Goldman Sachs has quietly dropped a uncommon inventory market forecast, which stretches all the way in which to 2035, whereas delivering a twist most U.S. buyers received’t love.

Following a decade that has been outlined by tech-fueled features together with increasing valuations, Goldman feels the subsequent decade will look remarkably totally different.

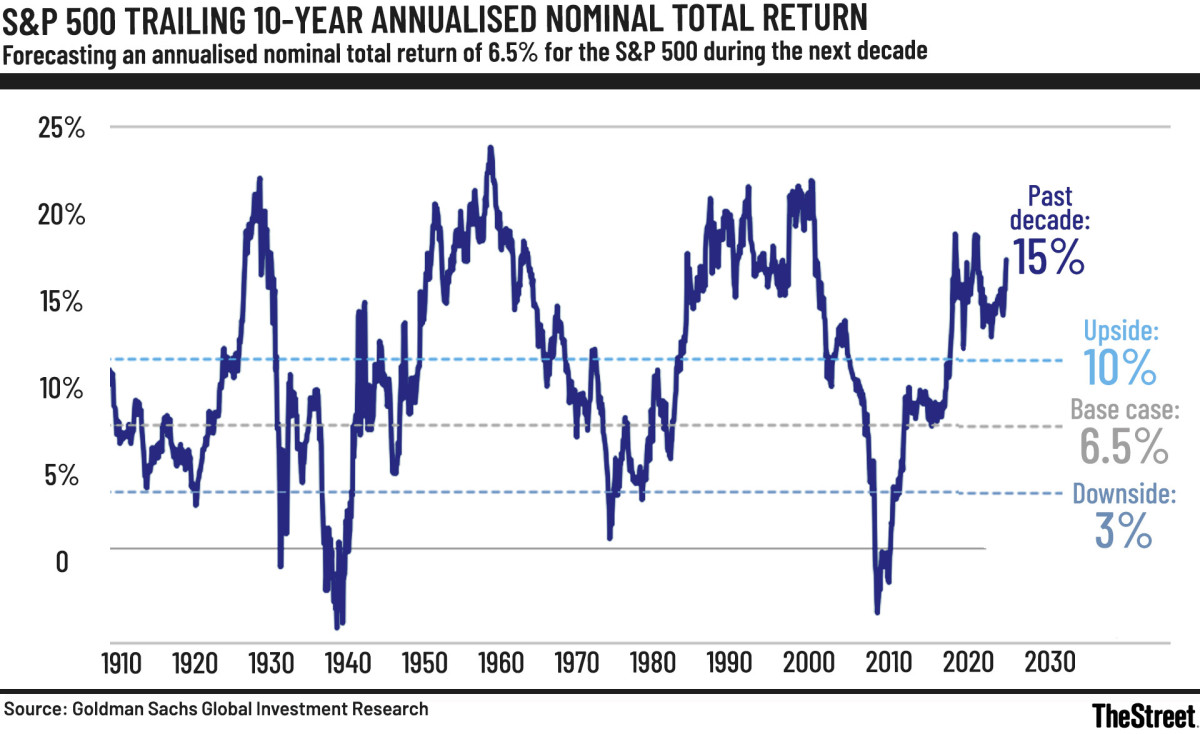

The financial institution forecasts only a 6.5% annual return for the S&P 500, a stark distinction from the standard double-digit run to which most buyers have change into accustomed.

Earnings, and never a number of enlargement, will likely be delivering the majority of these lofty features, a shift signaling a extra “normal” market setting forward.

Nevertheless, the larger shock is the place Goldman sees the largest alternatives. As an alternative of the same old Silicon Valley-led outperformance, the agency feels the largest upside will come from locations U.S. buyers are likely to overlook.

Goldman Sachs expects international shares to return 7.7% yearly via 2035, pushed largely by earnings progress.

Picture by Aditya Vyas on Unsplash

A inventory market outlined by earnings, not exuberance

Goldman’s perspective is generally easy.

The times when pricing multiples could be doing all of the heavy lifting are nearly over.

Lengthy-term S&P 500 trailing returns chart

The agency’s 6.5% return prediction solely is sensible as soon as we look at the underlying math, which includes regular 6% earnings progress, a light valuation headwind, and a modest dividend yield.

It’s a reminder that the subsequent 10 years received’t reward buyers for chasing the euphoria however will reward companies that constantly develop, worth neatly, and ship actual outcomes.

The tip of the multiple-expansion period

Goldman’s valuation name is blunt.

The agency believes that right this moment’s P/E ranges are “very high relative to history,” which, extra importantly, can’t be sustained as soon as the structural tailwinds that had been turbocharging margins fade away.

Their up to date mannequin now suggests a fair-value price-to-earnings ratio of 21x by 2035, which factors to a gradual pullback from the present 23x ratio.

Associated: Jim Cramer delivers pressing tackle the inventory market

Their logic primarily rests on a few constraints.

Firstly, revenue margins are already close to report highs after leaping from 5% in 1990 to roughly 13% right this moment. That enhance was primarily pushed by international provide chain efficiencies, in addition to many years of declining curiosity and tax bills. Goldman feels these tailwinds are unlikely to repeat.

Extra Wall Avenue:

- Veteran fund supervisor sees quiet gasoline for subsequent AI rally

- The 60/40 portfolio is again for a stunning motive

- High analyst calls ‘kick in the pants’ for S&P 500

Secondly, the agency embeds a 4.5% 10-year Treasury yield into its framework, which leaves nearly nothing for valuations to develop from right here.

Therefore, the result’s principally a decade that’s outlined by earnings, and never a a number of stretch.

Earnings maintain crushing expectations

Furthermore, Goldman’s name lands at a degree when company America continues to overdeliver. It has seen back-to-back quarters of broad earnings beats, which reveals that the engine is working hotter than most anticipated.

- Q2 wasn’t precisely a “Mag 7” mirage, however was extra of a full-on earnings improve. By August, 66% of the S&P 500 reported, and 82% ended up beating EPS estimates whereas 79% beat on gross sales. Blended EPS progress struck even greater at 10.3% yr over yr, greater than 50% the pre-season 2.8% forecast.

- Q3 saved the momentum going. Two-thirds of companies have already reported, with 83% beating EPS estimates whereas 79% topped gross sales forecasts, comfortably above five- and 10-year averages. The index appears to be on observe for 10.7% earnings progress, its fourth straight quarter of double-digit bottom-line features.

- Large Tech is carrying the league. In each Q2 and Q3, eight of the S&P’s 11 sectors posted year-over-year earnings progress, whereas 10 sectors are rising gross sales, powering a 19- then 20-quarter streak of uninterrupted income enlargement.

U.S. buyers could also be wanting within the unsuitable place

Goldman’s long-term math makes a easy level for U.S. buyers in that the most effective returns of the subsequent 10 years will not come from the U.S. in any respect.

Although the S&P 500 posts a wholesome 6.5% baseline, Goldman highlights Rising Markets at +10.9%, Asia ex-Japan at +10.3%, and Japan at +8.2%.

Associated: Cathie Wooden dumps $30 million in longtime favourite

EM and Asian markets normally profit from extra sturdy nominal GDP enlargement together with structural reforms, together with rising payout ratios, which Goldman expects to raise EM dividend yields from 2.5% to three.2% by 2035.

Throw in governance upgrades in areas corresponding to Korea and China, and immediately these areas really feel like compounding machines.

The actual kicker, although, is forex.

Goldman’s FX strategists consider the U.S. greenback is 15% overvalued, forecasting a decade-long reversal that will raise USD-translated EM returns by 1.7% per yr. Traditionally, dollar-related weak point coincides with foreign-market outperformance.

Additionally, there’s earnings energy for buyers to contemplate.

EM EPS progress is spearheaded by China and India, which drives the ten.9% baseline return. Japan’s reforms are anticipated to drive earnings to 8.2% returns.

Associated: High analyst revamps S&P 500 goal for the remainder of the yr