Picture supply: Getty Pictures

With rates of interest set to fall and geopolitical tensions sending shivers by way of markets, the outlook for UK shares is altering.

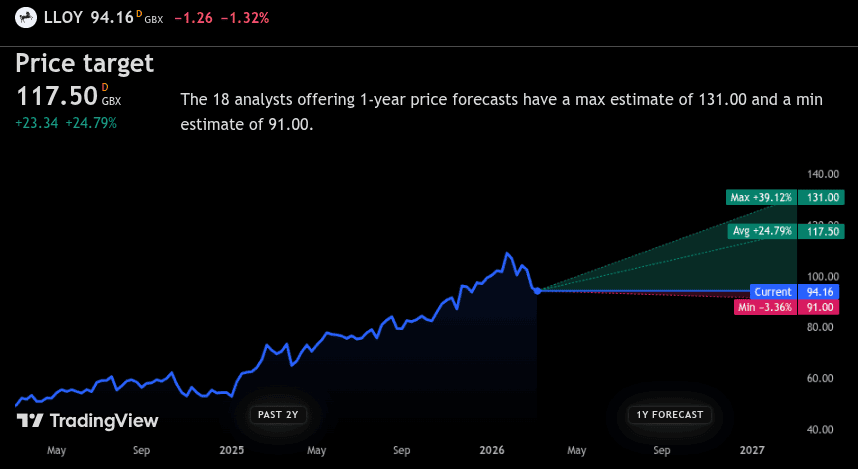

With Lloyds‘ (LSE: LLOY) shares usually thought of a bellweather for the home market, I made a decision to see the place analysts assume they could be heading within the coming yr.

Trying forward

Analysts following Lloyds have a median 12‑month value goal of 117.5p, which might be a 24.92% acquire from at the moment’s degree. If that performed out, £1,000 would develop to roughly £1,250 simply from the shares alone. Add the 6% dividend yield and the overall return may very well be near 30%, or round £1,300 (earlier than dealing prices and tax).

On the optimistic finish, some analysts assume the worth might climb about 39.27%. In that case, £1,000 might develop to roughly £1,390 from share value alone, or nearer £1,450 together with dividends.

Screenshot from TradingView.com

Screenshot from TradingView.com

On the pessimistic finish, the gloomiest forecast is for a 3.29% value fall. Even then, the dividend might nonetheless go away an investor roughly flat or barely forward over the yr.

To get a greater thought of the place it could be headed, I took a more in-depth look.

Key fundamentals and dividends

During the last 5 years, Lloyds’ share value is up round 125% — a fairly sturdy rally for a mature financial institution inventory. However income is the actual story right here, and a transparent indication of the advantages of a better rate of interest setting. It has greater than doubled since 2022, rising from £26.2bn to £65.55bn.

What does this imply for shareholders? Effectively, return on fairness (ROE) isn’t spectacular — it sits simply above 10%, broadly in step with many giant lenders. However the place Lloyds usually wins is earnings.

The inventory presently presents a dividend yield just under 6%, and payouts use solely about 52% of earnings — so that they’re properly lined. Plus, it’s backed up by 12 years of uninterrupted funds, including a level of reassurance for these concentrating on passive earnings.

Macro backdrop and dangers

As a largely home financial institution, Lloyds is closely uncovered to the well being of UK customers and companies. A key development driver in recent times has been rates of interest. However following a number of cuts, the Financial institution of England base price now sits round 3.75%, with additional cuts anticipated.

This presents a blended image for Lloyds. Decrease charges can squeeze lending margins, however additionally they assist the housing market and maintain dangerous money owed in verify. But when the financial system slows or unemployment rises sooner than anticipated, income might come beneath stress.

Nonetheless, it’s managed to pair dividends with sizable share buybacks.

Remaining ideas

For a UK investor seeking to open a brand new ISA in April, Lloyds nonetheless seems engaging. It’s an enormous, acquainted financial institution with a chunky dividend yield and analyst expectations are for modest share value development over the following yr. The financial institution’s worthwhile, properly capitalised and returning loads of money to shareholders.

Nevertheless, that is nonetheless a cyclical share tied carefully to the fortunes of the UK financial system. Anybody shopping for at the moment must be prepared for bumps alongside the way in which – particularly if development disappoints or the housing market turns.

For buyers snug with these dangers, it presents earnings plus some potential optimistic value motion. Nevertheless it’s simply certainly one of a number of high-yielding FTSE shares to contemplate on the UK market at the moment.