Picture supply: Getty Pictures

Lloyds (LSE:LLOY) shares are surging greater than 8% on Wednesday 8 April.

The index is up too, however this nonetheless makes it one of many FTSE 100‘s biggest gainers. Unsurprisingly, it’s the ceasefire settlement between Iran and the US that’s doing the heavy lifting.

Let’s take a more in-depth look and discover whether or not the inventory is price contemplating.

Struggle isn’t good for banks

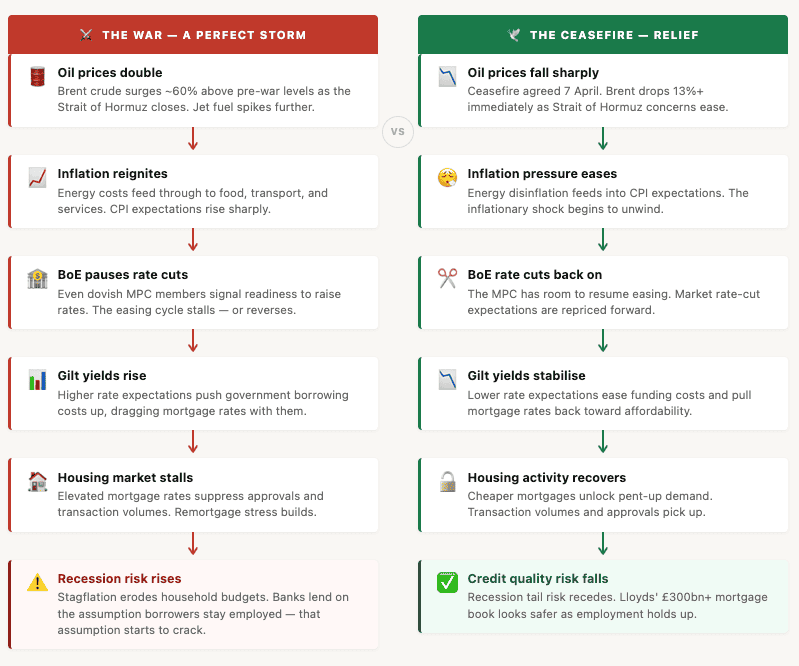

Lloyds is the UK’s largest mortgage lender — it’s actually not diversified. That makes it some of the economically delicate shares on the index, and the Iran-US battle constructed nearly the worst attainable backdrop for a UK retail financial institution.

How does this work? Effectively, the mechanism is sort of a chain response.

Struggle within the Gulf triggered oil costs to double — jet gasoline went even greater. The spike reignited inflation issues. In flip, even probably the most dovish members of the Financial institution of England’s Financial Coverage Fee have been speaking about being prepared to boost rates of interest.

We’ve seen gilt yields rise, mortgage charges keep elevated, and transaction volumes stall. In the long term, maintain excessive vitality costs raised the spectre of recession

Nevertheless, extra worryingly, sustained excessive vitality costs raised the spectre of recession. And recession is the one factor a financial institution concentrated in UK residential mortgages can’t afford.

There are a number of causes for this. However largely it’s as a result of banks lend on the belief that debtors will stay employed. A interval of energy-driven stagflation quietly erodes that assumption throughout a whole mortgage e-book.

The ceasefire adjustments the calculus — extra so if it holds.

Created with Claude

Created with Claude

It’s not low-cost anymore

Adjusting for immediately’s 8% achieve, Lloyds now trades on a ahead price-to-earnings ratio of round 10 occasions, a price-to-book of roughly 1.28 occasions, and a ahead dividend yield of roughly 4.3%.

Institutional analysts are nonetheless pointing to a modest undervaluation, and I feel ‘modest’ is the operative phrase right here. It’s buying and selling above e-book worth and, for a purely UK-focused, cyclical retail financial institution with no funding banking ops, it’s honest, reasonably than a cut price worth.

AI is a danger

The market has been distracted by the struggle within the Gulf. However earlier than that, again in February, buyers have been getting fearful about AI.

AI is nice for productiveness, however it could be so nice that it results in a sustained wave {of professional} job losses that flows straight into mortgage arrears. Lloyds’ £300bn-plus house mortgage e-book has extra publicity to that situation than nearly every other UK-listed firm.

The underside line

Lloyds shares will not be costly, and the ceasefire — if made everlasting — removes a real danger. Nevertheless, with the inventory now nudging the upper finish of what you’d comfortably pay for a cyclical financial institution, there could also be higher worth elsewhere.

It’s nonetheless price contemplating for the long term, however this margin of security concern ought to be entrance of thoughts.