Picture supply: Getty Photos

It may be laborious to purchase shares when their costs are taking place. All of us love a cut price however few wish to purchase one thing that might be cheaper tomorrow or subsequent week.

However investing at occasions like these will be the important thing to incomes big returns. And I believe there are some terrific alternatives inside the FTSE 100.

A FTSE 100 titan

Among the finest examples is 3i (LSE:III). During the last 10 years, the non-public fairness agency has been one of many FTSE 100’s high performers and it’s simple to see why.

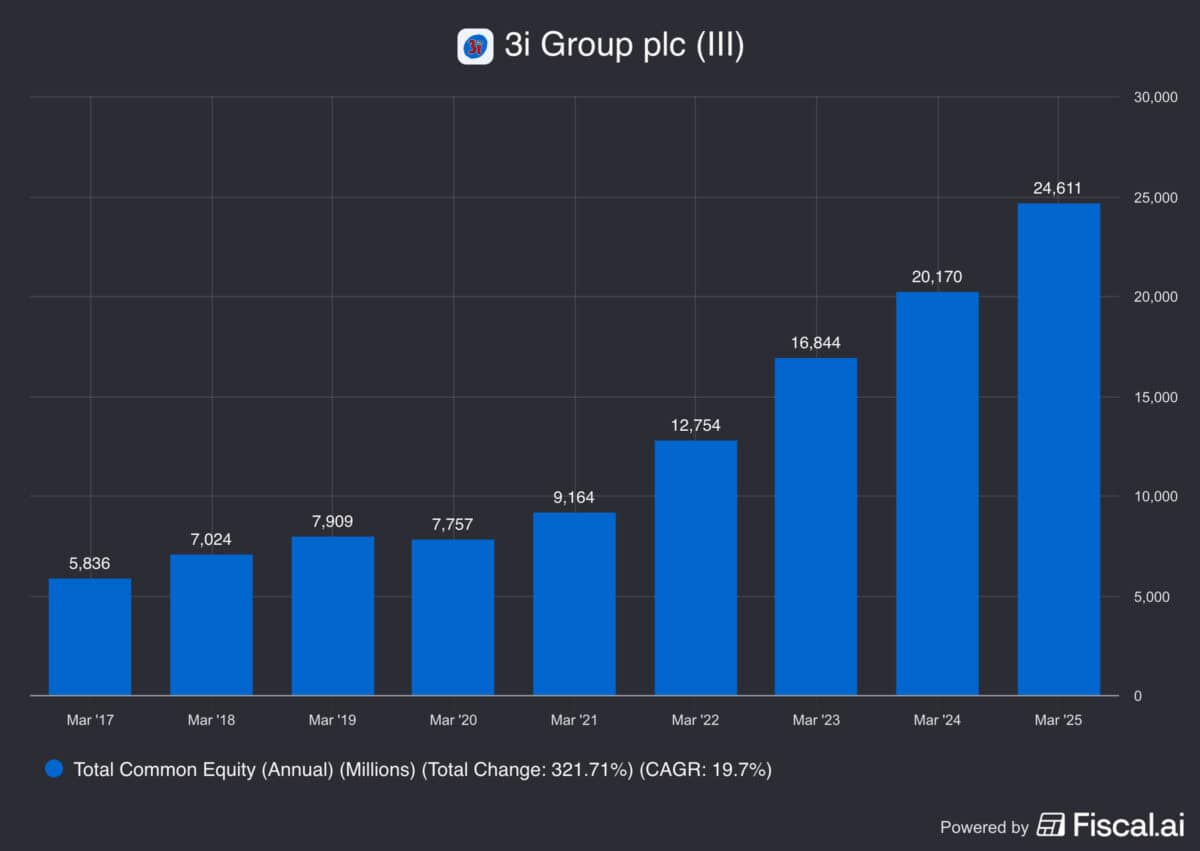

The corporate’s e book worth – the distinction between its belongings and its liabilities – has grown by 21% a yr on common. And it isn’t exhibiting indicators of slowing.

A number of this is because of Motion, 3i’s largest funding. The European retailer has grown strongly by means of a mixture of new openings and better same-store-sales.

Because of this, Motion makes up greater than 70% of 3i’s portfolio. That’s quite a bit, but it surely’s not an issue whereas the enterprise is performing properly.

Iran battle

Because of the battle in Iran, Qatar has halted liquefied pure fuel (LNG) manufacturing. And that’s an issue for Europe, which imports it.

Larger vitality costs are prone to create strain on family budgets. However that’s dangerous for Motion, which depends on client spending for its revenues.

3i values its stake in Motion at an EBITDA a number of of 18.5. That’s not outrageous, but it surely implies a optimistic view of the agency’s future progress prospects.

A fame for low costs ought to assist make Motion extra resilient. However given how a lot of 3i’s portfolio it makes up, buyers have to pay attention to the hazard.

Inventory down

The danger of LNG-related disruption is actual, however I don’t see it as a long-term menace to 3i’s key subsidiary. And I believe the discounted share worth offsets loads of this.

Only one month in the past, the inventory was buying and selling at a price-to-book (P/B) ratio of 1.2. After a 15% decline within the share worth, that a number of is now 1.

I believe that’s low-cost. I began shopping for the inventory at a P/B ratio of 1.2 with a view to the agency rising into its valuation inside a yr.

I’m nonetheless joyful shopping for it at that stage, however I prefer it much more at right now’s costs. Particularly with 3i’s long-term aggressive benefit intact.

Shopping for alternatives

3i’s key benefit is that it invests its personal capital, as an alternative of funds from shoppers. And which means it could actually purchase and promote when it chooses, not on mounted timelines.

That offers the corporate an enormous benefit over different non-public fairness companies. And LNG disruption doesn’t make any distinction to this.

Within the brief time period, there’s no rule saying the inventory can’t fall additional. It’s traded at a P/B ratio beneath 1 earlier than and it completely might achieve this once more.

From a long-term perspective although, I see the present disruption as a possibility. And that’s why it’s on my purchase listing proper now.