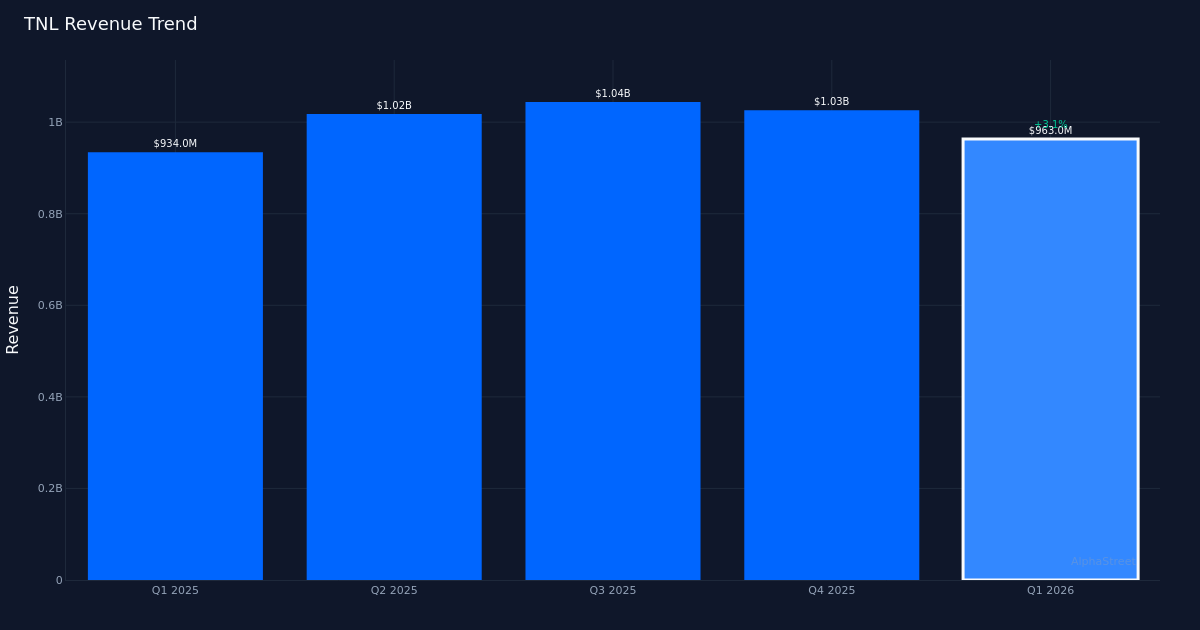

TNL|EPS $1.45 vs $1.32 est (+9.8%)|Rev $961M|Web Earnings $79.0M

Inventory $67.55 (-11.2%)

Stable Beat. Journey + Leisure Co. (NYSE:TNL) delivered Q1 2026 adjusted diluted earnings per share of $1.45, surpassing analysts’ $1.32 forecast by 9.8%, marking a robust begin to the 12 months for the holiday possession and journey companies supplier. Income totaled $961M for the quarter, up 2.8% from $934M in Q1 2025, demonstrating the corporate’s skill to capitalize on sustained shopper demand for leisure journey experiences. Backside-line revenue got here in at $93M on an adjusted foundation as the corporate balanced development investments with operational effectivity.

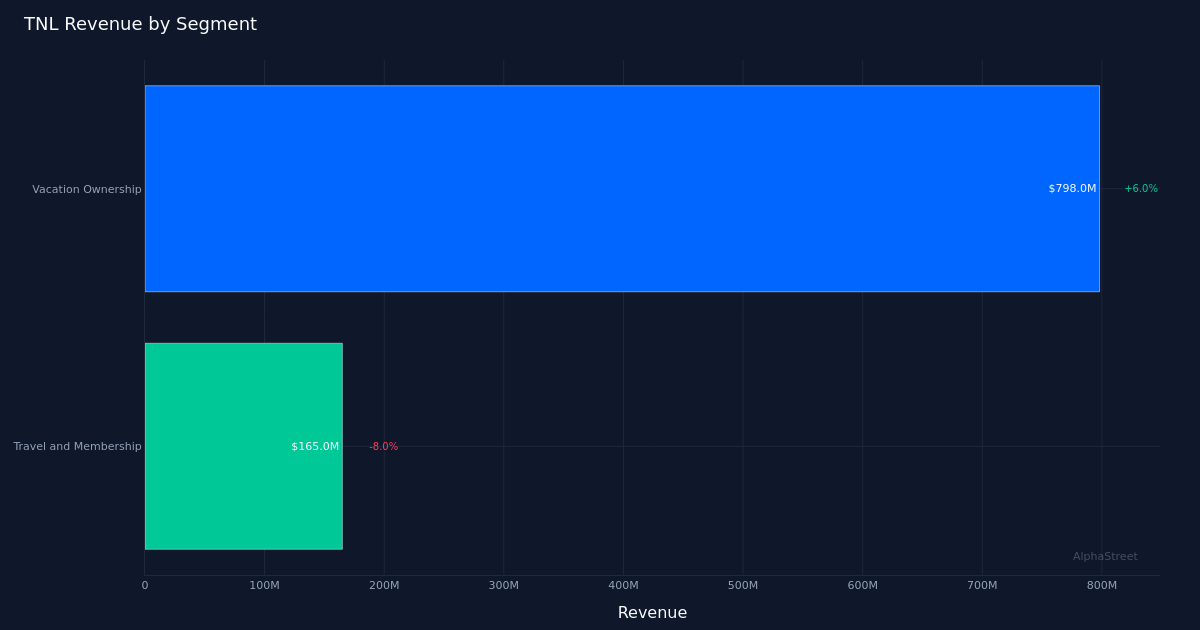

Income-Pushed Efficiency. The earnings beat seems basically sound, pushed by topline development relatively than aggressive cost-cutting measures. The two.8% income growth displays real enterprise momentum throughout the corporate’s trip possession platform, with Trip Possession main the way in which at $798.0M in income, up 6.0% year-over-year. This phase’s efficiency underscores the continued enchantment of timeshare and trip membership merchandise to shoppers searching for predictable leisure choices. Gross VOI gross sales reached $549.0M for the quarter, indicating wholesome buyer acquisition and improve exercise inside the present proprietor base.

Operational Execution. The corporate operated 161,000 excursions throughout the quarter, demonstrating its continued deal with changing potential consumers via face-to-face gross sales shows. This metric is especially necessary for Journey + Leisure’s enterprise mannequin, as excursions function the first buyer acquisition channel for trip possession merchandise. The power to take care of tour quantity whereas driving income development suggests bettering conversion charges or greater transaction values, each constructive indicators of pricing energy and gross sales drive productiveness within the present working atmosphere.

Market Response. Regardless of the earnings beat, TNL shares fell 11.2% to $67.55 following the discharge, suggesting buyers could also be involved about ahead steering, margin trajectory, or broader macroeconomic headwinds affecting discretionary shopper spending. The disconnect between operational outcomes and inventory efficiency might additionally replicate profit-taking after a latest run-up or sector rotation away from shopper discretionary names. Wall Avenue consensus stands at 8 purchase, 3 maintain, and 0 promote rankings, indicating analysts keep typically constructive outlooks on the corporate’s fundamentals regardless of the quick worth motion.

What to Watch: Traders ought to monitor tour quantity tendencies and VOI gross sales conversion charges in Q2 to evaluate whether or not shopper urge for food for trip possession merchandise stays resilient amid financial uncertainty. The corporate’s skill to maintain mid-single-digit income development whereas sustaining or increasing margins can be vital to validating present valuation multiples.

This text was generated with the help of AI know-how and reviewed for accuracy. AlphaStreet might obtain compensation from corporations talked about on this article. This content material is for informational functions solely and shouldn’t be thought-about funding recommendation.