![]() FLG|EPS $0.04 vs $0.03 est (+33.3%)|Rev $498.0M|Web Revenue $21.0M

FLG|EPS $0.04 vs $0.03 est (+33.3%)|Rev $498.0M|Web Revenue $21.0M

Inventory $14.35 (+0.8%)

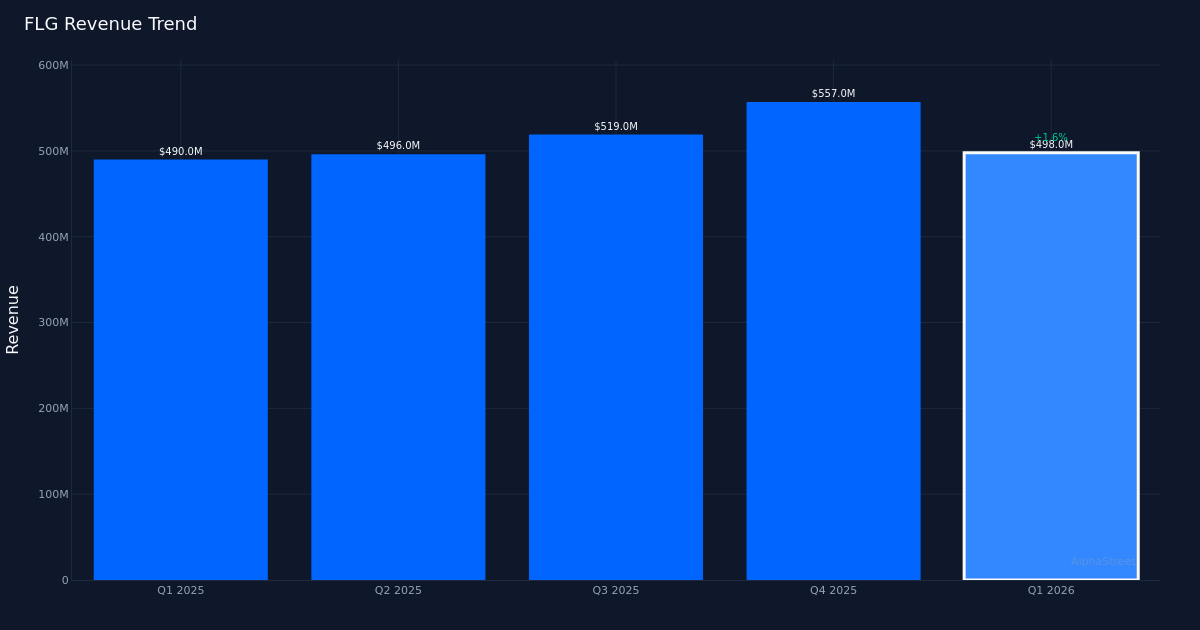

Modest Beat Delivered. Flagstar Financial institution, Nationwide Affiliation (NYSE:FLG) reported Q1 2026 adjusted earnings of $0.04 per share, edging previous the Avenue’s $0.03 consensus estimate by 33.3%. Income totaled $498.0M for the quarter, representing a 2.0% enhance from the $490.0M recorded in Q1 2025. The regional financial institution’s inventory traded largely unchanged following the discharge, suggesting traders are viewing the outcomes as incrementally constructive however not materially game-changing for the franchise.

Profitability Stays Skinny. Backside-line revenue got here in at $20.0M for the quarter, translating to razor-thin margins in an working setting that continues to problem regional banks. The modest earnings beat seems pushed primarily by the top-line enchancment fairly than aggressive expense administration, which is usually considered extra favorably by the market because it suggests sustainable income momentum. The two.0% year-over-year income progress, whereas constructive, displays the headwinds going through the banking sector as web curiosity margins stay compressed and mortgage demand stays muted throughout many markets.

Steadiness Sheet Scale. Flagstar maintained whole property of $87.10B at quarter finish, offering the regional financial institution with significant scale to compete towards each bigger money-center establishments and smaller neighborhood banks. The corporate’s bodily footprint encompasses 340 whole places, positioning it as a big regional participant with the distribution community essential to serve each retail and business banking clients. This department community stays a aggressive benefit in markets the place in-person banking relationships proceed to drive deposit gathering and mortgage origination, significantly for small and mid-sized companies.

Blended Avenue Sentiment. Wall Avenue analyst sentiment displays cautious optimism, with consensus standing at 8 purchase rankings and 11 maintain rankings, whereas no analysts at the moment price the shares a promote. This distribution suggests the funding neighborhood sees restricted draw back threat however stays unconvinced that Flagstar has recognized a transparent path to materially speed up progress or broaden profitability within the present price setting. The dearth of a decisive inventory response following the earnings launch reinforces this measured stance, as traders await proof of bettering mortgage progress, deposit stability, or margin growth earlier than committing contemporary capital.

What to Watch: Administration’s skill to translate modest income progress into significant margin growth might be crucial because the yr progresses. The important thing query is whether or not Flagstar can leverage its $87.10B asset base and 340-location community to seize market share in business lending and wealth administration whereas defending its deposit franchise towards aggressive competitors from each conventional banks and digital-only opponents.

This text was generated with the help of AI expertise and reviewed for accuracy. AlphaStreet could obtain compensation from firms talked about on this article. This content material is for informational functions solely and shouldn’t be thought-about funding recommendation.

in 2026")