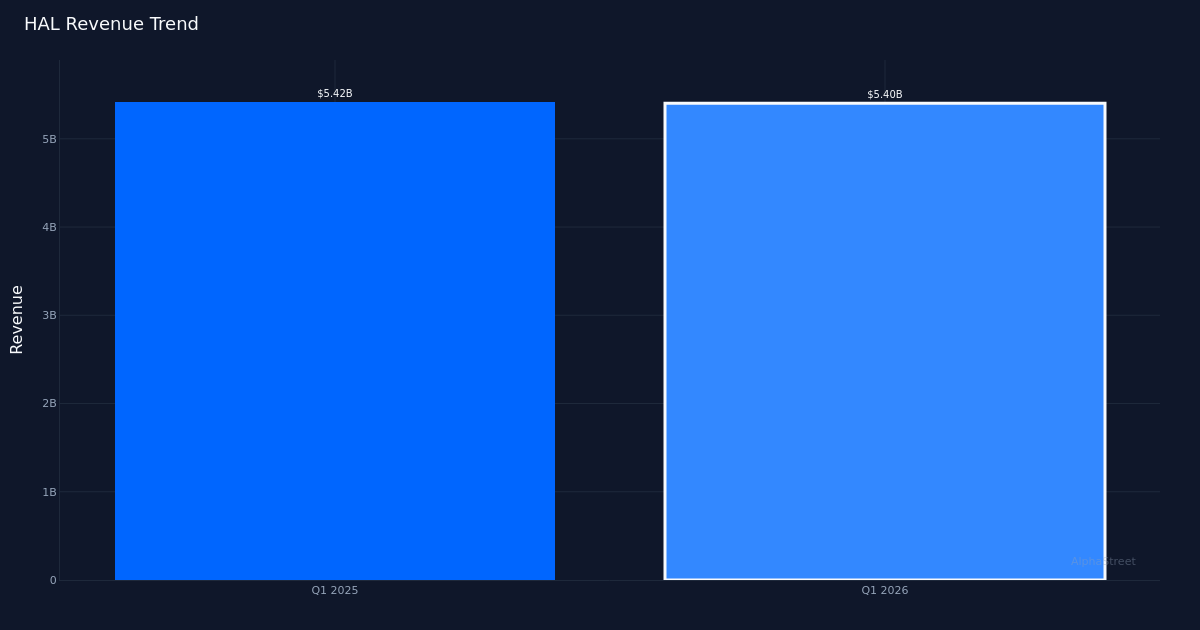

HAL|EPS $0.55 vs $0.50 est|Rev $5.40B|Web Earnings $461.0M

Inventory $36.68 (-1.3%)

EPS YoY +129.2%|Rev YoY -0.3%|Web Margin 8.5%

High quality beats amount in Halliburton’s margin growth story. Oilfield companies big Halliburton Firm (NYSE: HAL) delivered adjusted EPS of $0.55 for Q1 2026, beating the Avenue’s $0.50 estimate by 10.0% regardless of primarily flat income of $5.40B. The headline quantity masks the true story: a dramatic transformation in profitability. Web margin expanded 4.8 share factors year-over-year to eight.5%, whereas internet revenue greater than doubled to $461.0M from $204.0M within the prior-year quarter. This wasn’t revenue-driven progress—this was operational leverage lastly displaying up within the backside line. The inventory’s 1.3% decline to $36.68 suggests traders are specializing in the flat prime line slightly than the standard of earnings, a doubtlessly short-sighted response.

Margin growth tells the earnings high quality story. With income declining 0.4% year-over-year from $5.42B to $5.40B, the 129.2% surge in EPS from $0.24 to $0.55 got here fully from margin enchancment, not income progress. Working margin reached 12.6%, producing $679.0M in working revenue on that $5.40B income base. The corporate’s means to extract this stage of profitability from a stagnant income base demonstrates pricing energy and value self-discipline in a difficult macro setting. The online margin growth from 3.8% to eight.5% year-over-year represents structural enchancment, not one-time advantages, positioning the corporate for sustained profitability even when income progress stays muted.

Geographic divergence reveals the true problem. The worldwide versus North America break up exposes the underlying income stress. Worldwide income of $3.3B grew 3% year-over-year, offering some offset to North America’s 4% decline to $2.1B. This geographic combine shift issues past the top-line influence—worldwide work sometimes carries completely different margin profiles and contract constructions. The North America weak spot aligns with well-documented softness in U.S. land drilling exercise, whereas the worldwide progress displays longer-cycle initiatives with extra secure demand traits. The corporate’s means to take care of total margins regardless of this geographic shift suggests pricing self-discipline throughout each theaters.

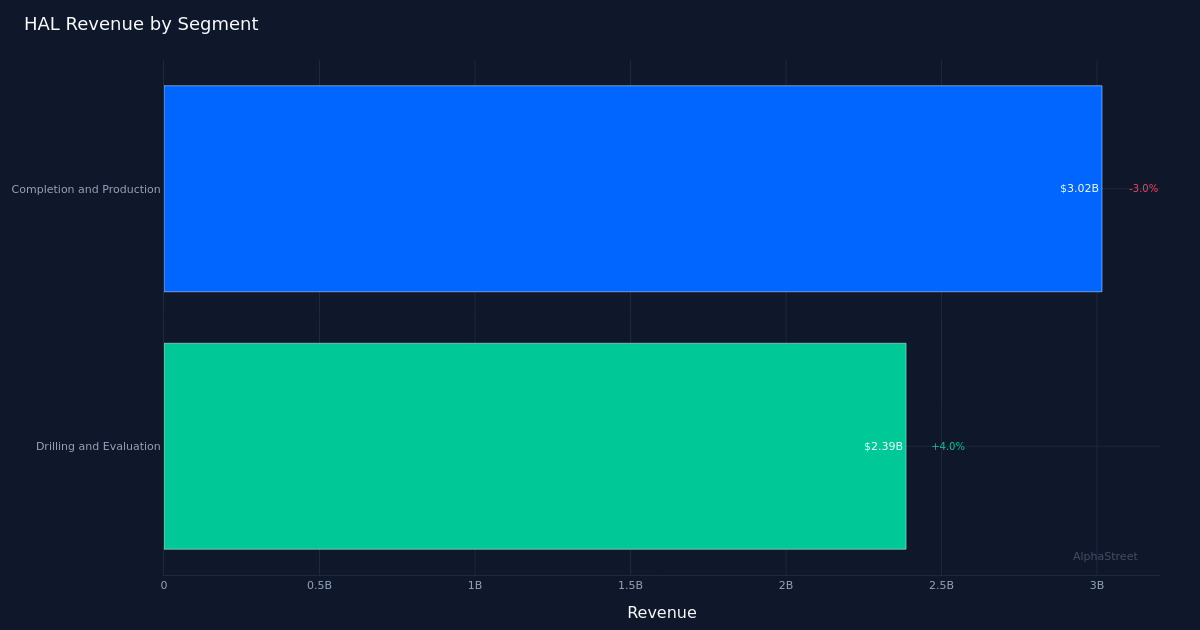

Section efficiency reveals combined underlying demand. The Drilling and Analysis phase posted $2.39B in income with 4.0% progress, whereas Completion and Manufacturing generated $3.02B with a 3.0% decline. This divergence issues for ahead visibility. Drilling and Analysis tends to be an earlier-cycle indicator, suggesting clients are nonetheless investing in exploration and appraisal work whilst they pull again on completion exercise. The Completion and Manufacturing phase’s decline probably displays the North America headwinds, the place completion crews face pricing stress and decrease utilization. The truth that the smaller, faster-growing phase couldn’t offset the bigger phase’s decline explains the flat consolidated income. Traders ought to watch whether or not Drilling and Analysis’s progress accelerates, which might sign a possible inflection within the broader exercise cycle.

Capital allocation indicators conservative administration expectations. Working money circulate of $273.0M transformed to simply $123.0M in free money circulate, indicating continued capital depth within the enterprise. Extra telling is administration’s commentary on share repurchases: “The buyback at $100 million was I think a little bit lighter than the run rate we’ve seen at $250 million a quarter.” This deceleration in buyback exercise from a $250M quarterly run fee to $100M suggests administration sees higher makes use of for money, presumably preserving flexibility for potential M&A or anticipating near-term market volatility. The diminished buyback tempo, mixed with the inventory’s decline regardless of the earnings beat, creates a disconnect price monitoring—both administration is being overly cautious or they see headwinds the Avenue hasn’t absolutely priced in.

Steering implications from geopolitical battle. Whereas particular ahead steerage numbers weren’t offered within the verified information, administration commentary revealed they’ve embedded conflict-related impacts of their outlook. One analyst famous, “I appreciate the guidance on 2Q in terms of the EPS impact of the conflict and how it’s embedded in your guidance.” This implies near-term headwinds are already baked into expectations, which might clarify the muted inventory response. The truth that administration is looking out particular geopolitical impacts implies materials publicity to conflict-affected areas, probably within the Center East or Jap Europe, the place worldwide operations would face disruption threat.

What to Watch: The trajectory of North America income will sign whether or not the 4% year-over-year decline stabilizes or accelerates. Monitor the Drilling and Analysis phase’s progress fee—sustained growth above 4% would point out early-cycle power that ought to finally circulate by means of to Completion and Manufacturing. The buyback run fee deserves scrutiny; if administration maintains the diminished $100M quarterly tempo, it indicators both steadiness sheet warning or various capital deployment plans. Worldwide margin developments will reveal whether or not the three% income progress there comes with acceptable returns or displays aggressive pricing stress. Lastly, observe working money circulate conversion—the hole between $273.0M in working money circulate and $123.0M in free money circulate signifies capital depth that might compress returns if income progress doesn’t speed up.

This text was generated with the help of AI expertise and reviewed for accuracy. AlphaStreet could obtain compensation from firms talked about on this article. This content material is for informational functions solely and shouldn’t be thought of funding recommendation.

Q3 2025 Earnings: Key financials and quarterly highlights | AlphaStreet")