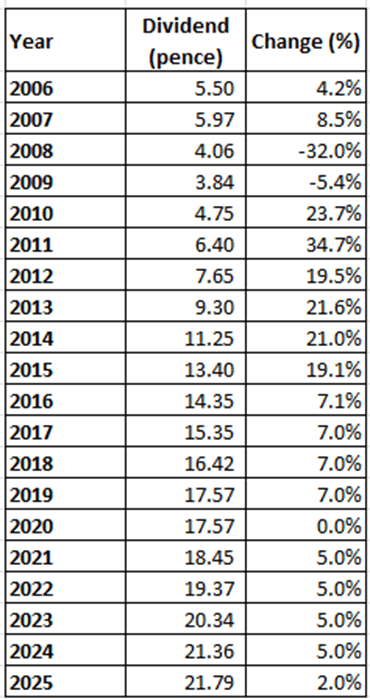

Personally, I believe that is unjustified. Why? Properly, historical past reveals that Authorized & Basic has a wonderful observe file of accelerating its payout. Wanting again over the previous twenty years, it stored it unchanged in 2020. It was final reduce it in 2009 – the second 12 months in a row — on account of the worldwide monetary disaster. In any other case, it’s been will increase all the way in which.

Supply: firm stories

Supply: firm stories

Delving deeper

In fact, historical past is probably not repeated. That’s as a result of dividends are a distribution of revenue, which implies they will fluctuate in keeping with earnings. However a better have a look at funds over the previous twenty years is revealing.

Sustaining the payout in 2020 – described as a “pause year” – was comprehensible given the uncertainty attributable to the pandemic. And in 2008, the group reported an enormous lack of £37.7bn on its funding portfolio. For context, its present market cap is £14.8bn.

In these circumstances, the group’s administrators felt that they had no various however to cut back its dividend. On the time, the group stated monetary markets had been “left reeling after narrowly avoiding a systematic failure of the banking system and entering one of the sharpest, deepest recessions on record”.

Which means that solely in probably the most excessive circumstances has the group reduce its dividend up to now 20 years. And through this era, we’ve had different financial downturns, Brexit, and a pandemic.

My view

In fact, there can by no means be any ensures. However the group’s dividend seems secure for now. The present ceasefire within the Center East has most likely – if it holds – averted a 2008-style market meltdown.

In 2025, the group reported a 9% enhance in core working earnings per share. It says it’s on track to extend its subsequent two annual payouts by 2% a 12 months. And it’s launched a £1.2bn share buyback programme.

Nevertheless, there are a few issues to control. The group has signalled that it has a brand new goal for its Solvency II ratio of 160%-190%. Okay, that is comfortably above the regulatory minimal of 100%. However it’s nicely beneath the 217% reported in June 2025.

And it operates in a aggressive business with challenger manufacturers looking for to take market share.

However I believe the group’s in fairly good monetary form. It’s persevering with to safe a lot of pension schemes to handle from its giant pipeline of potential new enterprise. And its retirement division ought to do nicely because the State Pension age rises additional.

In truth, I believe it’s a high earnings share with an incredible yield that buyers might take into account.