Picture supply: Getty Pictures

The FTSE 250 stays filled with sensible reductions as we transfer into the festive season. The inventory market volatility we’ve skilled in current weeks has seen much more high corporations transfer into discount basement territory.

Take the next FTSE 250 shares: QinetiQ (LSE:QQ.), Softcat (LSE:SCT), and TBC Financial institution (LSE:TBCG). Every now trades on a rock-bottom earnings a number of following heavy worth falls.

Might they rebound in December?

Defence discount

UK defence shares like QinetiQ have fallen sharply in current days. The prospect of peace in Ukraine could be welcome after years of bloodshed. However it might have important affect on protection sector earnings if gross sales hunch afterwards.

The low valuation on QinetQ shares particularly could assist it to rebound on this occasion. A 16% share worth drop during the last month leaves it on a ahead price-to-earnings (P/E) ratio of simply 13.7 occasions. This is among the lowest multiples throughout the European defence sector.

QinetiQ’s share worth additionally instructions a P/E-to-growth (PEG) ratio of 0.8. A studying under 1 implies a share goes mega low-cost.

Tech star

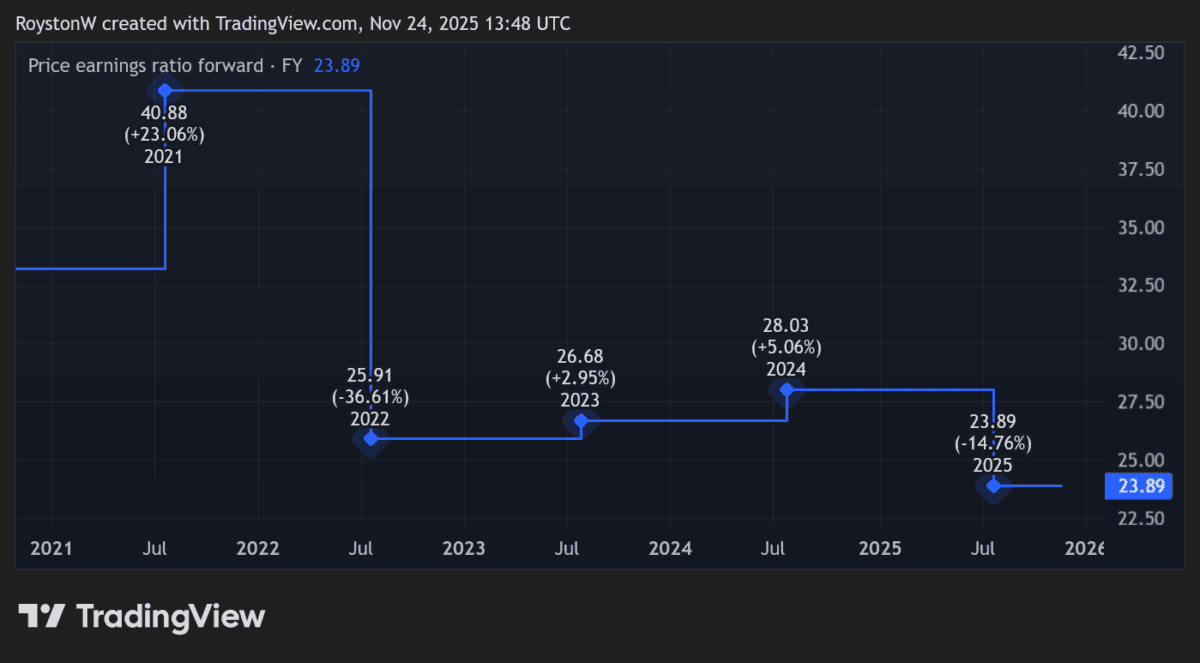

Fears of an AI bubble have unfold throughout the broader tech sector in current weeks. Data expertise supplier Softcat has sunk 13% as buyers have lowered or closed out positions.

It’s a decline I feel deserves severe consideration from discount hunters. The enterprise trades on a ahead P/E ratio of 19.7 occasions.

Because the chart exhibits, that is traditionally a rock-bottom score for Softcat shares.

Supply: TradingView

Supply: TradingView

My view is that worries over the AI sector have been overblown, as Nvidia‘s blowout results last week showed. I’m backing Softcat to rebound when market sentiment stabilises.

Over the long-term, I’m assured the corporate might surge in worth as growing digitalisation drives gross sales. That’s regardless of the specter of rising prices and competitors from US tech shares. Softcat’s share worth has rocketed 410% since November 2020.

Discount financial institution

TBC Financial institution has lengthy been one of the eye-catching FTSE 250 worth shares. Having declined 10% during the last month, it’s now a discount I feel deserves severe consideration from buyers.

Its ahead P/E ratio is 5.4 occasions. That makes it the most cost effective UK-listed financial institution share, properly behind the likes of Lloyds (11.9 occasions) and HSBC (9.8 occasions), for example.

Moreover, a 6.6% dividend yield for this yr is among the sector’s highest.

The financial institution’s shares have dropped after it stated full-year earnings will undershoot prior forecasts. Present issues embrace regulatory modifications which have launched a cap on microloans, a key marketplace for the corporate.

I feel TBC might spring again as buyers get up to its distinctive all-round worth