Booz Allen Hamilton Holding Company (BAH/NYSE), a U.S. administration and know-how consulting agency serving authorities and nationwide safety shoppers, shares had been buying and selling close to $95.76, up modestly in early session. The inventory has traded in a 52-week vary of $79 to $138 and carries a market capitalization of roughly $11.6 billion.

Share Influence

BAH shares rose barely following the discharge of third quarter fiscal 2026 outcomes, reflecting investor concentrate on stronger-than-expected earnings regardless of a decline in income and slower new bookings.

Q3 Monetary Outcomes

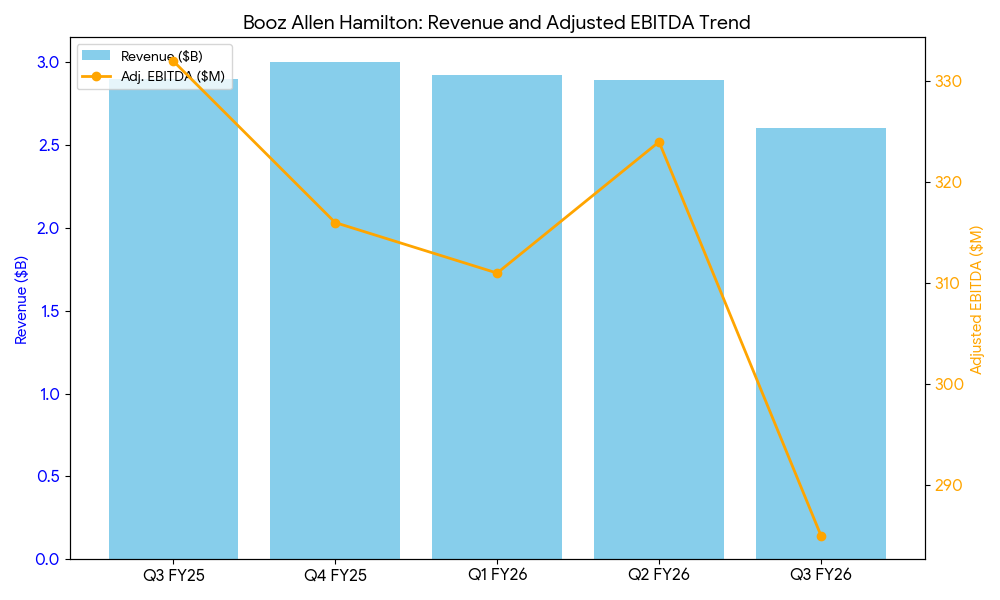

- Income: $2.62 billion, down 10.2% year-over-year, reflecting slower federal procurement, delayed contract execution, and diminished civilian company spending.

- Adjusted EPS: $1.77, above consensus expectations, aided by price self-discipline and favorable tax gadgets.

- Adjusted EBITDA: $285 million, yielding a margin of about 10.9%, broadly steady regardless of income decline.

- Working Earnings: Declined year-over-year, in step with decrease top-line efficiency.

- Internet Earnings: Roughly $200 million for the quarter.

- Free Money Circulate: $248 million, up greater than 80% from prior yr attributable to disciplined working capital administration.

Backlog and Billings

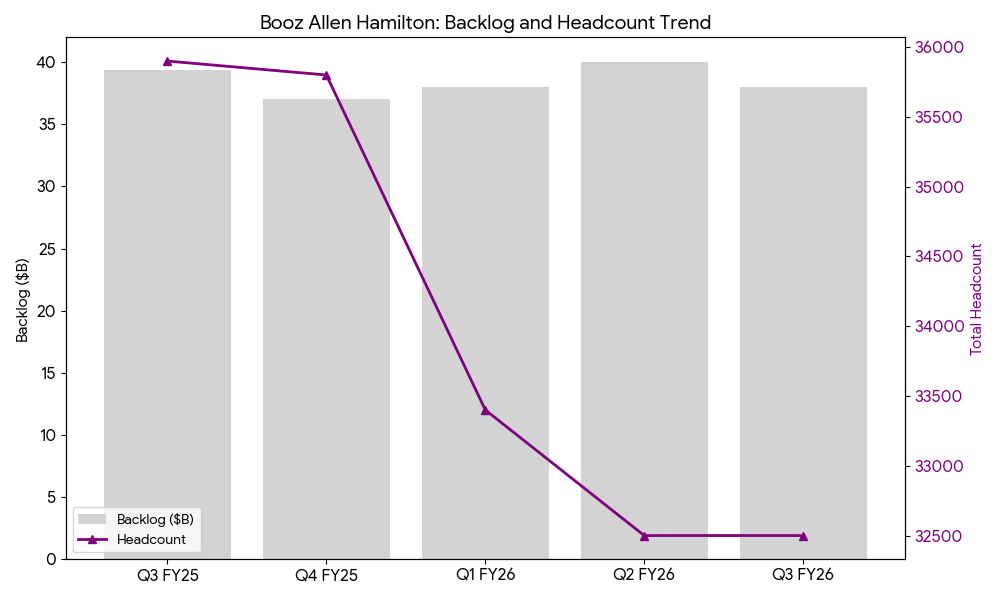

- Whole Backlog: ~$38 billion, largely steady year-over-year, offering multi-year income visibility.

- Ebook-to-Invoice Ratio: ~0.3x, indicating slower new bookings throughout the quarter.

- Headcount: Roughly 31,000 staff, comparatively flat sequentially, reflecting the corporate’s concentrate on effectivity and value administration amid slower new contract awards.

12 months-Over-12 months and Full-12 months Context

Quarterly income declined from Q3 fiscal 2025 ranges of ~$2.92 billion. Backlog remained stable, although slower bookings sign potential top-line stress in upcoming quarters. Headcount stability suggests tight management over labor prices and productiveness throughout a interval of weaker income progress.

Full-12 months Steering:

- Income: $11.3 billion – $11.4 billion, beneath prior expectations.

- Adjusted EPS: $5.95 – $6.15, reflecting anticipated margin resilience and decrease share rely.

Analyst Exercise

No main analyst upgrades or downgrades had been reported with the outcomes. Consensus rankings stay cautious, with income and EPS forecasts trimmed amid ongoing federal procurement uncertainty.

Sector and Macro Pressures

Booz Allen operates in a sector delicate to U.S. federal spending cycles. Delayed funds approvals, slower contract awards, and tighter civilian company budgets have pressured income and billings. Protection and intelligence spending stays comparatively resilient, supporting backlog execution and strategic staffing stability.

Aggressive Panorama

Booz Allen competes with CACI Worldwide, Leidos, and SAIC throughout cybersecurity, mission assist, analytics, and know-how modernization. Rivals face related publicity to federal funding uncertainty, with relative efficiency tied to contract combine, phase publicity, and talent to handle headcount according to backlog traits.

Backside Line

Q3 outcomes confirmed income contraction and weak new bookings, partially offset by sturdy adjusted earnings, steady margins, stable free money stream, and steady headcount. Backlog remained sturdy however slower bookings sign potential top-line challenges forward. Full-year steerage displays moderated progress expectations, and investor focus will stay on backlog execution, contract awards, and value self-discipline amid ongoing federal funds pressures.

Commercial