Picture supply: Getty Photos

2025’s been a tricky time for Berkeley Group‘s (LSE:BKG) share price. Down 7% since 1 January, it’s dropped 30% over the past yr as worries over the housing market restoration have grown.

Might this symbolize a beautiful dip-buying alternative although? I believe it’s price inspecting, and particularly given the cheapness of Berkeley’s shares versus its FTSE 100-listed peer group.

As we speak, the corporate trades on a ahead price-to-earnings (P/E) ratio of 11.4 instances. That’s under corresponding readings of:

- 14 instances for Persimmon.

- 14.7 instances for Taylor Wimpey.

- 17.3 instances for Barratt Redrow.

Right here’s my take.

Nonetheless on target

The UK housing market stays robust because the home economic system splutters. But the business’s rebound from 2022’s meltdown stays intact, as decrease rates of interest and competitors within the mortgage market assist homebuyers.

Berkeley’s newest buying and selling assertion right now (5 September) revealed that it continues to make gradual however regular progress. It mentioned “trading has been stable… over the first four months of the year, following a similar pattern to last year.”

The agency maintained its pre-tax revenue steering of £450m for the 12 months to April 2026, albeit down from £528.9m within the earlier fiscal yr. And it mentioned 85% of anticipated full-year income have already been secured by exchanged gross sales contracts.

It added that “we anticipate pre-tax profits to be weighted broadly evenly between the first and second half of the year, subject to the timing of completions.”

Berkeley additionally confirmed it expects to report related income to the present yr in monetary 2027.

Inexperienced shoots

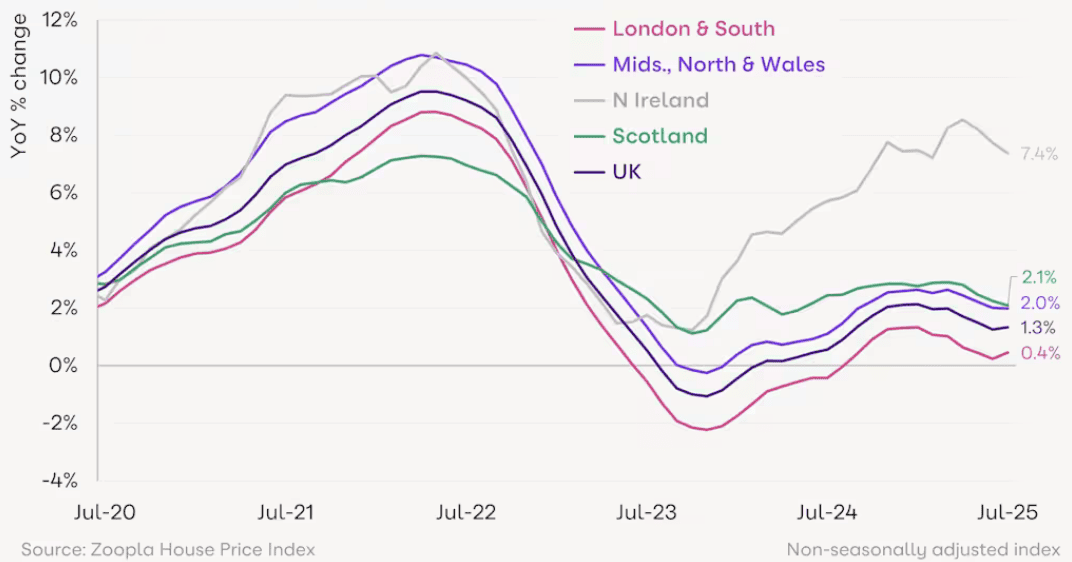

There’s little question Berkeley’s give attention to London and the South East has muted its restoration. An abundance of latest provide means dwelling worth progress within the capital and surrounding areas is lagging the remainder of the nation, as newest knowledge from Zoopla reveals.

Supply: Zoopla

Supply: Zoopla

However indicators are rising that circumstances in London are bettering because of a weaker improvement pipeline and beneficial demographic components (such because the regular return to the workplace following Covid-19).

Certainly, boffins at Capital Economics suppose costs within the capital will rise at a median of 6.5% in 2026. That beats the 5% rise predicted for the broader UK.

A continuation of the development that Capital Economics suggestions may pull Berkeley’s share worth sharply greater.

Progress alternative

There are after all dangers to those forecasts. Indicators of stickier inflation solid doubt on the tempo of future rate of interest cuts. Worrying financial indicators like rising unemployment additionally current trigger for concern.

However on stability, I nonetheless suppose Berkeley may very well be a beautiful choice for traders looking for restoration shares to think about. And particularly when one considers the cheapness of the builder’s shares.

I definitely stay upbeat concerning the housebuilder’s long-term prospects as inhabitants progress drives demand for brand spanking new houses. Statista analysts suppose the variety of Londoners will develop by nearly 700,000 between now and 2047 to 9.97m. And authorities plans to ease planning restrictions ought to assist Berkeley higher capitalise on this vital alternative.