Picture supply: Getty Pictures

The Lloyds Banking Group (LSE:LLOY) share value has gone from 55.04p to 97p in 2025. However the subsequent query for buyers is how a lot additional it may well run in 2026.

An analogous transfer once more subsequent 12 months would see the inventory attain £1.30. Rates of interest is likely to be set to come back down, however there are nonetheless causes for buyers to be optimistic.

Worth targets

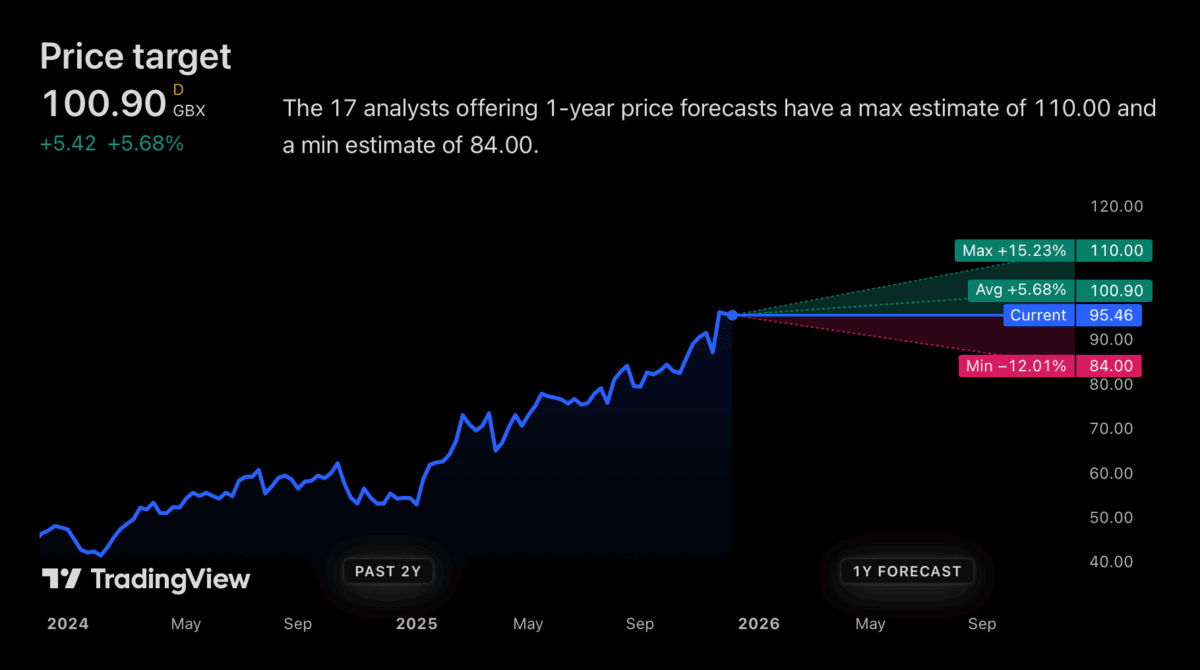

From what I can see, the analyst neighborhood isn’t anticipating a repeat efficiency from Lloyds in 2026. The very best value goal is round £1.10 – 16% above the present stage.

That wouldn’t be a foul consequence in any respect – it’s nicely above the FTSE 100 common. However the much less optimistic forecasts are projecting a share value decline of as a lot as 12%.

There are good causes for pondering that 2026 received’t be such a robust 12 months for the inventory. The obvious is the possibility of decrease rates of interest, which might be more likely to have an effect on lending margins.

Regardless of this, although, there are additionally causes for optimism. With a financial institution the dimensions of Lloyds, it’s not as easy as the corporate’s earnings falling if rates of interest get reduce.

Structural hedge

Like quite a few banks, Lloyds makes use of what’s generally known as a structural hedge. That is primarily a mixture of fixed-rate belongings (resembling bonds) with lengthy durations and rate of interest swaps.

These assist defend the financial institution within the brief time period if rates of interest fall. In different phrases, rate of interest cuts in 2026 shouldn’t imply the agency’s earnings falls away instantly.

In actual fact, decrease charges may imply higher margins in 2026. If the financial institution can scale back the curiosity on its financial savings immediately whereas mortgage charges stay fastened, this might give lending earnings a lift.

Larger charges are more likely to profit Lloyds over the medium time period. However I don’t suppose buyers ought to take the view that cuts in 2026 will instantly ship the agency’s earnings into reverse.

Rules

Wanting past 2026, there are additionally extra causes for Lloyds shareholders to be constructive. One is the potential for looser regulation giving the financial institution extra scope to lend.

For the primary time in 10 years, the Financial institution of England has determined to decrease the quantity of Tier 1 capital UK banks are required to carry. That is set to come back in from January 2027.

That ought to go away the likes of Lloyds with extra capital that can be utilized to develop mortgage books. Nevertheless it’s price noting that this may apply to all banks, so competitors may enhance.

Whereas banks usually keep capital ratios nicely above their authorized necessities, a decrease commonplace means extra scope for lending. And this might assist develop earnings past 2026.

Don’t be too hasty

Lloyds has been among the finest FTSE 100 shares to personal in recent times. And whereas cyclical forces have been a part of this, buyers shouldn’t be too fast to put in writing this one off in 2026.

Falling rates of interest are more likely to current a problem. However that is the form of factor the financial institution must be able to take care of – and its structural hedge suggests it’s.

Wanting additional forward there are causes to suppose the inventory could possibly be a great funding past 2026. Nevertheless it’s not my prime alternative because the New Yr approaches.