Picture supply: Getty Photographs

By lunchtime at the moment (6 January), the JD Sports activities Vogue (LSE:JD.) share value was almost 7% decrease after the Financial institution of America downgraded the inventory. In November, Shore Capital was additionally downbeat in regards to the retailer’s shares. It mentioned the group’s third quarter (the 13 weeks to 1 November 2025) buying and selling replace “underscored the depth of the present buying and selling headwinds“.

Admittedly, the retailer’s newest press launch wasn’t very optimistic. The group mentioned pre-tax income could be on the decrease finish of the consensus of estimates (£853m-£888m). And, worryingly, in comparison with a 12 months earlier, like-for-like (LFL) gross sales have been down 1.7%, with Asia-Pacific being the one area to develop.

Shore Capital was involved that the group was unable to cross on rising labour and working prices to clients attributable to a falling high line.

Nonetheless, regardless of this obvious doom and gloom, I stay optimistic in regards to the prospects for JD Sports activities. Right here’s why.

Low-cost as chips

In the intervening time, I reckon the group’s shares are attractively priced. Actually, they give the impression of being to be in cut price territory.

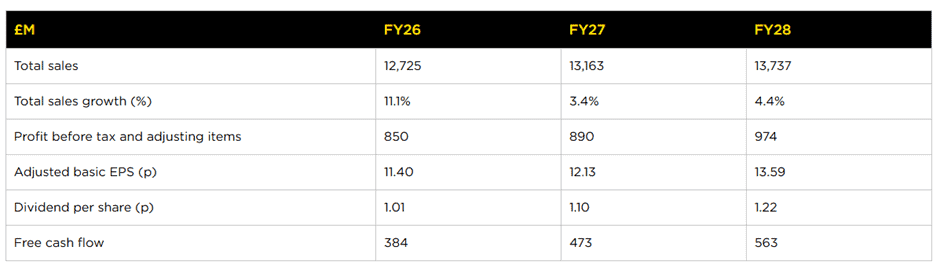

Analysts predict adjusted primary earnings per share of 11.4p for its present monetary 12 months ending in February 2026 (FY26). This implies the inventory trades on simply 7.3 occasions anticipated earnings. Waiting for FY28, the a number of drops to six.1. That is extremely low cost for any enterprise, particularly one which’s on the FTSE 100.

Supply: firm web site

Supply: firm web site

And with comparatively little borrowing on its stability sheet – it reported web debt (excluding leases) of £125m at 2 August 2025 — it stays impressively money generative. That is essential as a result of it offers it the headroom to spend extra on both revamping current shops or shopping for extra ones. Alternatively, it may return additional money to shareholders.

Abroad focus

I’m certain this summer time’s FIFA World Cup within the area may also assist increase gross sales. Nevertheless it’s additionally a reminder of how the group’s share value has struggled lately. Because the final competitors in Qatar in December 2022, it’s fallen by round 30%.

Importantly, though Nike, the struggling US sportswear large, is believed to account for round half of the group’s gross sales, JD Sports activities is brand-agnostic. The British retailer has a popularity for responding quickly to altering shopper traits. A have a look at its web site reveals 108 totally different manufacturers/producers listed.

Ultimate ideas

I acknowledge that JD Sports activities seems to have fallen out of favour in the mean time. The group’s income is rising as a result of it’s increasing each organically and thru acquisition, and never by boosting LFL gross sales. To regain investor confidence, I believe it’s going to have to handle this concern.

However the issues going through the group seem like sector-wide somewhat than something particular to JD Sports activities. Certainly, the corporate itself retains a robust model and a strong stability sheet. I believe the present downturn within the traditionally resilient athleisure/sports activities market is a brief blip.

| AlphaStreet")