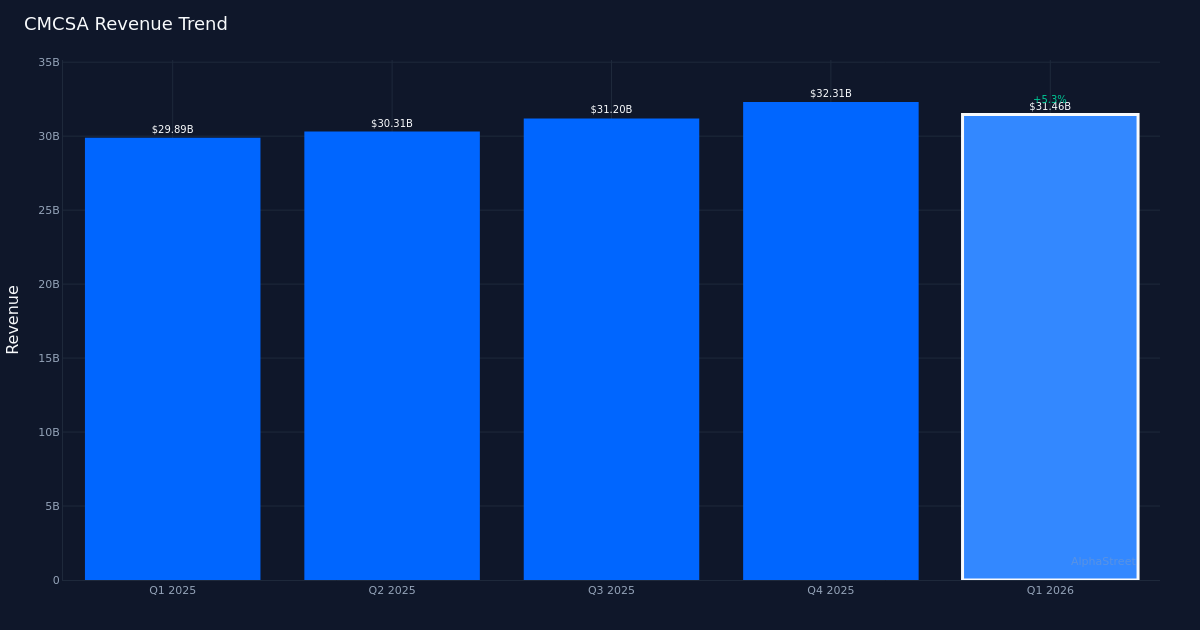

CMCSA|EPS $0.79 vs $0.76 est (+3.9%)|Rev $31.46B|Web Earnings $2.17B

Inventory $31.88 (+8.5%)

Stable beat. Comcast Company (NASDAQ:CMCSA) delivered Q1 2026 adjusted EPS of $0.79, topping Wall Road’s $0.76 estimate by 3.9%, because the telecom and media big demonstrated continued momentum in its wi-fi enterprise whereas navigating headwinds in its legacy connectivity operations. Income totaled $31.46B for the quarter, up 5.3% from $29.89B in Q1 2025, reflecting the corporate’s potential to extract development from shifting client preferences regardless of stress on conventional broadband and video companies. The corporate earned $2.86B in adjusted internet earnings for the interval, underscoring the profitability of its diversified service portfolio.

Income-driven efficiency. The standard of this earnings beat seems real, anchored by topline enlargement relatively than aggressive cost-cutting. The 5.3% year-over-year income development suggests Comcast is efficiently offsetting declines in mature enterprise strains with enlargement in higher-growth areas, notably wi-fi companies. This revenue-driven beat carries extra weight for long-term buyers than margin engineering alone, indicating the corporate retains pricing energy and market share in key segments whilst aggressive depth stays elevated throughout telecom companies.

Wi-fi momentum accelerates. Home wi-fi operations proceed to function a vibrant spot, with the corporate including 435,000 internet new strains through the quarter and reaching 9.7M complete home wi-fi strains at quarter finish. This wi-fi enlargement represents a strategic pivot for Comcast, leveraging its current buyer relationships and infrastructure investments to seize share within the cellular market. The wi-fi enterprise gives a development vector that partially offsets structural challenges in conventional cable, although the capital depth of community investments and aggressive promotional exercise from incumbent carriers warrant continued monitoring.

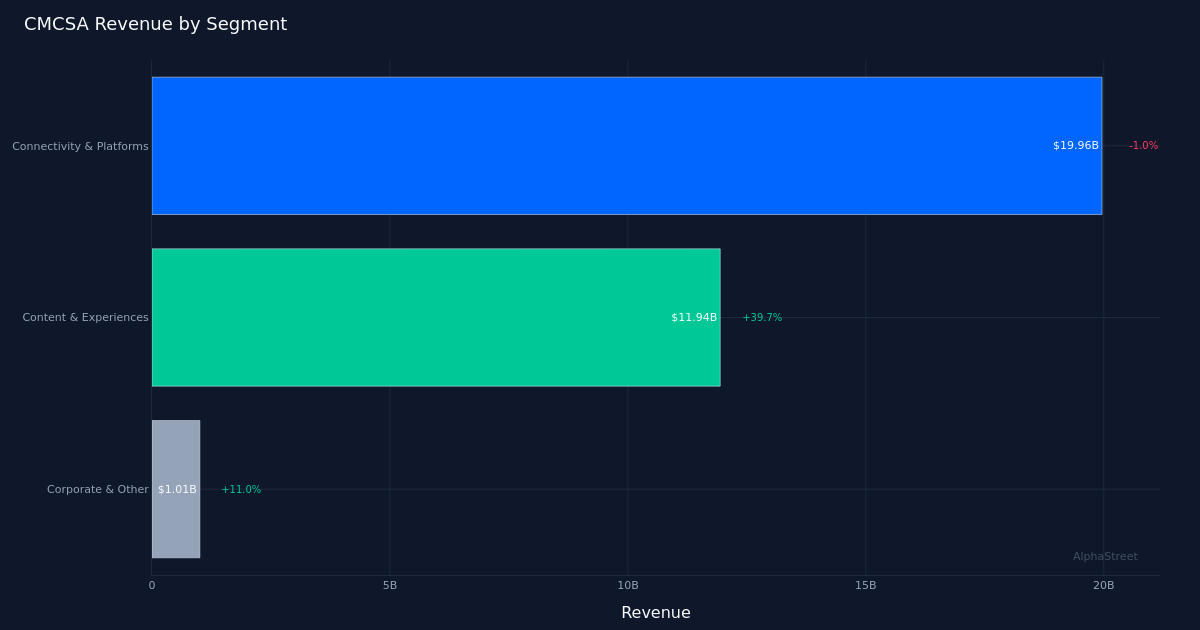

Core connectivity pressures persist. The Connectivity & Platforms phase led income era with $19.96B however noticed a 1.0% year-over-year decline, highlighting ongoing pressures within the firm’s foundational broadband and video companies. Wire-cutting tendencies and glued wi-fi competitors from telecom rivals proceed to weigh on this phase, whilst the corporate makes an attempt to bundle companies and drive ARPU enhancements. The modest decline suggests stabilization relatively than accelerating deterioration, however the phase’s trajectory stays a key concern for buyers evaluating the corporate’s long-term worth proposition.

Market response. Shares jumped 8.5% after the discharge, reflecting optimism that administration can maintain worthwhile development amid business headwinds. Wall Road consensus stands at 10 purchase, 21 maintain, and three promote rankings, indicating a divided view on the corporate’s prospects because it transitions from legacy cable dominance to a extra diversified connectivity and content material mannequin.

What to Watch: Monitor whether or not wi-fi line additions can maintain present momentum and whether or not the corporate can stabilize or reverse the Connectivity & Platforms income decline by way of profitable fiber enlargement and improved broadband buyer retention.

This text was generated with the help of AI expertise and reviewed for accuracy. AlphaStreet could obtain compensation from corporations talked about on this article. This content material is for informational functions solely and shouldn’t be thought-about funding recommendation.