Picture supply: Getty Pictures

Constructing a second revenue could really feel out of attain for anybody ranging from scratch at 45. However with 20 years forward till retirement, traders nonetheless have time to place compounding to work — and doubtlessly construct a £17,360 annual revenue stream in later life.

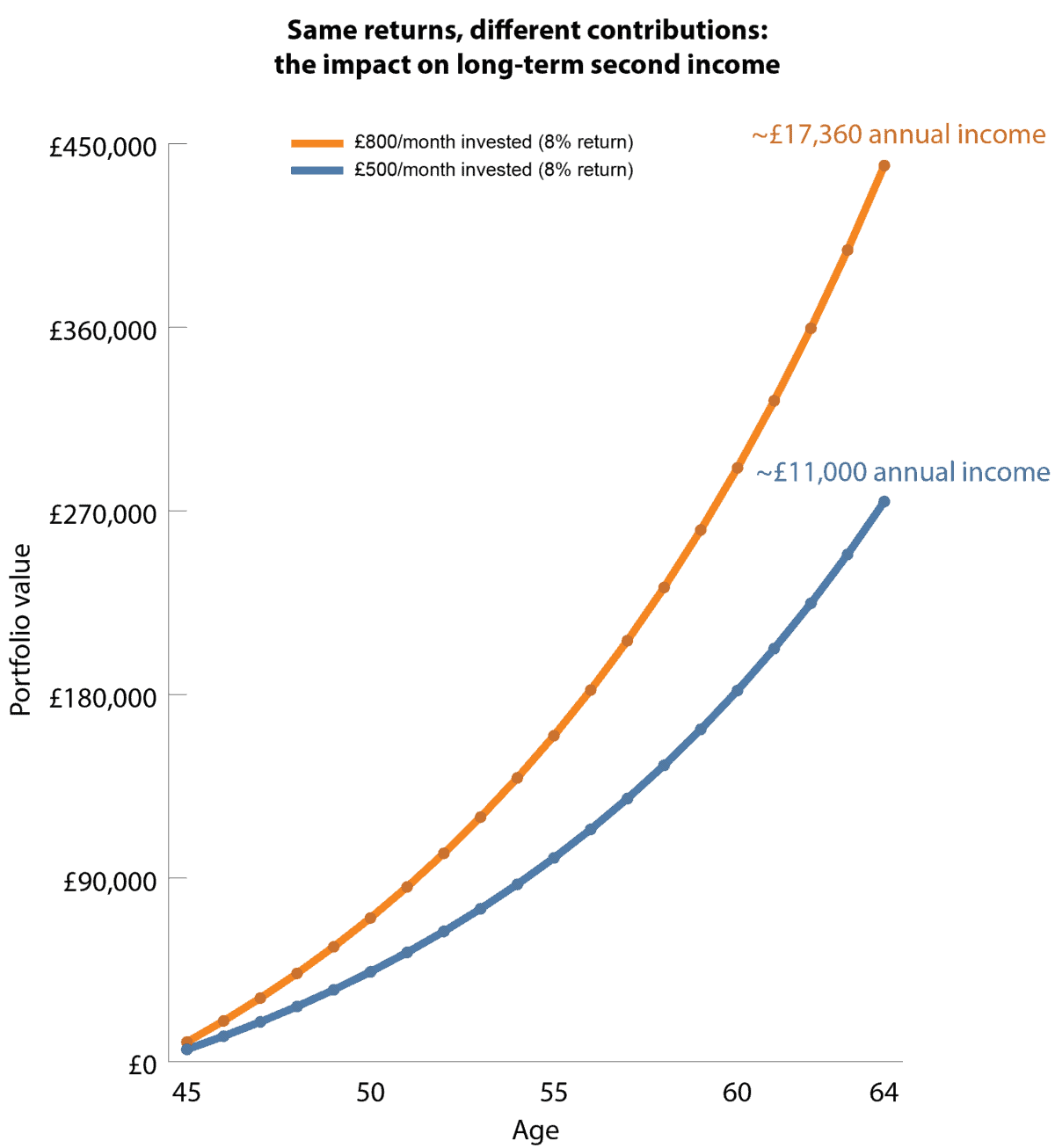

Beginning later in life doesn’t imply constructing a second revenue is solely a case of investing extra every month. Whereas larger contributions will help, the true driver of long-term wealth is how lengthy cash is invested and the way successfully it compounds over time.

Making up for misplaced time

Importantly, each situations within the chart beneath assume the identical annual return of 8%. In different phrases, the speed of compounding is similar in every case.

Even with a 20-year horizon, these results can nonetheless be highly effective. The secret is getting cash into the market and permitting returns to construct on themselves, reasonably than leaving money on the sidelines.

The chart beneath isn’t nearly contribution ranges. As an alternative, it highlights how placing more cash to work earlier — and protecting it invested — can considerably improve the revenue a portfolio is able to producing over time.

Chart generated by writer

The important thing takeaway is that each portfolios develop on the identical charge. Nevertheless, the upper month-to-month contribution merely ends in a bigger pool of capital for that very same compounding impact to work on over time.

A gradual revenue compounder

Headline-grabbing yields don’t come a lot larger than Authorized & Common (LSE: LGEN). With a ahead dividend yield of round 8.2%, the enchantment for income-focused traders is apparent. However the true attraction lies within the consistency of the money era behind it.

The group just isn’t merely paying out a excessive dividend; it’s working a enterprise mannequin constructed round long-term pension threat switch, annuities, and asset administration. That creates extremely predictable, recurring money flows that assist each dividends and buybacks over time.

FY25 outcomes mirrored that resilience. Core working earnings per share rose 9%, sitting on the high finish of the agency’s long-term 6%-9% progress goal vary, whereas the Solvency II protection ratio remained robust at 203%. Shareholder returns had been additional underpinned by a £1.2bn share buyback, funded largely via portfolio optimisation.

Trying forward, structural demand within the UK retirement market stays a key driver. Outlined contribution pensions are nonetheless increasing, and demand for annuity and pension threat switch options is anticipated to stay robust over the long run. The corporate additionally retains visibility on a major pipeline of potential offers, supporting medium-term revenue stability.

Nevertheless, dangers stay. As an asset-heavy insurer, it’s uncovered to actions in bond markets and credit score situations. A sustained rise in defaults or a pointy deterioration in mounted revenue valuations may stress each earnings and dividend capability. Likewise, weaker fairness markets may scale back property underneath administration and charge revenue.

Regardless of this, the core enchantment stays unchanged: a high-yielding enterprise with comparatively seen money era, returning capital steadily via cycles reasonably than counting on quick bursts of progress.

Backside line

The chart above illustrates the facility of compounding in constructing a second revenue over time. Authorized & Common operates on an analogous precept internally: constant money era is reinvested into shareholder returns, primarily via dividends and buybacks, permitting traders to profit from compounding at each the portfolio and enterprise degree.