Picture supply: Getty Photos

My particular person shares portfolio primarily consists of high-quality, blue-chip progress shares with clear aggressive benefits. I’m speaking about names like Apple, Amazon, and Rightmove.

Nevertheless, I’m not afraid to take small positions in high-risk, high-return progress firms in an effort to generate explosive positive aspects. I name these my ‘moonshot’ progress shares.

Not too long ago, I used to be doing a little analysis into the autonomous driving and humanoid robotics industries and discovered a comparatively unknown enterprise that I believed appeared actually fascinating. So, I purchased just a few shares for my portfolio.

This inventory is actually dangerous. However I feel it might have extra potential than another in my portfolio.

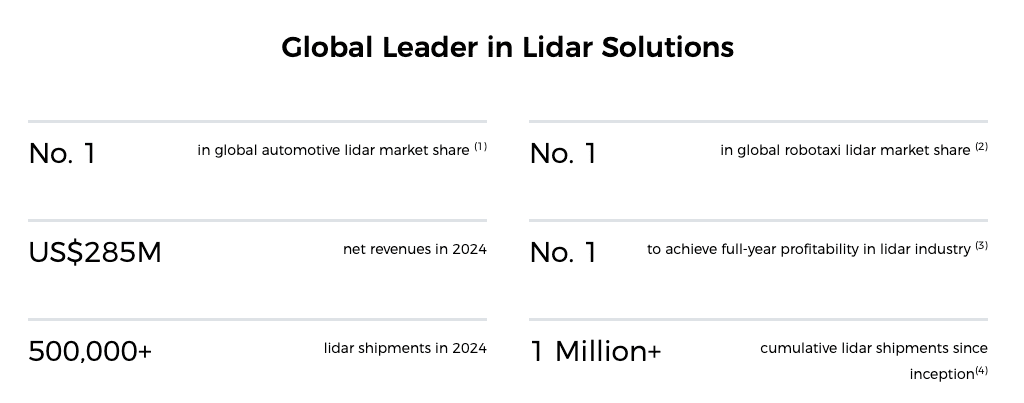

A worldwide chief in area of interest know-how

The inventory I purchased was Hesai Group (NASDAQ: HSAI). A Chinese language firm that’s listed on each the Nasdaq and the Hong Kong Inventory Trade, it’s a world chief in LiDAR (Gentle Detection and Ranging) know-how.

LiDAR is a distant sensing tech that emits fast laser pulses to create exact, high-resolution 3D maps of the atmosphere. Right now, it’s utilized by most autonomous driving firms together with Waymo, Apollo, and Zoox.

In 2024, Hesai had a 33% market share of the worldwide LiDAR market by income (61% market share in autonomous ‘Level 4’ driving). In the meantime, it additionally had extra world LiDAR revealed patent purposes than another firm.

Supply: Hesai Group

Supply: Hesai Group

Out of my consolation zone

Now, that is very totally different from my regular kind of funding. It’s honest to say that it’s out of my consolation zone.

For a begin, it’s a Chinese language ADR (American Depositary Receipt). I are inclined to keep away from these as a result of geopolitical dangers (the potential for a US delisting, excessive tariffs, and so forth) and transparency points.

Secondly, it’s laborious to know if the corporate has a real aggressive benefit. Whereas it has substantial market share, it has just a few opponents together with the likes of Luminar and Ouster.

Huge potential

As I stated above although, I see enormous potential. There are two the reason why.

For a begin, Hesai seems rather well positioned to profit from the shift to self-driving autos. At present, it has partnerships with a spread of robotaxi firms together with Apollo, Pony.ai, DiDi, and WeRide. It additionally has partnerships with many common carmakers providing Superior Driver-Help Techniques (ADAS) and exploring self-driving tech. Names right here embrace Mercedes-Benz, Toyota, and Li Auto. Because the self-driving trade grows, I count on LiDAR know-how to be in excessive demand.

It’s price noting that the corporate is already rising at a fast clip. In Q2, it made complete LiDAR shipments of 352,095 models, a rise of 307% 12 months on 12 months. This resulted in a 54% improve in income. It additionally led to a swing from losses to revenue.

I’ll level out that I count on this inventory to be a wild journey. It might crash spectacularly. With a market cap of round $4bn and a price-to-sales ratio of 8.5, nonetheless, I just like the set-up. I’m excited in regards to the potential.

Q3 2025 earnings outcomes | AlphaStreet")