Picture supply: Getty Pictures

Because the begin of the battle within the Center East, shares in BP have set a brand new 52-week excessive. And with the oil worth displaying no signal of dropping, there might be extra data damaged quickly.

Nevertheless, there’s one other inventory that’s risen extra over the previous 4 weeks. The 2 are like chalk and cheese, so how can this non-energy group be doing so properly given the present world uncertainty? Let’s take a more in-depth look.

Who?

The RELX (LSE:REL) share worth has been rising steadily.

In the present day (16 March), shares within the FTSE 100 data and knowledge analytics group are altering arms for 17% greater than they have been a month in the past. Over the identical interval, BP’s share worth is up 16%.

It follows a dramatic fall in early February, when buyers despatched RELX’s inventory worth 14% decrease on the day that Anthropic introduced it had developed an add-on for its Claude synthetic intelligence (AI) software. Though circuitously replicating any of the providers offered by RELX, there was a worry that it may empower authorized groups and disrupt the enterprise fashions of established firms working within the sector.

Different knowledge and software program shares additionally suffered. Since then, quite a lot of observers have come to the defence of the group and the sector basically.

Nvidia’s boss, Jensen Huang, lately stated: “I think the markets got it wrong.” He reckons AI brokers will depend on the information that these firms personal fairly than make their services out of date.

Finsbury Progress and Revenue Belief has important positions in lots of knowledge firms, together with RELX. Its fund supervisor, Nick Practice, claims all of them have “a credible opportunity to bring AI-enhanced services to their customers, an opportunity based on their ownership of data assets that are not available to emerging large language models (LLMs) like ChatGPT or Anthropic.”

Large volumes of proprietary knowledge

And in the case of knowledge, RELX has numerous it. For instance, its Scientific, Technical, and Medical division makes out there 105m publications to subscribers. Individually, authorized professionals have entry to over 200bn paperwork. The group claims to analyse 130bn transactions yearly.

Though spectacular, this makes it notably susceptible to a cyber assault or knowledge privateness breach.

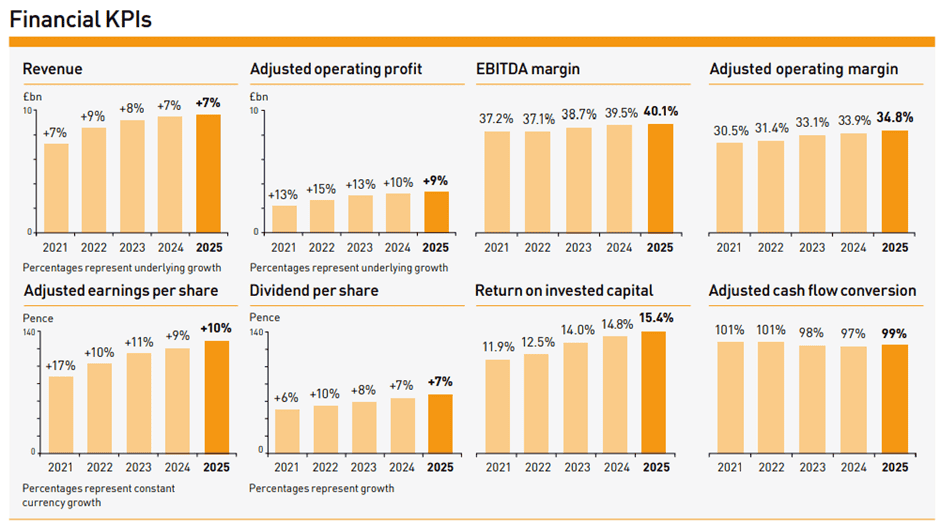

However in the intervening time, RELX sees AI as a chance to boost buyer worth and cut back prices. Certainly, it was spending closely on AI lengthy earlier than it grew to become modern. This has helped drive its key monetary measures increased throughout its previous 5 monetary years.

Supply: RELX annual report 2025

Supply: RELX annual report 2025

Particularly, its give attention to enterprise prospects — the place the emphasis is extra on high quality than worth — has helped it improve its EBITDA (earnings earlier than curiosity, tax, depreciation, and amortisation) margin.

And I reckon the latest pullback within the group’s share worth may make it a wonderful shopping for alternative to contemplate.

Supply: London Inventory Change Group/EPS TTTM = earnings per share trailing 12-months

Supply: London Inventory Change Group/EPS TTTM = earnings per share trailing 12-months

Over the previous 5 years, the inventory’s common (median) price-to-earnings ratio has been roughly 30. Based mostly on its 2025 earnings per share (EPS) of 112p, it’s now below 23.

Hopefully, the battle will finish quickly. And when it does, vitality costs are prone to fall again in direction of pre-conflict ranges. In these circumstances, BP’s share worth might be going to undergo however I’m assured that RELX’s will proceed to go in the wrong way.