Picture supply: Getty Photos

By mid-afternoon at this time (20 March), the JD Wetherspoon (LSE:JDW) share value was down round 10% as buyers digested the group’s outcomes for the 26 weeks ended 25 January.

The rationale? Properly, this a part of the press launch didn’t assist:

“There is clearly considerable pressure on consumer finances, combined with higher taxes, wages and energy costs for the hospitality industry. This may result in profits that are slightly below current market expectations.”

However I feel the Metropolis could have over-reacted. Let me clarify.

Simpler methods to make cash

You don’t have to look at EastEnders to know that working a pub is tough. Nonetheless, simply think about the issues that Wetherspoons’ boss, Tim Martin, has to deal with. In any case, he has 747 boozers to fret about.

However I really like the truth that he’s by no means shy in explaining the problems that the trade, and his chain specifically, are dealing with. This morning’s announcement is not any totally different.

With cautious reasoning – supported by some insightful numbers — he defined how enterprise charges for Scottish pubs have develop into a “de facto sales tax”, highlighted the “plethora of stealth taxes (non-domestic electricity charges, climate change levies, packaging charges, etc)” positioned on his enterprise, and argued for “VAT equality” with supermarkets.

And that is earlier than we all know how the battle within the Gulf goes to have an effect on disposable incomes and whether or not the pub chain’s margin would possibly come underneath strain from rising prices.

Total, earnings per share (EPS) for the interval fell 32.7% to 18.7p.

Not all dangerous

In the course of the interval, like-for-like (LFL) gross sales elevated 4.8% in comparison with a yr earlier. Income was additionally up 5.7%.

In February, trade LFL gross sales had been down 0.2%. For the forty second consecutive month, Wetherspoons outperformed the broader market with an increase of three.2%. Gross sales per pub elevated 35.4%.

And the drop within the group’s share value means its inventory is, on paper not less than, attractively priced.

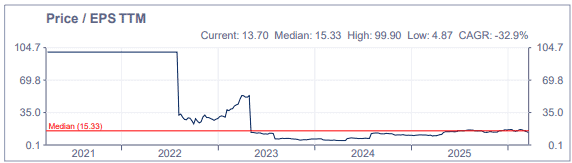

EPS for the yr to 25 January was 50.9p, giving a present price-to-earnings ratio of simply 10.8. Earlier than at this time, the five-year common (median) was 15.3.

Supply: London Inventory Trade Group/EPS TTM = earnings per share trailing 12-months

Supply: London Inventory Trade Group/EPS TTM = earnings per share trailing 12-months

It’s an identical story with regards to the group’s steadiness sheet. Since March 2021, its price-to-book ratio has averaged 2.3. It’s now 1.86.

To be trustworthy, I feel at this time’s 10% drop within the group’s market cap is somewhat unfair. In any case, the group hasn’t mentioned that its full-year revenue will likely be beneath expectations. It mentioned it “may” be.

So does this imply it’s time to bag a cut price?

Properly, it relies upon. If I knew with an inexpensive diploma of certainty that the autumn within the group’s earnings is a brief phenomenon then I’d say ‘yes’. However given all the issues that Tim Martin lists in his chair’s assertion, I can’t make certain.

Primarily based on its income, JD Wetherspoon is clearly doing higher than the trade as a complete. Pubs are closing in every single place and but ‘Spoons continues to develop. With its low-cost foods and drinks, outstanding excessive avenue areas, and robust model it has heaps going for it.

However taking a stake now can be too dangerous for me. I wish to see an enhancing backside line earlier than parting with my cash. Once I see proof of this, I shall revisit the funding case.