DEA|EPS $0.77 vs $0.09 est (+755.6%)|Rev $91.5M vs $88.3M est (+3.7%)|Web Revenue $1.4M

Steering adjusted $3.06 – $3.12|Inventory $23.85 (+1.4%)

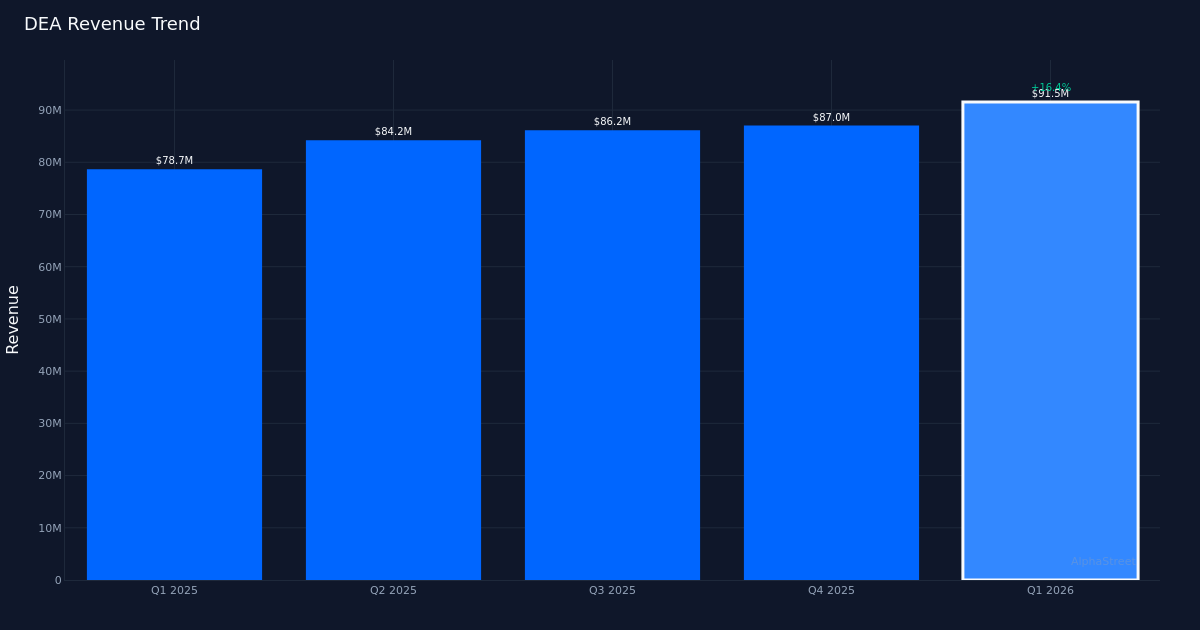

Blowout Quarter. Easterly Authorities Properties, Inc. (NYSE:DEA) delivered a shocking Q1 2026 efficiency, with Core FFO per share of $0.77 crushing analyst expectations of $0.09 by 755.6%. The federal government-focused workplace REIT generated income of $91.5M, exceeding Wall Road’s $88.3M forecast by 3.7%, whereas Core FFO totaled $37.1M for the quarter. The corporate continued capitalizing on steady authorities tenant demand throughout its specialised property portfolio.

Income-Pushed Efficiency. The quarter’s outperformance was basically sound, anchored by sturdy top-line enlargement fairly than aggressive value administration. Income of $91.5M represented a 16.3% improve from the $78.7M recorded in Q1 2025, demonstrating significant natural progress within the firm’s government-leased workplace section. This year-over-year acceleration suggests sustained demand from federal businesses for the purpose-built services that comprise Easterly’s portfolio, a very encouraging sign given broader workplace market headwinds affecting standard industrial properties. The corporate operated 106 working properties at quarter finish, offering a diversified base of income-generating property.

Full-12 months Outlook. Administration offered FY 2026 steerage with adjusted EPS projected between $3.06 and $3.12, establishing a transparent roadmap for continued profitability. The steerage vary suggests confidence within the sturdiness of presidency lease earnings streams and the corporate’s means to keep up occupancy ranges regardless of macro uncertainty. Given the substantial Q1 beat, the steerage framework seems conservative, doubtlessly leaving room for upward revisions because the yr progresses relying on acquisition alternatives and lease renewals throughout the portfolio.

Market Reception. Shares responded positively to the outcomes, climbing 1.4% to $23.85, although the modest acquire relative to the magnitude of the earnings beat suggests buyers could also be tempering enthusiasm amid broader considerations concerning the workplace sector. The muted response might additionally mirror Wall Road’s cautious stance on the title, with analyst consensus standing at 0 purchase rankings, 6 maintain rankings, and 5 promote rankings. This skeptical positioning signifies Road considerations about workplace fundamentals could also be overshadowing Easterly’s differentiated authorities tenant base and mission-critical property focus.

Strategic Positioning. Easterly’s specialised area of interest serving authorities businesses offers insulation from the work-from-home pressures plaguing conventional workplace landlords. The 16.3% income progress demonstrates the worth proposition of purpose-built services with long-term authorities leases, which usually characteristic minimal emptiness threat and contractual lease escalations. As federal area wants evolve, the corporate’s established relationships and security-enhanced properties place it to seize further demand, significantly for businesses requiring specialised infrastructure that can’t be simply replicated in standard workplace buildings.

What to Watch: Monitor lease renewal charges and lease spreads throughout the portfolio as present authorities contracts come up for renegotiation. Federal finances dynamics and potential modifications to company area utilization insurance policies might be important components figuring out whether or not Easterly can maintain double-digit income progress and justify a re-rating among the many skeptical sell-side analyst group.

This content material is for informational functions solely and shouldn’t be thought of funding recommendation. AlphaStreet Intelligence analyzes monetary knowledge utilizing AI to ship quick and correct market data. Human editors confirm content material.

on Christmas Day 2025 | Fortune")