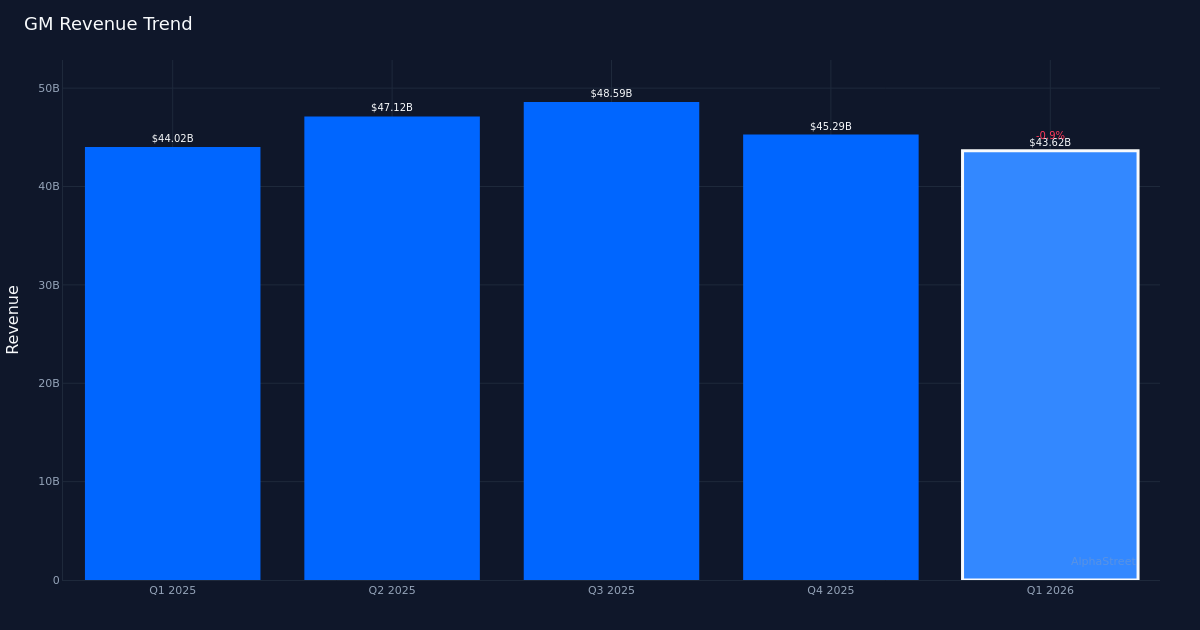

GM|EPS $3.70 vs $2.69 est (+37.5%)|Rev $43.62B|Web Revenue $2.63B

Steering GAAP $10.62 – $12.62|Inventory $75.00 (-3.8%)

Spectacular Beat. Common Motors Firm (NYSE:GM) delivered a powerful begin to 2026, posting adjusted earnings of $3.70 per share that crushed Wall Avenue expectations of $2.69—a 37.5% beat that underscores the automaker’s operational resilience. Income totaled $43.62B for the quarter, down a modest 0.9% from $44.02B within the year-ago interval, whereas adjusted bottom-line revenue got here in at $3.43B.

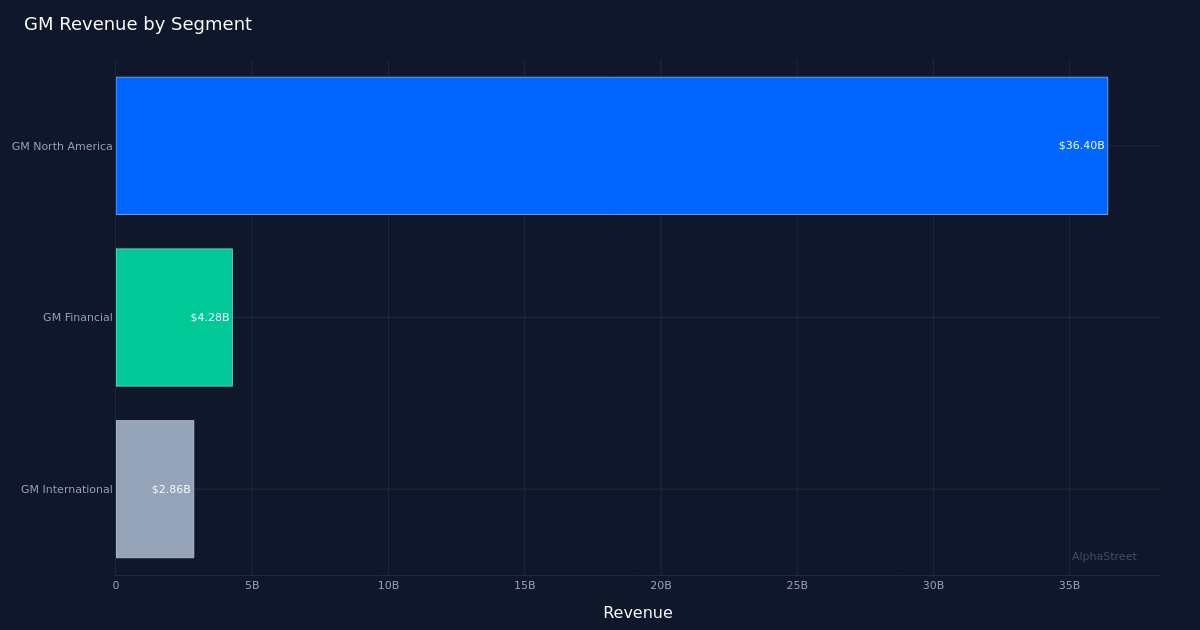

High quality of Efficiency. The magnitude of the earnings beat factors to a mix of favorable components past easy top-line progress. With income primarily flat year-over-year regardless of wholesale car gross sales of 20,786,000 for the quarter, the substantial revenue outperformance suggests improved pricing self-discipline, favorable product combine, or margin enlargement throughout the corporate’s operations. GM North America, the corporate’s largest section, generated $36.40B in income for the quarter, representing the lion’s share of whole gross sales and highlighting the home market’s continued significance to the corporate’s monetary profile.

Ahead Steering. Administration supplied a variety for full-year 2026 GAAP EPS, projecting $10.62 to $12.62, reflecting the continuing uncertainty within the automotive sector round shopper demand, rates of interest, and the tempo of the electrical car transition. For FY2026, the corporate expects income between $9.90B and $11.40B—a notably broad vary which will elevate questions amongst analysts about near-term visibility.

Market Sentiment. Wall Avenue maintains a usually constructive view on GM shares, with analyst consensus standing at 18 purchase rankings, 8 maintain rankings, and simply 2 promote suggestions. This tilts positively, although the inventory’s muted response to a considerable earnings beat suggests the market could also be grappling with competing narratives—celebrating robust present profitability whereas weighing considerations concerning the income trajectory and the corporate’s positioning in an evolving automotive panorama marked by electrification pressures and intensifying competitors.

What to Watch: GM’s capacity to maintain margin enlargement whereas navigating the pricey EV transition will decide whether or not the corporate can keep its earnings momentum by means of the rest of 2026.

This content material is for informational functions solely and shouldn’t be thought-about funding recommendation. AlphaStreet Intelligence analyzes monetary information utilizing AI to ship quick and correct market data. Human editors confirm content material.

This autumn Earnings: Misses on EPS, Income Recap – Alphastreet")