Picture supply: Getty Pictures

A £1,000 month-to-month passive revenue — £12,000 a 12 months — seems like one thing reserved for individuals who have already got some huge cash. However that’s not the case.

With a Shares and Shares ISA and a protracted sufficient runway, it’s a sensible goal for abnormal traders. The mechanism that makes it attainable is compounding, and it’s price understanding correctly earlier than we get to the numbers.

Begin early, consider in compounding

Compounding is solely what occurs when returns construct on earlier returns. Reinvest a dividend (or spend money on progress shares that basically do this for you — they reinvest the corporate’s earnings) and subsequent 12 months you’re incomes revenue on a barely bigger holding. Watch a share value rise and future beneficial properties come off a better base. Nothing sophisticated — however give it 10 years and the impact turns into very noticeable certainly.

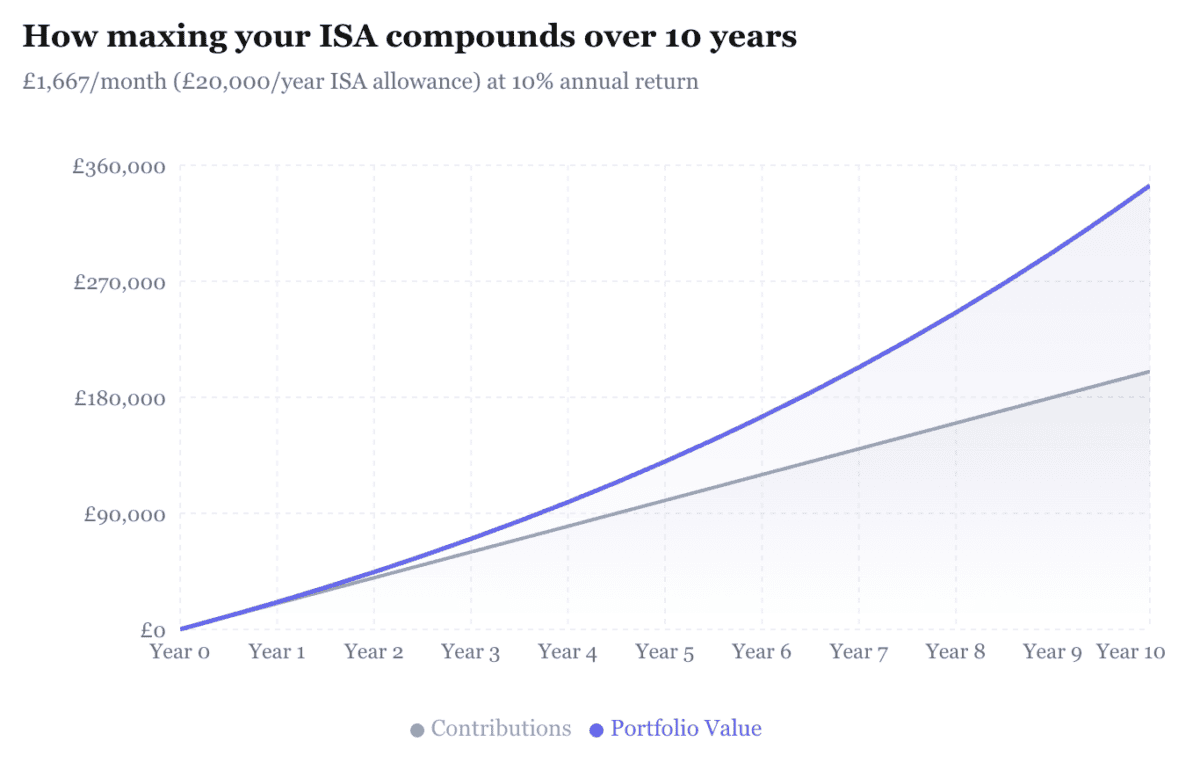

Nevertheless, compounding begins to indicate after a comparatively brief time period.

The annual ISA allowance is £20,000, so somebody maxing it out every year would have put in £200,000 over a decade earlier than funding returns are even thought-about. At a ten% annual return — roughly what world fairness markets have averaged traditionally, although with loads of bumpy years alongside the way in which — common month-to-month contributions of round £1,667 would compound to round £300,000 over 10 years.

Created with Claude

Created with Claude

So how a lot do you really must hit £12,000 a 12 months? The reply is determined by the yield. Personally, I consider a 5% dividend yield may be very achievable and sustainable with the proper shares. That may recommend an traders wants £240,000 in a portfolio.

No dividends are assured and markets don’t transfer in straight traces… however that is the idea.

Placing that cash to work

Past the idea, novice traders want to contemplate the place to place that cash to work. Combining diversification and conviction is a well-liked technique. Development-oriented shares are arguably one of the simplest ways to develop the dimensions of the portfolio — however threat may be better right here.

One inventory I discover genuinely compelling proper now could be Sanmina Company (NASDAQ:SANM). The US-listed electronics manufacturing specialist sits on the intersection of cloud computing, AI infrastructure, and superior industrial methods — and but the market doesn’t seem to have absolutely priced that in.

The shares commerce at round 11.7 instances ahead earnings, roughly 45% under the sector median. With medium-term earnings progress estimated close to 26% yearly, the implied price-to-earnings-to-growth (PEG) ratio of round 0.49 suggests the expansion story isn’t absolutely mirrored within the value.

For context, Celestica — a really comparable enterprise I invested in over three years in the past — now trades at 29 instances ahead earnings after rising greater than 3,000% in 5 years. Sanmina seems to be like Celestica did earlier than the market caught on.

The principle threat is the stability sheet. The pending acquisition of ZT Techniques’ information centre manufacturing enterprise from AMD will push internet debt in the direction of $2bn, leaving the corporate extra uncovered if AI spending slows.

That stated, I completely assume this firm’s price contemplating.