Picture supply: Getty Photographs

Proper now, there’s an S&P 500 inventory that analysts suppose can climb 85% from its present degree. And the underlying enterprise seems to be terrific.

It’s just about a monopoly and is likely to be tougher to disrupt than buyers suppose. However there’s an enormous motive I’m not shopping for it proper now.

The enterprise

The inventory’s Truthful Isaac Company (NYSE:FICO). It’s the corporate behind what folks in US TV exhibits check with as their FICO rating.

FICO scores are primarily a means of evaluating creditworthiness. Lenders use them to work out what loans to make.

These are fairly ubiquitous. When a credit score bureau like Experian checks on somebody, it runs its personal knowledge via FICO’s algorithm. Importantly, the corporate doesn’t personal buyer knowledge. Its algorithm calculates a rating primarily based on the inputs from the credit score bureau.

Traditionally, FICO’s made cash by licensing its product to the most important credit score bureaus. This has been a pleasant enterprise for shareholders.

The inventory nevertheless, has fallen round 58% from its highs. And every time this occurs, buyers must suppose why?

So why’s the inventory down?

FICO’s beneath assault from all sides. One problem is that it’s the topic of a possible antitrust investigation. The difficulty is that the corporate unfairly makes use of its energy to extend costs for credit score scores. And that makes for an advanced state of affairs.

One other concern – bizarrely – is that its place is beneath risk. Experian, Equifax, and TransUnion are launching their very own merchandise.

FICO hasn’t essentially helped itself right here. Its try and disintermediate credit score bureaus and promote on to lenders may need accelerated this.

There’s additionally an AI risk. If synthetic intelligence makes it simpler to create rival merchandise, FICO’s pricing energy may evaporate. That’s why the inventory’s down. However analysts appear to suppose that rumours of this firm’s demise are vastly exaggerated.

Oversold?

FICO’s definitely beneath strain. However buyers shouldn’t suppose disrupting this enterprise can be easy. Getting a credit score rating prices a lender round $150 for a mortgage, $5 for a automobile mortgage, and $2 for a bank card. In comparison with the price of a default, that isn’t so much.

Meaning banks should take into account whether or not the financial savings through a less expensive product are actually value it. And they may not be.

With mortgages particularly, lenders usually need to resell the loans they originate. However this is likely to be tougher with no FICO rating. Cheaper options is likely to be coming, however value isn’t the one problem. And that’s what the inventory market is likely to be underestimating.

UK buyers

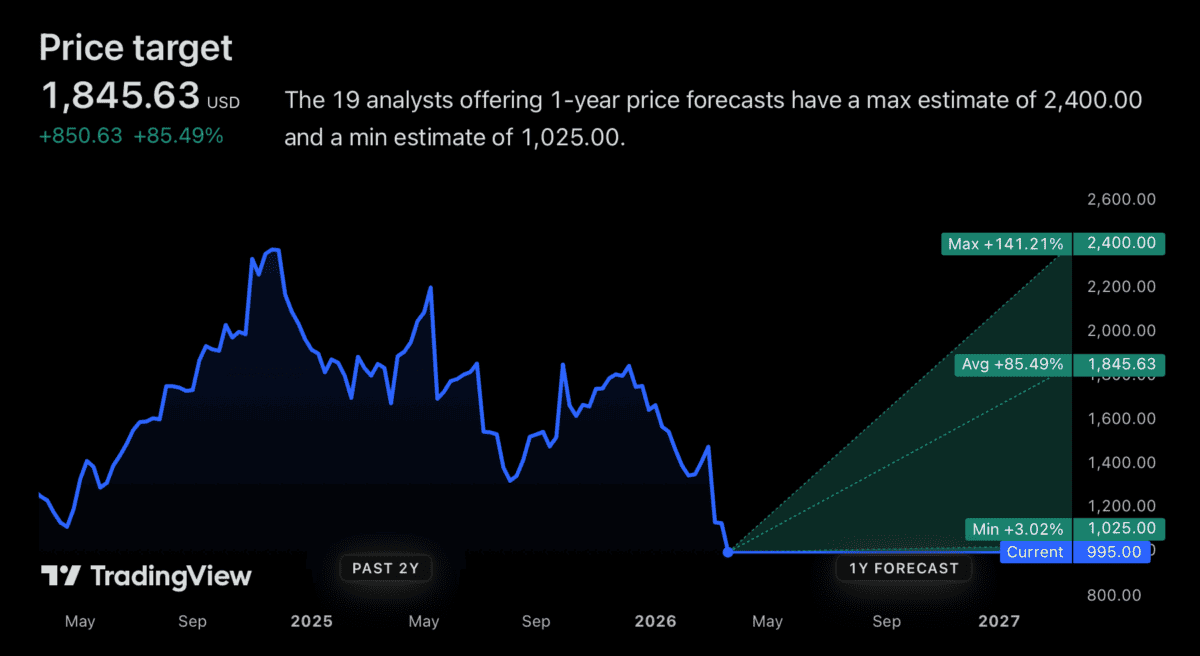

The common analyst value goal is 85% above the inventory’s present degree. That’s the best of any S&P 500 firm.

It might be an enormous alternative. However there’s one motive I’m not shopping for it in my very own portfolio. Share costs elsewhere have been falling and I can see extra apparent shares to purchase proper now. That’s all it comes right down to.

Assessing the dangers with FICO precisely is difficult for a UK investor like me. And I believe it’s essential to be trustworthy with myself about that.

The inventory is likely to be value contemplating in a market the place alternatives are scarce. However that’s not the state of affairs proper now. Consequently, I’m sticking to the place I can see the most effective worth. That’s what I believe the most effective buyers have all the time performed.