Bitcoin’s implied volatility has fallen to its lowest stage since 2023.

Based on on-chain analysts in a Wednesday analysis report, the course of Bitcoin’s value will now rely on the long run accumulation of open curiosity.

MVRV Ratio Suggests a ‘Wait-and-See’ Method

Analyst ‘XWIN Research Japan’ identified that Bitcoin’s Market Worth to Realized Worth (MVRV) ratio is at a impartial place of round 2.1. An MVRV of two.1 signifies that buyers are neither seeing main losses nor extreme income.

Sponsored

Sponsored

This value stage is unlikely to set off a wave of panic promoting or pure profit-taking. The analyst defined that in such intervals, a “wait-and-see” perspective tends to dominate the market.

Bitcoin: MVRV Ratio. Supply: CryptoQuant

This quiet sentiment is additional supported by the continued decline within the whole steadiness of Bitcoin held on exchanges, which suggests a weakening of promoting strain. Traditionally, a lower in trade holdings has been a prelude to a provide scarcity when demand instantly surges. XWIN Analysis Japan means that the market could now be experiencing the “calm before the storm.”

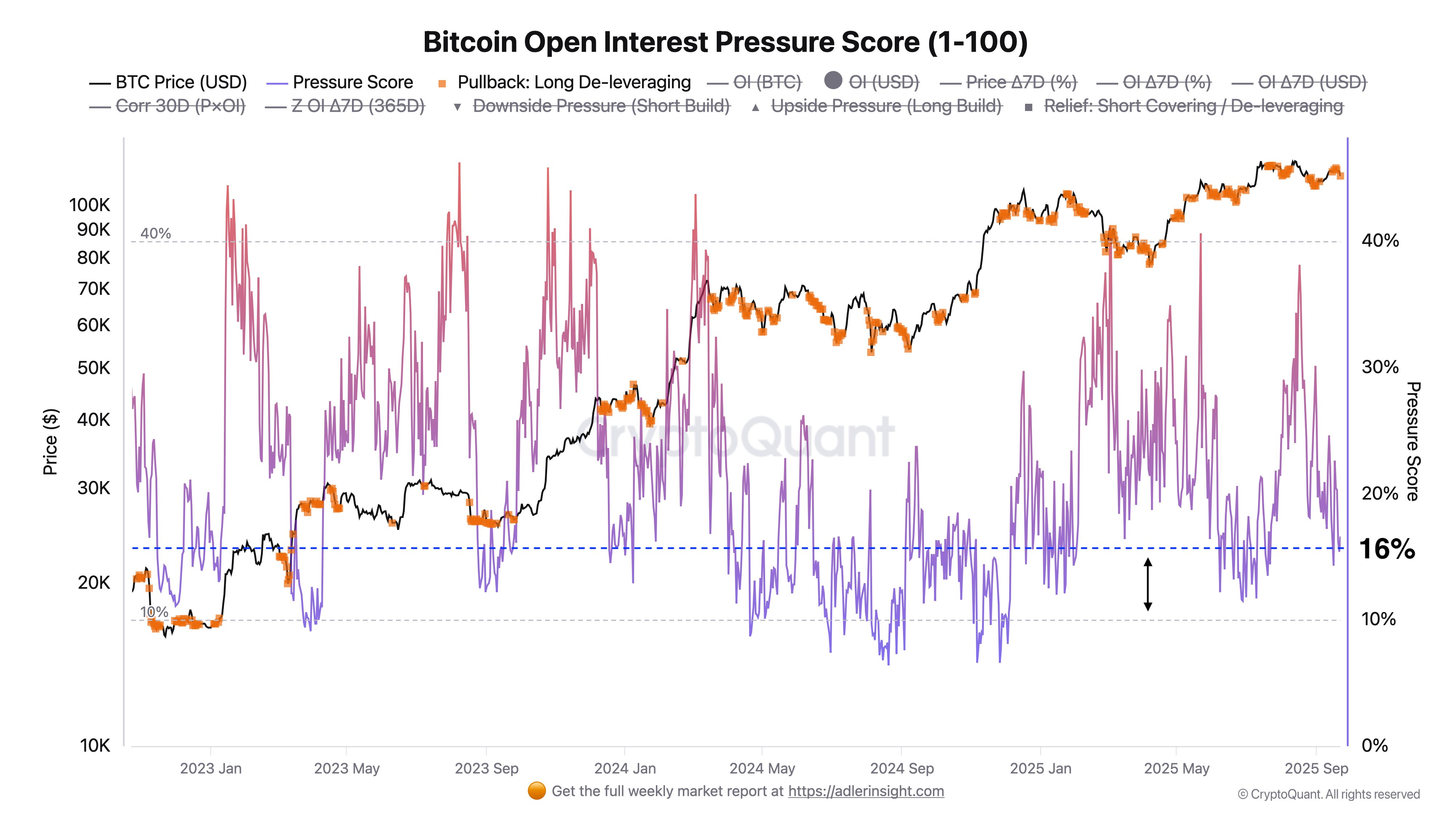

Open Curiosity: The Key to the Subsequent Transfer

One other analyst, ‘Axel Adler Jr’, that the latest sharp value drop induced Bitcoin’s open curiosity to fall by 16%. This means that leverage is now at a low stage following a latest deleveraging of lengthy positions.

Axel Adler Jr argues that the long run value path of Bitcoin is determined by which course open curiosity (OI) begins to build up. If lengthy positions enhance under a resistance stage, the chance of one other leverage-driven drop will increase. Conversely, if brief positions enhance throughout a downturn, the likelihood of an upward transfer by way of a brief squeeze rises.

The analyst believes a transparent directional sign will emerge when the chance of leverage accumulation/strain rises above 40% or when it drops to a ten% leverage depletion stage, signaling a possible reversal.