ARLP|EPS $0.07 vs $0.35 est (-80.0%)|Rev $516.0M|Internet Revenue $9.1M

Inventory $24.90 (-1.3%)

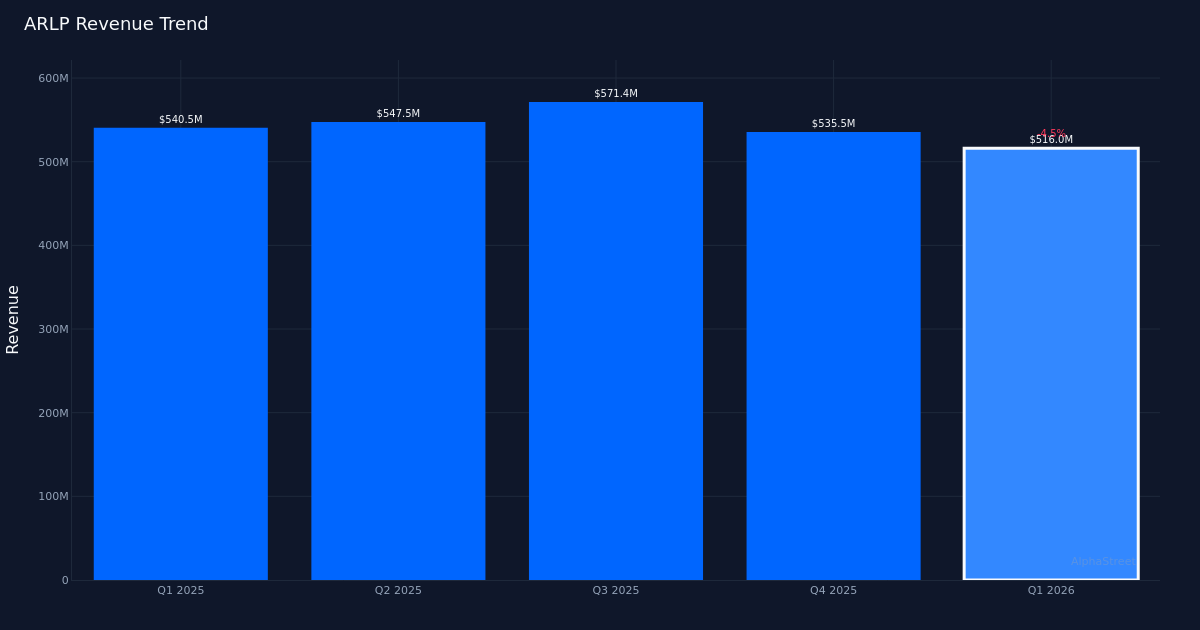

Important Miss. Alliance Useful resource Companions, L.P. (ARLP) reported Q1 2026 primary and diluted earnings of $0.07 per share, badly lacking the $0.35 consensus estimate by 80.0%. The thermal coal producer generated $516.0M in income for the quarter, representing a 4.5% lower from the $540.5M recorded in Q1 2025. Backside-line revenue got here in at $9.1M, a dramatic decline from the $0.57 per share earned a yr in the past—an 87.7% lower that underscores the extreme margin compression dealing with the partnership.

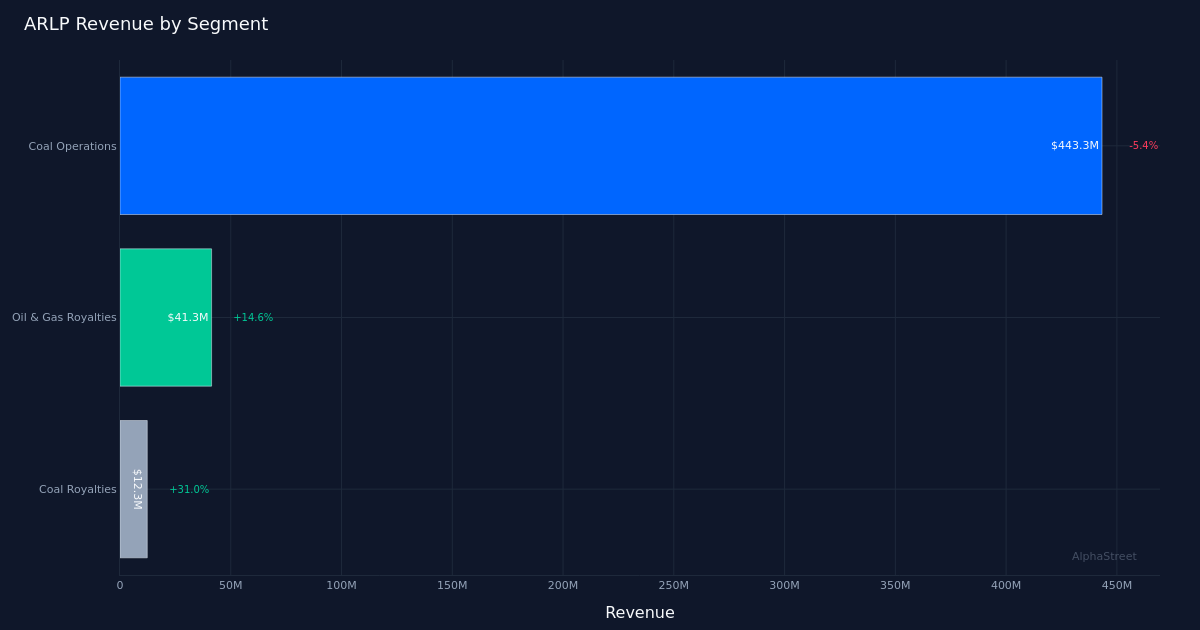

Coal Operations Decline. The corporate’s core Coal Operations section led with $443.3M in income, down 5.4% year-over-year, reflecting continued headwinds in thermal coal markets. With 1,200,000 complete coal stock at quarter finish, Alliance maintains operational scale however faces persistent demand challenges as utilities proceed transitioning away from coal-fired technology. The income decline coupled with the sharp earnings contraction suggests this was not merely a quantity story—margin strain seems acute, seemingly pushed by each pricing weak spot and elevated working prices within the present atmosphere.

Royalty Vibrant Spot. A notable constructive emerged from the corporate’s diversification efforts, with oil & gasoline royalty revenues posting 14.6% development for the quarter. This section continues to supply vital money movement stability because the core coal enterprise navigates structural challenges. The royalty stream’s countercyclical traits supply some buffer towards thermal coal volatility, although the section stays too small to offset the partnership’s major publicity to coal market dynamics.

Market Response Muted. The inventory traded down 1.3% to $24.90 following the discharge, a comparatively contained response given the magnitude of the earnings miss. This means traders might have already anticipated weak outcomes or are specializing in the partnership’s distribution capability moderately than near-term earnings volatility. With Wall Road consensus standing at 6 purchase rankings, 1 maintain, and 0 promote suggestions, the analyst neighborhood seems to take care of conviction regardless of operational headwinds, seemingly viewing present weak spot as cyclical moderately than terminal.

High quality Issues. The severity of the revenue decline relative to the extra modest income lower—87.7% versus 4.5%—raises questions on working leverage and price construction. This earnings high quality concern suggests the partnership is absorbing important margin compression, whether or not from decrease realized costs, larger enter prices, or unfavorable contract combine. Buyers will want visibility into administration’s plans to revive profitability and whether or not the present value construction is sustainable at prevailing coal costs.

What to Watch: Deal with Q2 coal pricing commentary and contract renewal charges, which can decide whether or not margin strain intensifies or stabilizes. The partnership’s skill to take care of its distribution whereas earnings stay underneath strain will check steadiness sheet capability, making leverage metrics and money technology essential monitoring factors for unitholders.

This content material is for informational functions solely and shouldn’t be thought-about funding recommendation. AlphaStreet Intelligence analyzes monetary knowledge utilizing AI to ship quick and correct market info. Human editors confirm content material.