")

When my daughter was born, one of many first issues I did was open a SIPP (Self-Invested Private Pension) in her title. It’d sound untimely — in any case, retirement’s at the least 55 years away for a new child.

However that’s exactly the rationale to do it. Time is the one strongest ingredient in wealth creation, and a SIPP opened at delivery has extra of it than virtually some other funding automobile.

Right here’s the fantastically easy maths. After I contribute simply £240 a month right into a Junior SIPP — that’s the equal of round £55 per week — the federal government mechanically tops it up with 20% tax aid, bringing the gross contribution to £300 a month, or £3,600 a yr. That’s the present most annual allowance for a non-earner.

At a ten% common annual progress fee, compounded month-to-month over 55 years, that £300 a month snowballs into roughly £8.6m. The entire quantity really contributed? Simply £198,000.

The remainder — which is over £8.3m — is generated purely by compound progress. It’s just about the closest factor to monetary magic that exists.

Picture supply: Getty Pictures

It’s very achievable

Now, 10% may sound formidable, but it surely’s broadly according to the long-run common return of the inventory market. The S&P 500, for example, has returned round 10%-11% yearly over the previous century. After all, previous efficiency doesn’t assure future outcomes, and there will likely be stomach-churning drops alongside the way in which. However over a 55-year horizon, historical past suggests the percentages are firmly in your favour.

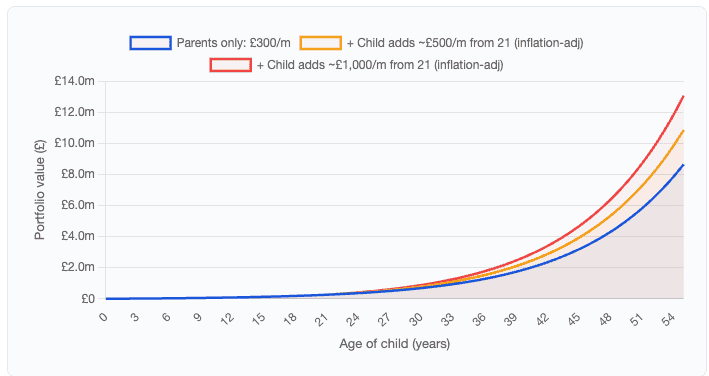

And right here’s the place it will get actually thrilling. These figures assume the dad and mom or grandparents shoulder the total price for 55 years. In actuality, sooner or later the kid grows up, will get a job, and might begin contributing themselves. If they start including to the pot from age 21, the numbers turn into actually staggering.

State of affairs (10% progress)Worth at 55Total contributedParents solely: £300/m for 55 years£8,574,424£198,000Child provides £500/m (inflation-adj) from 21£14,853,736£402,000Child provides £1,000/m (inflation-adj) from 21£21,133,048£606,000

The place to speculate?

That is the million-dollar query. Nevertheless, right here’s some issues to think about. The portfolio will begin small, so it might be finest to make fewer trades (restrict transaction prices). Which may imply taking a single stake in a fund or belief that gives immediate diversification throughout corporations.

One belief that continues to draw my consideration is Scottish Mortgage Funding Belief (LSE:SMT). The funding belief has an incredible monitor report of selecting the subsequent huge winners, and can hopefully have the ability to navigate a number of the upcoming AI upheaval. Scottish Mortgage has positions within the likes of TSMC, Mercadolibre, ASML, and Nvidia. These are know-how leaders, and three out of the 4 have carried out very properly over the previous yr.

However the largest holding by some margin in SpaceX. And I like that. If I needed to take a guess at what I feel would be the greatest firm on the earth in a decade from now, I’d say SpaceX. I could possibly be very flawed, however I feel there’s a really compelling argument to consider SpaceX will dominate the area financial system.

Dangers? Effectively, Scottish Mortgage makes use of gearing — borrowing to speculate. This may heighten features when shares go up, however enlarge losses when investments go down.

Nonetheless, this could possibly be a wonderful long-term automobile for a passive investor. I feel it’s value contemplating.