Many gig employees and small-business homeowners are advised to open what’s often known as a solo, or one-participant, 401(ok). Fewer are advised why it may be one of the vital highly effective retirement financial savings instruments out there to individuals who work for themselves.

The brief reply is contribution limits. A solo 401(ok) permits eligible enterprise homeowners to save lots of excess of they may in an IRA and, in lots of instances, greater than in a conventional office 401(ok).

The IRS defines a one-participant 401(ok) as a plan masking a enterprise proprietor with no workers aside from a partner. These plans are sometimes called solo 401(ok)s, solo Ks or uni-Ks.

Gig employees and small-business homeowners usually overlook the solo 401(ok). Right here’s how the 2026 contribution limits work and why some excessive earners can bypass a brand new catch-up rule.

We Are/Getty Photos

What’s the enchantment of solo 401(ok) plans?

What makes the solo 401(ok) particularly enticing is how contributions work. The enterprise proprietor successfully wears two hats, worker and employer, and may contribute in each roles.

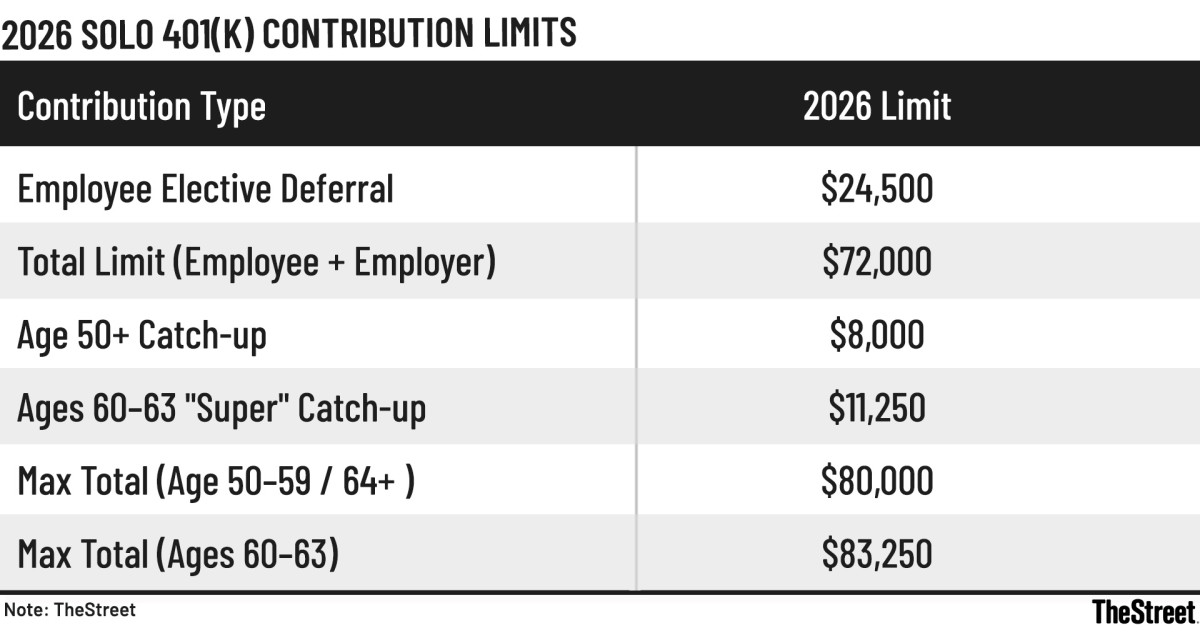

As the worker, the proprietor could make elective deferrals of as much as 100% of compensation, or earned earnings for the self-employed, capped on the annual deferral restrict. For 2026, that restrict rises to $24,500. The mixed worker and employer contribution restrict climbs to $72,000 earlier than any catch-up contributions, in keeping with Constancy Investments.

Because the employer, the proprietor could make nonelective contributions of as much as 25% of compensation, as outlined by the plan. The calculation differs barely for self-employed people, as defined under.

Associated: Medicare errors seniors want they’d recognized sooner

Taken collectively, these limits enable a high-earning solo entrepreneur to shelter as much as $72,000 in 2026. For these eligible for catch-up contributions, the overall can attain $83,250.

There is a crucial caveat for enterprise homeowners who additionally take part in a 401(ok) by one other employer. Elective deferral limits apply per particular person, not per plan. Deferrals made to any 401(ok) throughout the 12 months rely towards the identical annual cap.

Calculating contributions is extra complicated for self-employed people. The IRS requires a particular computation to find out the utmost elective deferrals and employer contributions you may make for your self.

On this case, compensation is outlined as earned earnings, which suggests web earnings from self-employment after subtracting one-half of your self-employment tax and any contributions made in your behalf.

That complexity is one motive advisers say many solo employees underfund these plans or keep away from them altogether. For these keen to do the maths or get assist, the payoff will be substantial.

In sensible phrases, listed below are the important thing guidelines solo entrepreneurs want to know.

TheStreet

Worker deferral limits for 2026 (solo 401(ok))

When performing as the worker, a enterprise proprietor could make elective deferrals as much as the annual IRS cap. For 2026, these limits rise with inflation.

- Base worker salary-deferral restrict: $24,500 in 2026. This restrict applies per particular person, not per plan, and contains all 401(ok) or 403(b) plans during which you take part throughout the 12 months.

- Flexibility of selection: Deferrals will be made on a pre-tax foundation, as Roth contributions, or as a mixture of the 2.

Complete solo 401(ok) contribution restrict (worker plus employer)

The true energy of the solo 401(ok) lies within the mixed contribution restrict. As a result of the enterprise proprietor acts as each worker and employer, the overall quantity that may be saved is way greater than in most office plans.

- Mixed restrict: For 2026, the overall per-person contribution restrict is $72,000, earlier than catch-up contributions.

- Employer contribution math: Whereas worker deferrals are capped at $24,500, employer profit-sharing contributions are typically restricted to 25% of compensation, or about 20% of web self-employment earnings for sole proprietors. No matter earnings stage, the mixed whole can not exceed the $72,000 ceiling.

Enhanced catch-up alternatives below SECURE 2.0

For these nearing retirement, 2026 features a tiered catch-up construction created by the SECURE 2.0 Act.

- Commonplace catch-up (ages 50-59 and 64+): The catch-up contribution is $8,000 for 2026. That raises the utmost worker deferral to $32,500 and the general solo 401(ok) restrict to $80,000.

- “Super” catch-up (ages 60-63): People on this age band could make an enhanced catch-up contribution of $11,250.

Most worker deferral: $35,750.Most whole Solo 401(ok): $83,250, assuming earnings helps it.

A word on the $150,000 Roth catch-up rule

SECURE 2.0 requires excessive earners with prior-year W-2 wages above $150,000 to make catch-up contributions on a Roth foundation. In follow, this rule does not apply to most self-employed solo 401(ok) homeowners as a result of they don’t obtain wages topic to FICA within the conventional sense.

That exemption is one motive the solo 401(ok) stays particularly enticing for high-earning impartial employees.

Even so, solo plans are extra complicated than IRAs and infrequently extra sophisticated than employer-sponsored 401(ok)s. That complexity explains why account homeowners ceaselessly have questions on eligibility and setup, contribution limits, Roth versus pre-tax methods, the $150,000 catch-up rule, loans, rollovers, mega backdoor Roth conversions, and ongoing reporting and compliance.

The most typical solo 401(ok) questions, answered

With the principles laid out, the following problem for a lot of solo entrepreneurs is making use of them in actual life. The enchantment of a solo 401(ok) is obvious. So is the complexity, which helps clarify why questions on eligibility, Roth guidelines, reporting, and compliance usually come up solely after a plan is in place.

Sarah Brenner, director of retirement schooling at Ed Slott & Co., mentioned the next are among the many most typical solo 401(ok) questions her agency hears from advisers.

Is a solo 401(ok) a separate sort of 401(ok) plan?

No. A one-participant 401(ok) shouldn’t be a definite plan sort. It’s merely a 401(ok) that covers a enterprise proprietor with no workers, or the proprietor and a partner. The identical core guidelines and necessities that apply to different 401(ok) plans apply right here as nicely.

What makes solo 401(ok)s distinctive?

The defining function is that the enterprise proprietor wears two hats, worker and employer. That enables contributions in each roles: elective deferrals as the worker and profit-sharing contributions because the employer. Every contribution sort has its personal limits, and each are topic to an total annual cap.

How does the necessary Roth catch-up rule apply to solo 401(ok)s?

Starting in 2026, sure older, higher-paid workers who need to make catch-up contributions should accomplish that on a Roth foundation. The rule applies to these with prior-year W-2 wages above $150,000. However it typically doesn’t apply to self-employed solo 401(ok) homeowners as a result of they don’t obtain wages topic to FICA.

Does a solo 401(ok) sponsor need to file Type 5500?

A solo 401(ok) sponsor by no means recordsdata a full Type 5500. Nevertheless, Type 5500-EZ should be filed as soon as plan belongings exceed $250,000 on the finish of a plan 12 months, or within the 12 months the plan is terminated, even when belongings are under that threshold.

Does nondiscrimination testing apply?

No. As a result of there are not any non-owner workers, nondiscrimination testing shouldn’t be required.