Picture supply: Getty Photographs

I’m at all times looking out for prime development names for my ISA and Palantir (NASDAQ:PLTR) inventory would definitely qualify as a kind of.

That’s as a result of, since 2020, the software program firm’s income has swelled from $1.1bn to an anticipated $7.2bn this 12 months. Earnings have additionally exploded increased, sending the share value up by an eye-popping 1,469% over this time.

Do you have to purchase Palantir Applied sciences shares as we speak?

Earlier than you determine, please take a second to evaluation this report first. Regardless of ongoing uncertainties from Trump’s tariffs to international conflicts, Mark Rogers and his staff consider many UK shares nonetheless commerce at substantial reductions, providing savvy traders loads of potential alternatives to find out about.

That is why this could possibly be a super time to safe this invaluable analysis – Mark’s analysts have scoured the markets to disclose 5 of his favorite long-term ‘Buys’. Please, do not make any large selections earlier than seeing them.

Since November, nevertheless, the inventory has fallen 29%. Does this signify a terrific alternative so as to add Palantir to my ISA? Listed here are my ideas.

Accelerating development

In contrast to many software program corporations, Palantir doesn’t function a knowledge platform that clients simply take a look at. As an alternative, it builds software program that pulls collectively messy, scattered information and turns it into insights that decision-makers can act on shortly in actual time.

Whereas the agency lower its enamel within the defence and intelligence world, it’s the industrial facet that’s now having fun with explosive development. Its AIP (Synthetic Intelligence Platform), specifically, permits organisations to deploy giant language fashions (LLMs) safely on their non-public information.

In This fall, industrial income skyrocketed 137% to $507m. And Palantir closed 180 offers price no less than $1m and 61 offers of $10m or extra. Quarterly internet revenue was $609m, representing a 43% margin on whole income of $1.4bn.

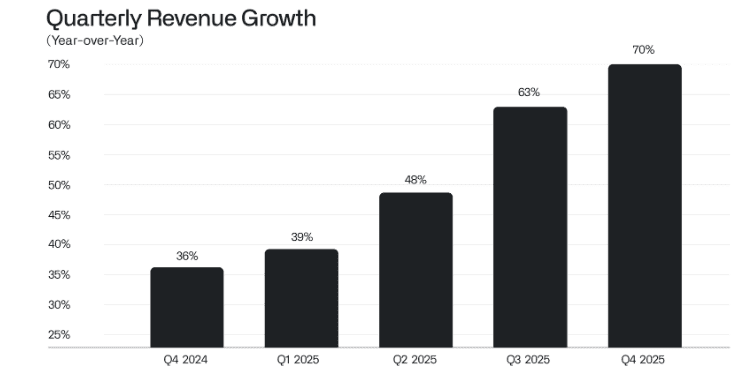

What has excited a number of traders — and despatched the inventory skywards — is that the corporate’s price of development has been accelerating in current quarters.

Supply: Palantir.

Supply: Palantir.

A polarising firm

Now, as spectacular as that is, I do have a few considerations. One is that Palantir is a politically polarising firm, with a bogeyman repute amongst many individuals.

On the weekend, for instance, the agency printed a 22-point put up on-line. This acknowledged that free and democratic societies wanted “hard power” with a view to prevail, in addition to predicting a future stuffed with autonomous AI weapons. Naturally, this induced a backlash in some quarters.

The query will not be whether or not AI weapons will likely be constructed; it’s who will construct them and for what goal. Our adversaries is not going to pause to take pleasure in theatrical debates in regards to the deserves of creating applied sciences with crucial navy and nationwide safety functions. They may proceed.

Palantir.

As a consequence of rhetoric like this, some liberal MPs are calling for the federal government to scrap the NHS’s £330m contract with Palantir. And with its expertise being extensively used within the Iran battle and by US Immigration and Customs Enforcement (ICE), extra controversy appears sure.

The second concern pertains to valuation. At current, Palantir has a large $353bn market cap, but is barely anticipated to generate round $7.2bn in income this 12 months. This implies it trades at a forward-looking price-to-sales ratio of virtually 50.

And whereas Wall Avenue analysts anticipate income to double between now and 2028, that is nonetheless an extremely dear inventory. If development unexpectedly slows, the valuation would virtually actually show unsustainable.

So what’s my transfer?

Palantir is undoubtedly an thrilling firm, with super-strong margins and an extended potential runway of development forward. The agency additionally has a particular company tradition that retains it innovating forward of rivals and centered on the long run.

Nevertheless, it’s additionally politically polarising, and I fear this will likely cut back its worldwide development prospects, particularly in Europe. With the inventory buying and selling very expensively, this isn’t one I’m trying to purchase for now.