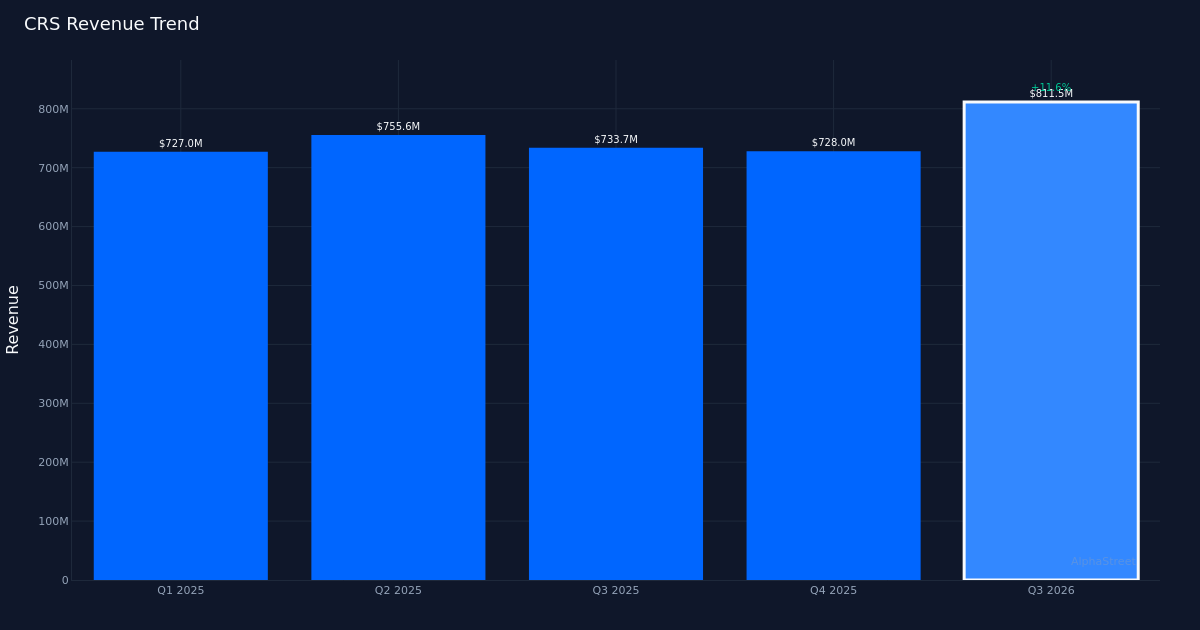

CRS|EPS $2.77 vs $2.64 est (+4.9%)|Rev $811.5M vs $797.5M est (+1.8%)|Internet Revenue $139.6M

Inventory $423.96 (-1.0%)

EPS YoY +47.3%|Rev YoY +12%|Internet Margin 17.2%

Carpenter Know-how (CRS) delivered a decisive beat on each prime and backside strains in Q3 2026, however the power beneath the headline numbers reveals an much more compelling story. The specialty metals producer posted adjusted EPS of $2.77, surpassing estimates by 4.9%, whereas income of $811.5M exceeded consensus by 1.8%. Extra considerably, the corporate achieved a 47.3% year-over-year EPS growth on simply 12% income progress, a margin story that alerts elementary working leverage slightly than mere quantity good points.

The standard of those earnings stands out instantly when inspecting margin development. Internet margin expanded to 17.2% from 16.7% a yr in the past, whereas working margin reached 23.0% within the quarter. This margin growth towards a backdrop of 12.0% income progress demonstrates that Carpenter isn’t merely driving quantity tailwinds—the corporate is extracting considerably extra revenue from every greenback of gross sales. The $139.6M in internet earnings represents a 46% enhance over the year-ago determine of $95.4M, outpacing the 12% income progress charge and confirming that operational effectivity enhancements are driving the earnings acceleration. Administration emphasised this achievement, noting: “The ability to increase earnings by 20% sequentially over what was a record quarter and in a market that is still accelerating must be recognized as superior performance.”

Sequential momentum seems sturdy when considered by means of the four-quarter lens. Income development exhibits Q3 2026 at $811.5M, representing a considerable step-up from This fall 2025’s $728.0M and Q3 2025’s $733.7M, although Q2 2025 registered $755.6M, making a blended sample. The essential commentary lies in internet earnings trajectory: $139.6M in Q3 2026 marks a transparent acceleration from $95.4M a yr prior, $111.7M in Q2 2025, and $117.3M in This fall 2025. This ascending revenue sample regardless of uneven income tendencies reinforces the margin growth narrative—Carpenter has cracked the code on changing gross sales into revenue extra effectively than it did all through 2025.

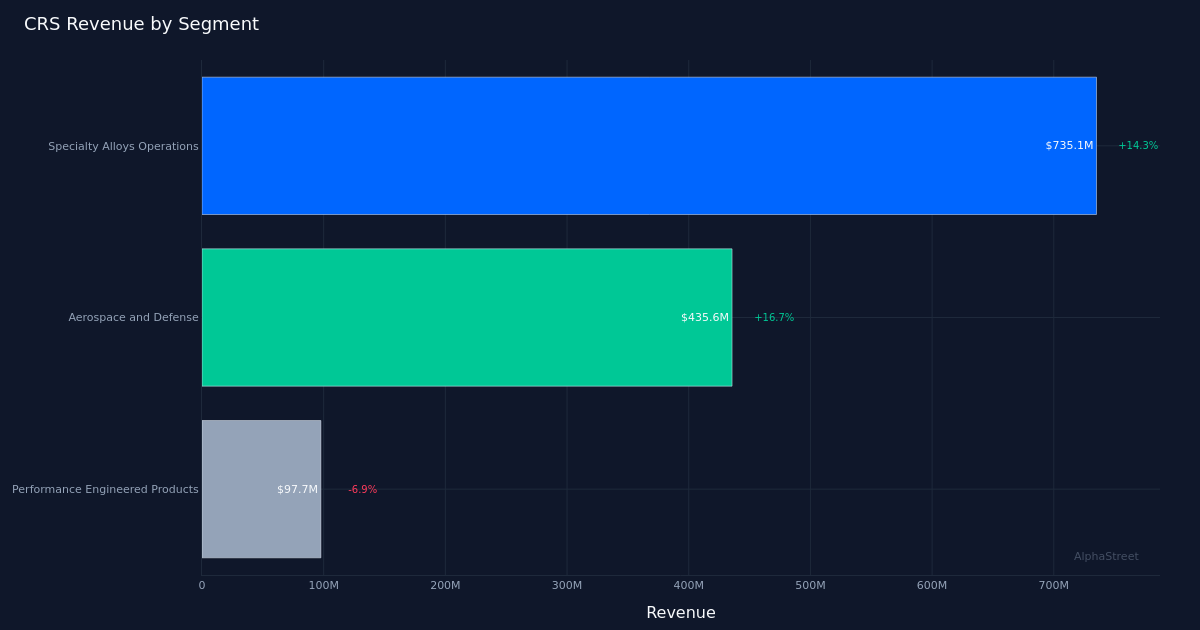

Section efficiency reveals a stark bifurcation that deserves shut consideration. Specialty Alloys Operations generated $735.1M with spectacular 14.3% progress, representing over 90% of complete income and clearly serving as the corporate’s main progress engine. The section’s working margin of 35.6% stands as a outstanding achievement within the capital-intensive metals fabrication trade. Administration highlighted this milestone: “The SAO segment delivered an adjusted operating margin of 35.6% in the quarter, another new record for the business.” In distinction, Efficiency Engineered Merchandise posted $97.7M, with a regarding 6.9% decline. The divergence suggests Carpenter’s fortunes are more and more tied to its specialty alloys enterprise, with the aerospace and protection finish market driving a lot of the power at $435.6M and 16.7% progress. Administration famous continued momentum in key classes: “So still see very strong sales on the, on the engine side fasteners were up 9 or 10% sequentially, about 20% year over year.”

Quantity metrics present extra texture to the expansion story. The corporate bought 53.5 million kilos within the quarter. The mixture of 12.0% income progress and vital margin growth suggests Carpenter is reaching each quantity good points and favorable pricing/combine. The aerospace and protection vertical’s 16.7% progress signifies the corporate is well-positioned in high-value purposes the place technical specs and high quality certifications create switching prices and pricing energy.

The market’s muted response—shares have been largely unchanged following the report—suggests traders could have already priced in a lot of this power. The 100% beat charge during the last quarter signifies consistency, however a single-quarter monitor report offers restricted perception into how usually Carpenter exceeds expectations. The inventory’s stability regardless of report earnings and margin efficiency may mirror both full valuation or skepticism about sustainability, significantly given the Efficiency Engineered Merchandise section’s contraction.

Administration’s tone conveyed confidence within the sturdiness of present tendencies. The emphasis on sequential enchancment over an already-record quarter alerts that management views this efficiency as reflecting structural enhancements slightly than cyclical peaks. The 35.6% working margin in Specialty Alloys Operations represents a stage that may have appeared bold in prior cycles, but administration’s commentary suggests continued room for optimization: “As you’ve seen, we’ve delivered steady increase in SAO margins and we’re very happy with the efforts of the commercial and OPER teams to achieve the 35.6% this quarter.”

What to Watch: The sustainability of 35.6% working margins in Specialty Alloys Operations might be essential—any compression would sign pricing stress or price inflation. Monitor whether or not Efficiency Engineered Merchandise can stabilize or if the 6.9% decline represents the beginning of structural headwinds. Aerospace and protection progress tendencies deserve shut monitoring given this vertical’s 16.7% growth and obvious pricing energy. Free money move conversion relative to internet earnings will point out whether or not working capital is absorbing progress or if the enterprise mannequin generates clear money. Lastly, look ahead to any shifts in kilos bought sequentially, as quantity tendencies will reveal whether or not demand power persists past favorable pricing and blend results.

This content material is for informational functions solely and shouldn’t be thought of funding recommendation. AlphaStreet Intelligence analyzes monetary knowledge utilizing AI to ship quick and correct market info. Human editors confirm content material.

s, IRAs")