Picture supply: Getty Photographs

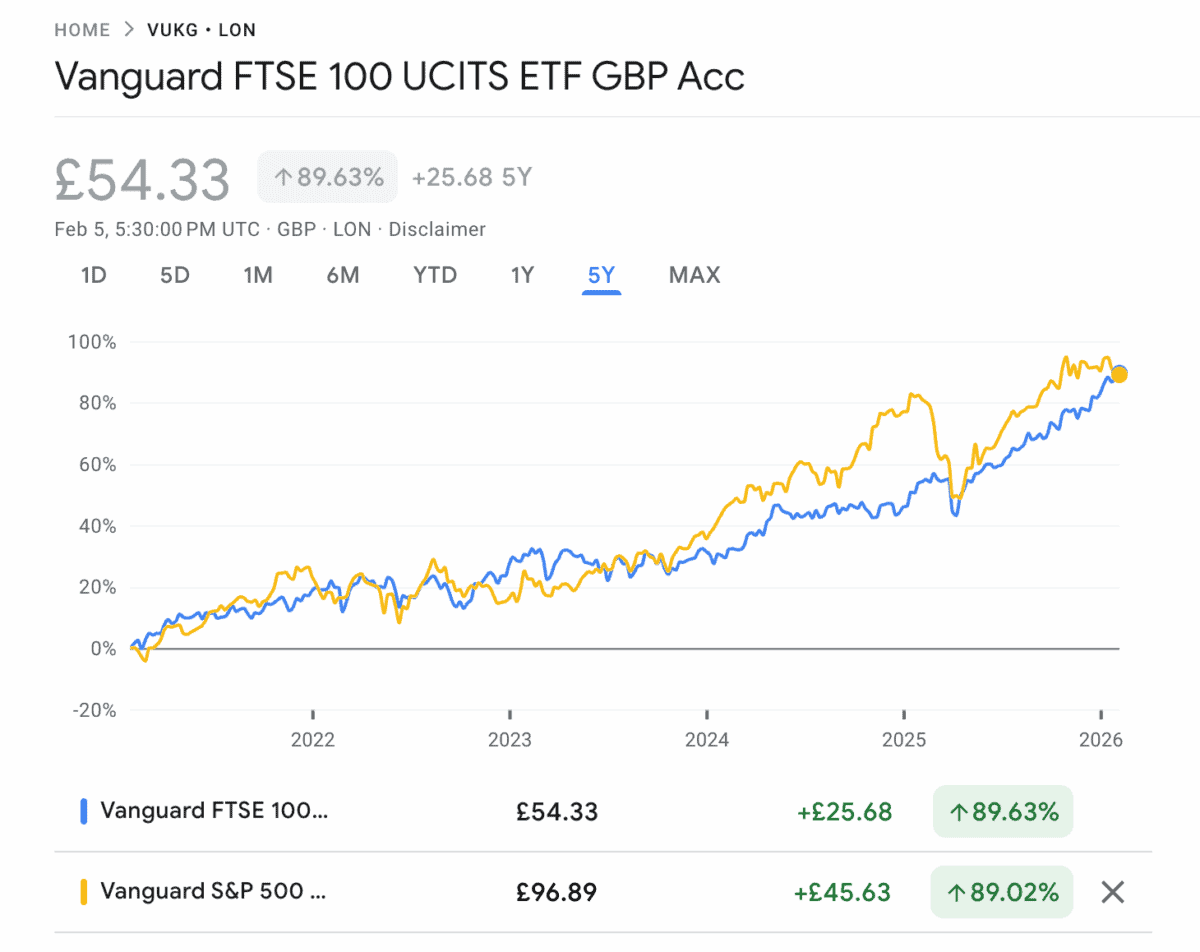

The FTSE 100 is up 1.36% this week, whereas the S&P 500 has fallen 0.7%. And that is simply the newest replace in what has been fairly a run for UK shares towards their US counterparts.

A stopped clock is true twice a day. However the FTSE 100’s current outperformance isn’t only a case of being in the fitting place on the proper time – there’s a deeper structural cause to pay attention to.

Diversification

It’s no secret that the S&P 500 has a a lot heavier focus in tech shares than the FTSE 100. And that’s been an enormous benefit over the previous couple of years, however the state of affairs has modified just lately.

Synthetic intelligence (AI) has been a giant problem for the US index. On the one hand, buyers are involved that demand isn’t sturdy sufficient to justify the continued investments in knowledge centres.

Alternatively, there are issues that current software program corporations are about to see their aggressive positions threatened by AI startups. So there’s been strain right here as properly.

The FTSE 100 hasn’t been solely resistant to this – it’s had its share of fallers. However no one’s complaining concerning the index having a relative lack of tech publicity in the mean time.

One good week doesn’t make up for years of relative underperformance. The most recent strikes, although, imply the entire returns from the FTSE 100 and the S&P 500 are roughly stage over the past 5 years.

So the place ought to buyers search for alternatives proper now? Have US shares fallen sufficient to grow to be low-cost, or are UK shares lastly selecting up some momentum?

The place to look?

I feel there are alternatives on each side of the Atlantic. And constructing a diversified portfolio means trying to reap the benefits of each when possibilities to take action current themselves.

One instance is Bunzl (LSE:BNZL). The FTSE 100 firm is a distributor of consumables corresponding to espresso cups, cleansing provides, and provider baggage.

It doesn’t sound like an thrilling enterprise and natural development has been restricted just lately, however the agency has an impressive monitor file of rising by means of acquisitions. And it’s unusually good at this.

This may be dangerous – there’s at all times a hazard of paying an excessive amount of in a deal and even the very best buyers have made errors. However Bunzl has an unusually sturdy investing self-discipline.

The place different companies have began paying larger multiples, Bunzl has caught to valuations of round eight instances EBITDA (earnings earlier than curiosity, tax, depreciation, and amortisation). That doesn’t assure good returns, but it surely provides the corporate the very best probability.

Publicity to the weakest elements of the US economic system mixed with some unforced errors have precipitated the inventory to crash 38% in 12 months. However I feel it’s properly price contemplating at in the present day’s costs.

Lengthy-term worth

I feel Bunzl is a good instance of a essentially sturdy enterprise coping with some short-term challenges. However I anticipate the agency to fare significantly better over the long run.

If I’m proper, the present share value may very well be a very nice shopping for alternative. And I additionally assume there are related alternatives in plenty of US shares which have fallen just lately.