Picture supply: Getty Photographs

Billionaire investor Warren Buffett has a brilliantly easy strategy to investing. Give attention to the underlying enterprise as an alternative of the share value and be grasping when others are fearful.

These appear to be apparent ideas. But it surely’s shocking how a lot of a bonus buyers can glean simply by sticking to those in a inventory market crash.

Inventory market threats

Proper now, buyers have lots to fret about within the inventory market. There’s the continuing danger of synthetic intelligence (AI) resulting in job losses and placing stress on shoppers.

Which may present up in a number of completely different locations. Decrease discretionary spending is one instance and one other is a rise in mortgage defaults is one other.

Extra not too long ago, battle in Iran has added one other dimension. Rising oil costs are set to bump up prices for heavy industrial companies which have excessive energy wants.

Some firms although are extra in danger than others. And a inventory market crash can provide buyers the possibility to purchase shares in high quality firms at very engaging costs.

Alternatives

Buffett’s preliminary Financial institution of America deal is a good instance of being grasping when others are fearful. With the financial institution in monetary hassle in 2011, Buffett organized a $5bn funding.

In return, his funding automobile Berkshire Hathaway acquired 50,000 shares of most well-liked inventory, which got here with a 6% dividend. It additionally acquired warrants to purchase 700m peculiar shares at $7.14.

In 2017, Buffett used the warrants to purchase a inventory that was buying and selling at $24 per share utilizing the unique most well-liked inventory. So the preliminary $5bn become virtually $17bn in a single transfer.

Realistically, buyers like me are extremely unlikely to be able to do this type of deal within the subsequent inventory market crash. However I feel there can be alternatives for many who are on the lookout for them.

The place I’m wanting

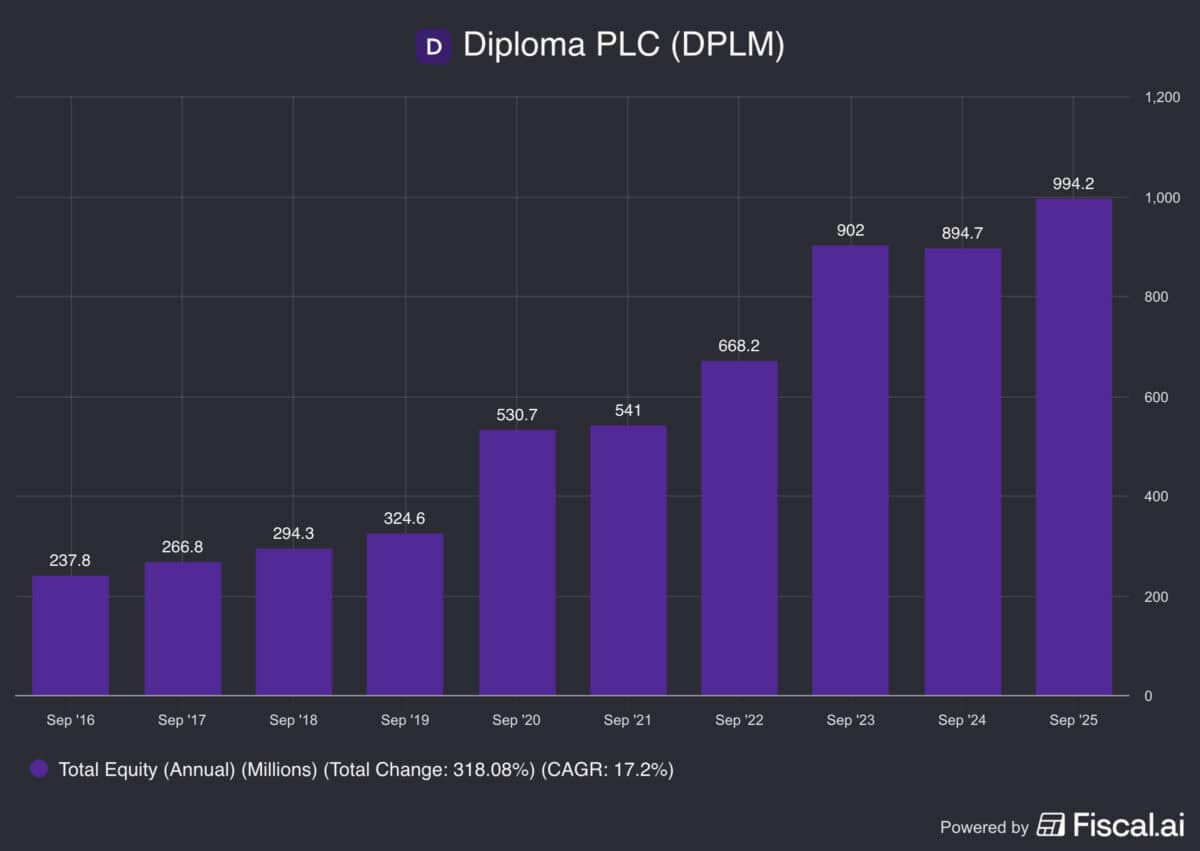

One inventory I’m preserving a detailed eye on is Diploma (LSE:DPLM). The commercial distributor is an especially high-quality enterprise that appears costly proper now – however that would change.

Acquisitions are a key a part of the enterprise mannequin and this brings a danger of overpaying. And the corporate has been paying larger costs not too long ago, which is price keeping track of.

Regardless of this, the agency’s file is excellent. With Diploma retaining most of its money (as an alternative of paying dividends) adjustments in e-book worth are a key metric to give attention to when it comes to progress.

From this angle, the final 10 years have been an enormous success – annual progress has been 17% on common. And I feel there’s extra to return, however the difficulty proper now could be value.

Shopping for

The factor with Diploma is that its progress hasn’t been linear. However each time it seems prefer it could be stalling, a excessive price ticket means the share value can fall sharply.

When e-book worth stagnated in 2021, the inventory fell 35% within the first half of 2022. And it fell 21% in early 2025 after a gentle, however unspectacular, efficiency in 2024.

I’m positive this may occur once more and I’m seeking to be prepared when it does. However a inventory market crash may also do the job simply as nicely when it comes to producing a possibility for me.