NNOX|EPS -$0.17 vs -$0.20 est (+15.0%)|Rev $3.7M|Internet Loss $33.4M

Inventory $2.16

EPS YoY +0%|Rev YoY +23.0%|Internet Margin -903%

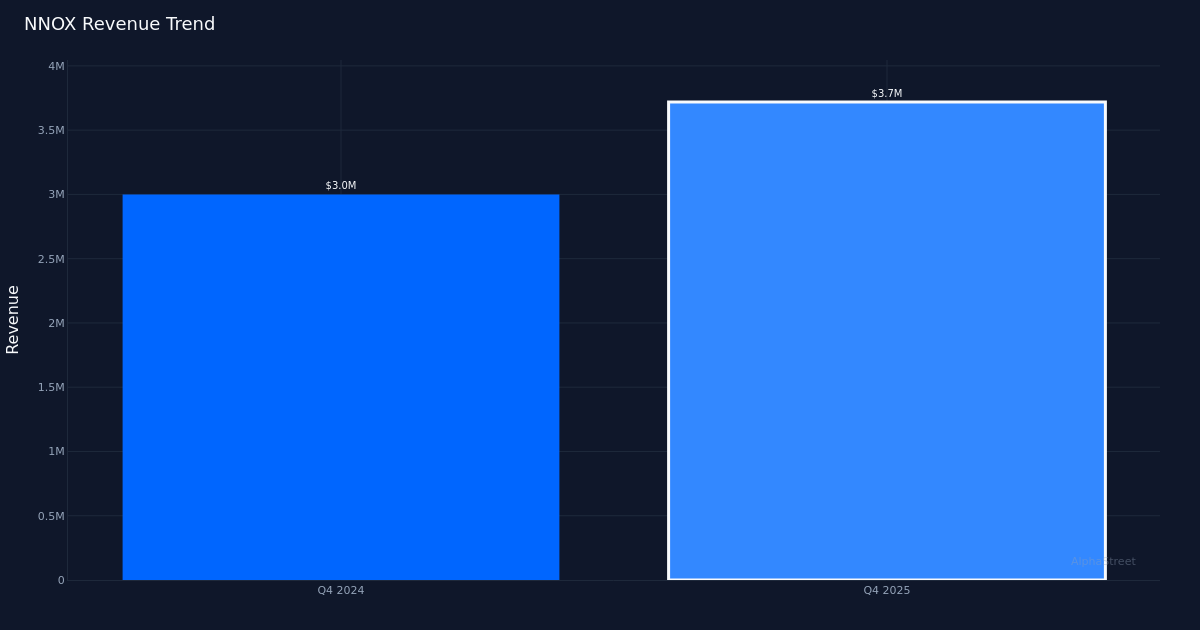

Nano-X Imaging topped expectations with a narrower-than-expected loss in This autumn 2025, however the high quality of the beat reveals deeper structural challenges masked by non-operating objects. The medical machine maker posted a lack of $0.17 per share versus the $0.20 loss anticipated by analysts, representing a beat by 15.0%. Whereas the corporate delivered its first earnings shock in latest quarters—attaining a 100% beat price over the past quarter—the underlying fundamentals paint a extra complicated image than the headline quantity suggests. Income reached $3.7M for the quarter, up 23% year-over-year, but the corporate’s margin construction deteriorated considerably regardless of the top-line enlargement.

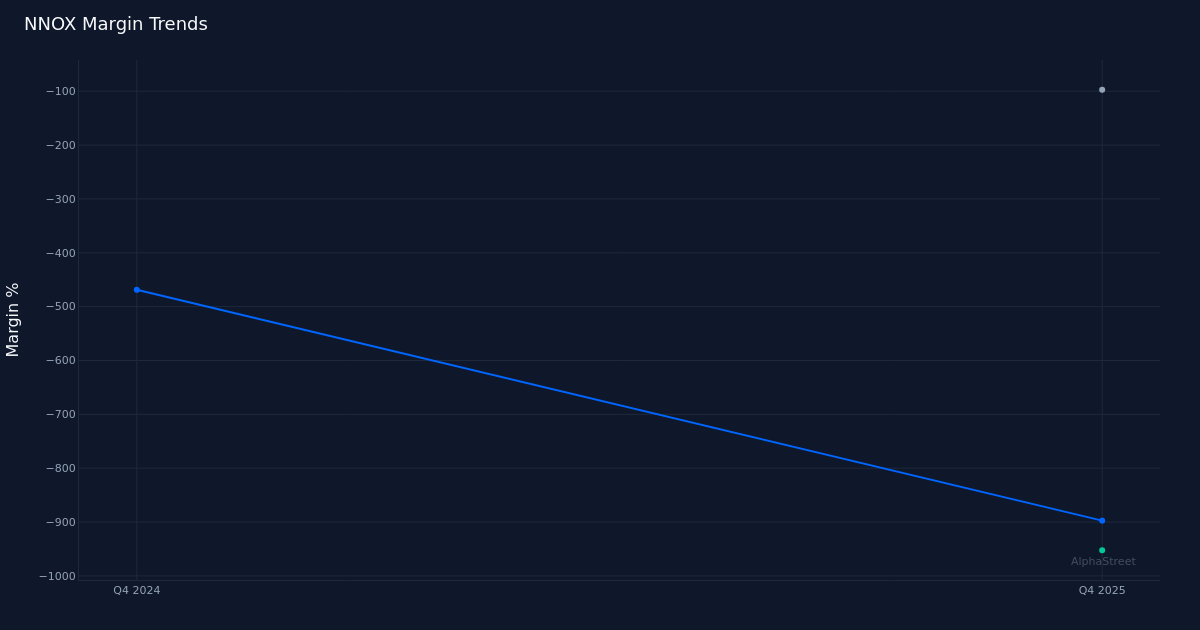

The earnings high quality evaluation reveals a troubling disconnect between income development and profitability metrics. Whereas income expanded from $3.0M in This autumn 2024 to $3.7M within the present quarter, gross margin plunged to -97%, indicating the corporate misplaced practically a greenback on each greenback of income generated on the gross revenue degree. The online margin of -902.7% in comparison with -470.0% a yr in the past represents a compression of 432.7 proportion factors, suggesting the enterprise mannequin stays removed from financial viability regardless of scaling efforts. Working margin deteriorated to -957.2%, with working loss registering at $35.4M. Administration acknowledged the margin stress, noting “The increase was also due to an increase of $0.7 million in the gross loss, increase of $1.1 million in the sales and marketing expenses and increase of $1.4 million in other expenses.”

Income composition reveals diversification efforts are starting to bear fruit, albeit from a low base. Administration attributed the expansion to a number of sources, explaining “The increase of $0.7 million, increase of 23% in the revenues, stems from an increase of $0.3 million in our revenue from the teleradiology services and an increase of $0.4 million in our revenue due to the consolidations of Nano-X Health IT Inc.” The teleradiology companies enlargement and the Well being IT consolidation collectively account for the complete year-over-year enhance, suggesting the corporate is broadening its income streams past pure {hardware} gross sales. The deployment metric of 36 Nanox.ARC techniques supplies a tangible indicator of market penetration, although the comparatively modest put in base underscores the early-stage nature of commercialization.

Administration’s FY 2026 steering implies a dramatic inflection that can require scrutiny. The corporate guided to $35.0M in income for the complete yr 2026, which might symbolize a virtually tenfold enhance from the quarterly run price of $3.7M. An analyst probed this in the course of the name, asking “when we look at the guidance for 2026, the $35 million, which is strong growth, can you talk about the cadence throughout the year?” The magnitude of implied acceleration suggests both an enormous deployment ramp, important one-time contracts, or further M&A consolidation—none of which have been quantified within the accessible information. This steering hole presents execution threat that buyers might want to monitor intently by way of 2026.

Non-operating objects considerably distorted reported outcomes and obscure underlying operational efficiency. CFO Ran Daniel disclosed a significant non-cash cost, stating “Besides the impairment expense that we recorded in 2025, which was the impairment of mainly whatever is related to the chip line in the Korean fab, which was amounted to $17.5 million in the non-cash expense.” This impairment alone exceeds annual income steering and suggests writedowns of producing infrastructure. The presence of such giant non-cash expenses makes it tough to evaluate true operational money burn and raises questions on prior capital allocation choices.

Market response. At present ranges, the market is pricing in profitable execution of the multi-fold income ramp whereas discounting the margin deterioration and capital depth questions raised by the Korean fab impairment. The valuation a number of on ahead steering seems modest, however provided that administration can bridge the hole between present quarterly income of $3.7M and full-year targets of $35.0M.

The trail ahead hinges on demonstrating unit economics at scale and managing money consumption. With 36 techniques deployed and gross margins deeply destructive, every incremental deployment at present destroys worth on the gross revenue degree. The corporate should show that these economics enhance dramatically with scale, or that the teleradiology and IT companies income streams carry materially totally different margin profiles. The gross sales and advertising and marketing expense will increase referenced by administration counsel continued funding in market improvement, which is acceptable for a growth-stage firm however extends the timeline to profitability.

What to Watch: Q1 2026 income would be the first check of whether or not administration can ship on the $35.0M annual steering, requiring quarterly run charges to just about triple from present ranges. Monitor Nanox.ARC deployment velocity past the present 36 items and any disclosure of unit economics or gross margin trajectories. Money burn price and stability sheet energy can be important given the -902.7% web margin, notably in gentle of the $17.5M impairment cost. Any updates on teleradiology companies development and Well being IT consolidation advantages will make clear whether or not these segments can offset {hardware} margin stress. Lastly, look ahead to clarification on the Korean fab writedown and what it alerts concerning the firm’s manufacturing technique going ahead.

This text was generated with the help of AI expertise and reviewed for accuracy. AlphaStreet might obtain compensation from corporations talked about on this article. This content material is for informational functions solely and shouldn’t be thought of funding recommendation.

This autumn Earnings: Misses on EPS, Income Recap – Alphastreet")