Picture supply: Getty Photographs

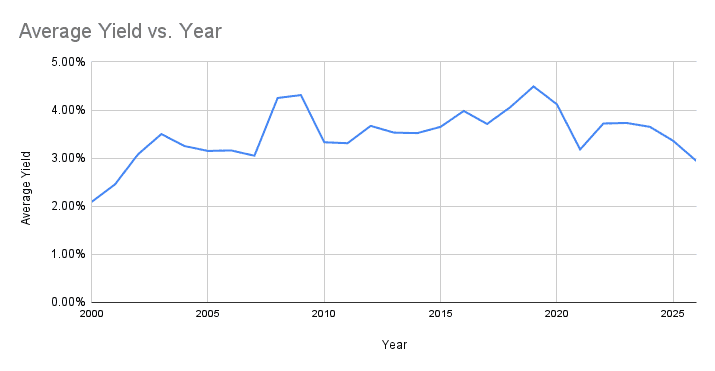

The FTSE 100‘s common dividend yield has dipped under 3% for the primary time since Covid, in keeping with knowledge from dividenddata.co.uk. For brief intervals in 2020 and 2021, the yield fell under 3% — however has largely remained above that common since 2002.

Created with knowledge from dividenddata.co.uk

Created with knowledge from dividenddata.co.uk

That’s a wake-up name for income-hungry retirement traders. With the Shopper Costs Index (CPI) at 3.4%, rates of interest at 3.75%, and the FTSE at highs over 10,200, is it the tip of UK shares as dependable revenue machines? Or is it a wholesome signal of capital development?

Why yields are falling

Low yields don’t sign weak spot – they’re really an indication of power. When share costs rise sooner than dividends develop, the yield naturally compresses. In 2025, mining, defence and finance helped the Footsie surge practically 20%, ramping up valuations. Whereas payouts stay strong (forecast 3.4% in 2026), index yields shrink as costs climb.

Zooming out, the macro image is encouraging. The OECD simply upgraded UK development to 1.2% for 2026, retail gross sales stunned to the upside (+0.4%), and shopper confidence hit its highest degree since August 2024. Inflation sits at 2.1%, the Financial institution of England base price is 3.75% (with cuts anticipated by the 12 months), and gilts yield round 3.5%.

Most significantly, whole returns (dividends plus worth development) have traditionally beat inflation by a rustic mile. So anybody nonetheless holding money financial savings might be shedding buying energy.

So is revenue useless?

I wouldn’t quit on dividend investing simply but. Even with index yields compressed, particular person UK shares nonetheless provide mouth-watering revenue. Take into account Admiral Group (LSE:ADM), the insurance coverage and worth comparability big. It yields round 6.7% with dividend cowl of 1.8 instances — that means payouts are safely lined by earnings. Higher but, it boasts over 20 years of uninterrupted dividend payouts.

A £100,000 holding in Admiral would generate £5,500 yearly, 100% tax-free inside an ISA. So it’s nonetheless an interesting inventory to think about for long-term dividend revenue. Plus, the corporate’s digital moat retains prices aggressive, including defensive prospects for an income-focused portfolio.

My solely concern could be regulatory scrutiny. Previously, the Monetary Conduct Authority (FCA) has flagged concern round premium finance merchandise — a key income for Admiral. If the FCA tightens regulation, or bans these practices outright, insurers may take a revenue hit, threatening dividend protection.

Stability it with development

For retirement savers with a 20-25-year outlook, development may compound more durable than revenue. For instance, a 1%-yielder with 12% annual NAV development beats a 6%-yielder with no development, full cease.

Dividend shares nonetheless maintain a crucial place in a portfolio geared toward passive revenue however development shares may pace up the journey. These hoping to seize one of the best of each worlds could take into account a tech-heavy development automobile like Scottish Mortgage Funding Belief.

This highly-diversified belief invests in corporations all over the world, together with prime S&P 500 names, non-public fairness corporations and rising market leaders.

So whereas yields could look low lately, my technique stays the identical: accumulate high quality dividend shares supported by defensive performs and powered by compounding development.