Seize a espresso — as a result of stablecoins could also be about to reshape the US bond market. A brand new Normal Chartered report suggests rising demand for Treasury payments from digital greenback issuers may quietly power Washington to rethink the way it funds its debt.

Crypto Information of the Day: Stablecoin Demand May Pressure Washington to Rethink US Debt Technique

Stablecoins might quickly reshape the US Treasury market, probably forcing a radical shift in debt issuance, in accordance with a brand new report from Normal Chartered.

The financial institution tasks that stablecoin issuers may generate between $0.8 trillion and $1 trillion of contemporary demand for Treasury payments (T-bills) by the top of 2028.

This pattern, when mixed with Federal Reserve purchases, may push complete short-term Treasury demand to $2.2 trillion.

The report warns that the Treasury may use this rising extra demand as justification to extend T-bill issuance whereas decreasing long-term bond provide. Such a transfer may, in impact, enable the US authorities to droop all 30-year bond auctions for the subsequent three years.

“We think the US Treasury may use this potential excess demand as a reason to issue more T-bills,” wrote Geoff Kendrick within the newest Normal Chartered report, highlighting stablecoin issuers as more and more vital consumers of short-term US debt.

Rising market stablecoins are anticipated to drive nearly all of this demand. Normal Chartered estimates that two-thirds of projected T-bill demand will come from rising markets, representing internet new demand. In the meantime, stablecoins in developed markets largely substitute for current holdings.

This sample highlights the rising position of digital property in world capital flows and their affect on conventional fixed-income markets.

The potential implications for the Treasury yield curve are substantial. Shifting roughly $9 billion from long-term bonds to T-bills may initially flatten the US Treasury curve.

Attention-grabbing notice from Normal Chartered on stablecoins & T-bills.

Regardless of provide stalling since October, they nonetheless venture 2 trillions $ by 2028 (projection cited by the US Treasury).

EM would drive 2/3 of demand (internet new T-bill demand), vs DM the place it’s principally substitution. pic.twitter.com/fKVqgRYNZF

— Googly 👀 (@0xG00gly) February 23, 2026

Yield Curve Dangers Mount as Treasury Weighs Increasing T-Invoice Share

Normal Chartered notes, nevertheless, that long-term premia, fiscal deficit considerations, and market sentiment may affect investor response over time.

The financial institution cautions {that a} bull flattening on the entrance finish often is the rapid response, however structural elements, together with time period premia and rollover danger, may form yields in another way in the long term.

Treasury Secretary Scott Bessent may leverage this situation to extend the share of T-bills throughout the general debt portfolio.

Elevating the T-bill share by simply 2.5% over three years would generate roughly $900 billion of extra T-bill provide, offsetting the projected extra demand.

This might ease shortage on the entrance finish of the curve whereas conserving the 10-year Treasury yield manageable.

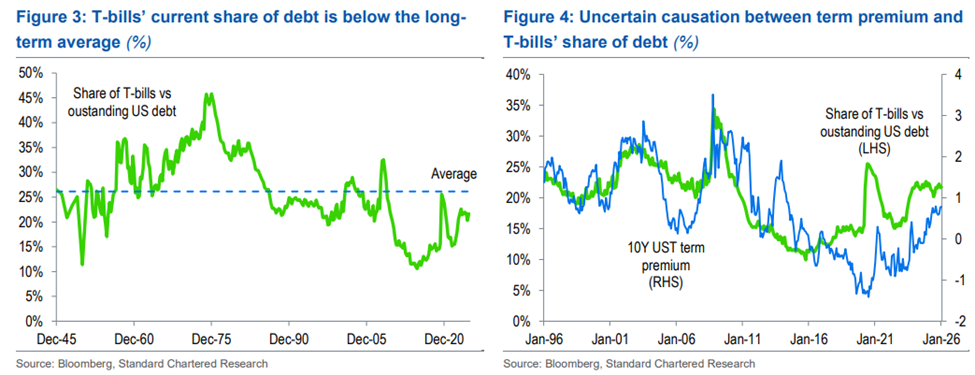

The report additionally notes that traditionally, T-bills have averaged 26.1% of excellent marketable debt. That is effectively above the Treasury Borrowing Advisory Committee’s advisable 15–20% vary, suggesting room for a rise.

Regardless of short-term stagnation, stablecoin market capitalization is projected to succeed in $2 trillion by the top of 2028. Development has lately stalled at round $304 billion, influenced by weaker digital asset markets and regulatory delays following the US GENIUS Act.

Normal Chartered Stablecoin Market Cap Projection. Supply: Normal Chartered.

Nonetheless, Normal Chartered considers these elements cyclical reasonably than structural. Stablecoin demand, mixed with ongoing Fed Reserve Administration Purchases and substitute of maturing mortgage-backed securities, may subsequently drive a historic reshaping of short-term US debt markets.

The report concludes that whereas suspending 30-year bond auctions wouldn’t be unprecedented—the Treasury paused them from 2002 to 2006—the present deficit setting differs markedly.