CLF|Loss Per Share -$0.40|Rev $4.92B|Web Loss $229.0M

Inventory $9.94 (+2.3%)

Rev YoY +6.3%|Web Margin -4.7%

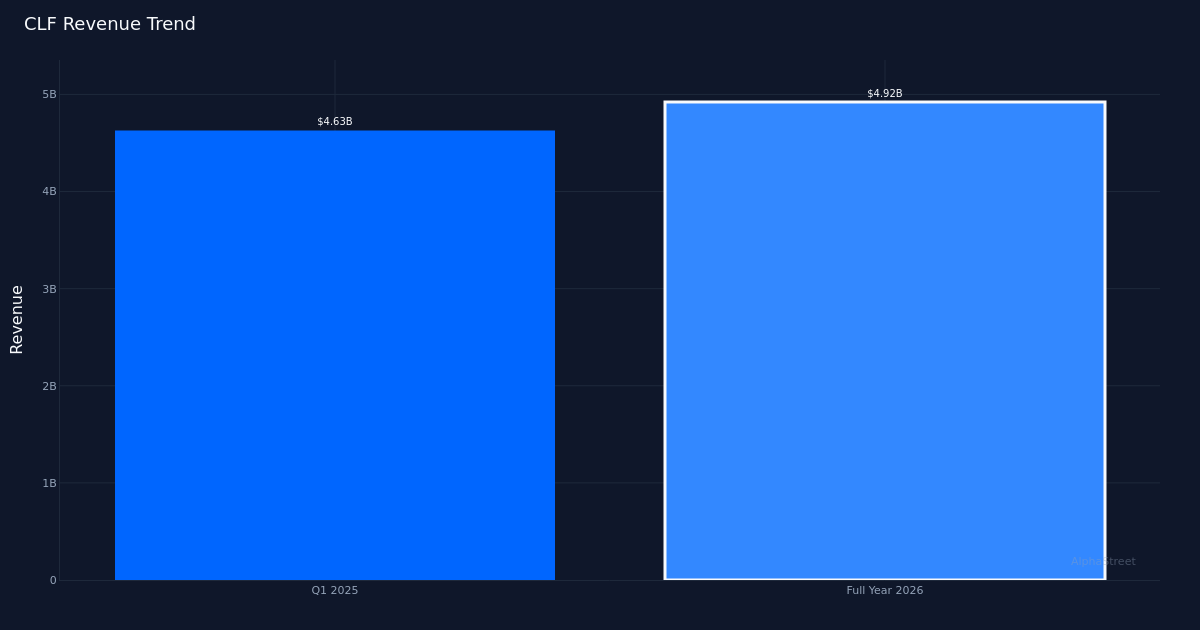

Cleveland-Cliffs Inc. (NYSE: CLF) delivered a materially narrower loss in Q1 2026, posting an adjusted loss per share of $0.40, versus a lack of $1.01 within the year-ago quarter, reflecting pricing momentum and quantity restoration. The metal producer generated income of $4.92B, up 6.3% year-over-year, whereas internet loss narrowed to $229.0M from $486.0M a 12 months earlier. The sequential and year-over-year trajectory reveals a cyclical backside forming, with pricing energy returning to the metal market after an prolonged downturn. EBITDA of $95.0M represented a stark reversal from deeply unfavorable territory, although absolutely the stage stays modest relative to the corporate’s income base.

The standard of this quarter’s enchancment hinges on pricing enlargement somewhat than operational effectivity good points. Web margin improved by 5.8 proportion factors year-over-year to unfavorable 4.7% from unfavorable 10.5%, reflecting the narrowing loss construction. Nevertheless, the corporate stays in unfavorable margin territory regardless of income progress, signaling that price construction nonetheless exceeds pricing realization on a fully-loaded foundation. Administration highlighted that “average selling prices increased by $68 per ton from a year ago and sequentially by $55 per ton during the quarter, reflecting improving market conditions and better automotive pull.” This pricing momentum drove the EBITDA enchancment. The margin trajectory suggests the corporate is climbing out of a trough, however profitability stays contingent on sustained pricing self-discipline somewhat than structural price benefits.

Income trajectory evaluation reveals stabilization after what seems to have been a multi-quarter downturn. The four-quarter pattern reveals income of $4.63B in Q1 2025, adopted by the present quarter’s $4.92B. The 6.3% year-over-year progress price marks a return to constructive territory. Quantity restoration performed a key function, with administration noting that “first quarter shipments totaled just over 4.1 million tons, which represents a recovery of 338,000 tons sequentially.” Metal shipments of 4.1 million internet tons point out the corporate is working at substantial scale, and the sequential quantity enchancment represents significant throughput restoration.

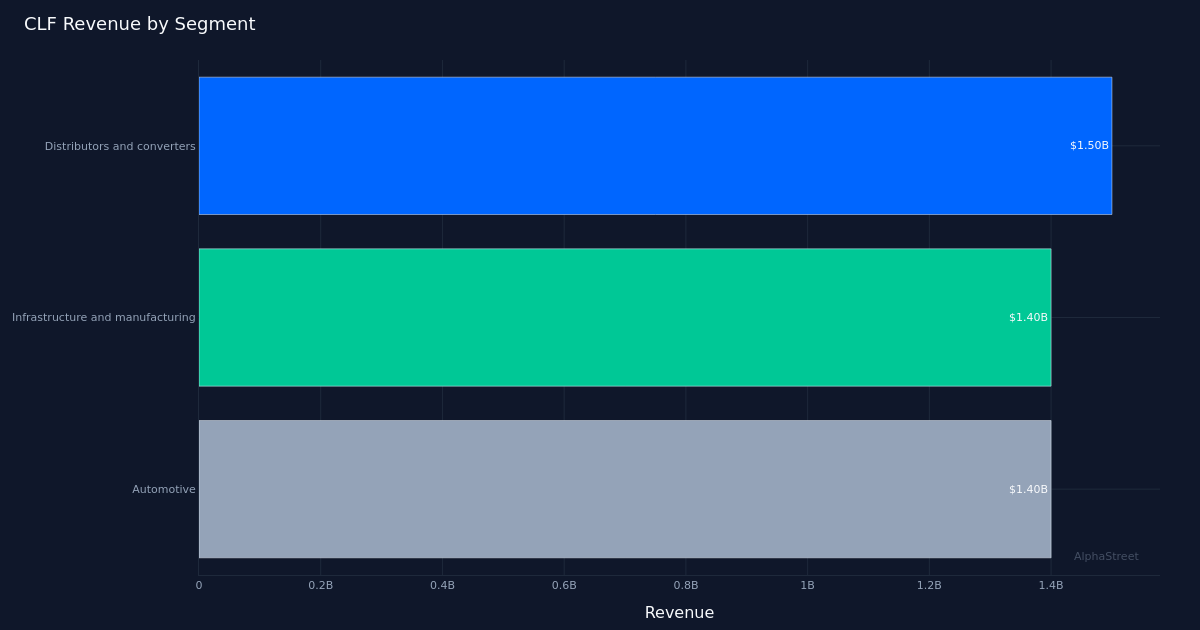

Section composition reveals balanced demand throughout Cleveland-Cliffs’ three main finish markets, although no single section is demonstrating breakout power. The distributors and converters section generated $1.50B, representing the biggest income contributor, whereas infrastructure and manufacturing contributed $1.40B, and automotive additionally delivered $1.40B. The near-parity between infrastructure/manufacturing and automotive segments—each at precisely $1.40B—suggests broad-based demand somewhat than focus danger in any single vertical. The automotive section’s efficiency is especially notable given the cyclical headwinds going through that business, with administration attributing pricing good points partially to “better automotive pull.” The distributor section’s main place displays the significance of service middle stock restocking within the present section of the metal cycle.

Working capital dynamics level to a enterprise inflecting towards progress somewhat than managing decline. Administration disclosed that “the Q1 build of working capital, about $130 million, was primarily driven by AR as pricing continued to rise in March, shipments were strong, and it was offset by a reduction in inventory.” This accounts receivable construct usually indicators accelerating gross sales exercise and rising costs—prospects are shopping for extra at larger costs, creating timing lags in money assortment. The simultaneous stock discount suggests the corporate is efficiently changing uncooked materials and work-in-process into completed items and shipments, a constructive operational indicator. This working capital sample contrasts sharply with distressed eventualities the place stock builds whereas receivables stagnate.

Administration’s ahead commentary suggests substantial EBITDA leverage to additional pricing enchancment. The corporate’s govt group famous that “last quarter we were talking about, I think about a $500 million increase in EBITDA.” Whereas the present quarter delivered EBITDA of $95.0M, this commentary implies that metal pricing at particular ranges might drive EBITDA to roughly $595 million in a extra normalized atmosphere. This leverage profile displays the excessive fixed-cost nature of built-in metal manufacturing, the place incremental pricing flows on to EBITDA as soon as variable prices are lined. The $68 per ton year-over-year pricing acquire has already pushed a $274 million EBITDA enchancment, establishing a transparent sensitivity ratio that buyers can mannequin for future quarters.

The inventory’s modest 2.3% acquire to $9.94 suggests the market is treating this as affirmation of a gradual restoration somewhat than an inflection level. The muted response doubtless displays continued skepticism in regards to the sustainability of metal pricing enhancements and the corporate’s capacity to return to constant profitability. On the present worth stage, the market seems to be pricing in modest enchancment from trough situations however not rewarding the corporate for the sequential momentum evident in volumes and pricing. The loss per share of $0.40, whereas improved from $0.93 a 12 months in the past, retains the corporate firmly in unfavorable earnings territory, limiting upside catalysts till profitability is restored on a GAAP foundation.

What to Watch: The sustainability of pricing good points will decide whether or not Cleveland-Cliffs can attain administration’s implied EBITDA targets. Monitor automotive sector demand indicators, as this section now represents a 3rd of income, and administration cited “better automotive pull” as a pricing driver. Sequential quantity traits past the Q1 restoration will sign whether or not capability utilization is bettering structurally. Working capital traits will present early warning of pricing momentum or deterioration. The trail from $95.0M quarterly EBITDA to the implied $500+ million enchancment potential relies upon completely on metal worth realization—benchmark hot-rolled coil costs stay the one most necessary exterior metric for modeling Cleveland-Cliffs’ earnings trajectory.

This text was generated with the help of AI know-how and reviewed for accuracy. AlphaStreet might obtain compensation from corporations talked about on this article. This content material is for informational functions solely and shouldn’t be thought of funding recommendation.