Picture supply: Nationwide Grid plc

Discovering shares to purchase is all about figuring out alternatives that different buyers are lacking. And I feel Nationwide Grid (LSE:NG) is one to take very significantly proper now.

The inventory doesn’t look thrilling. However the firm may be on the verge of the type of increase it hasn’t had within the final 10 years – and the market hasn’t clearly mounted on to this.

Development and worth

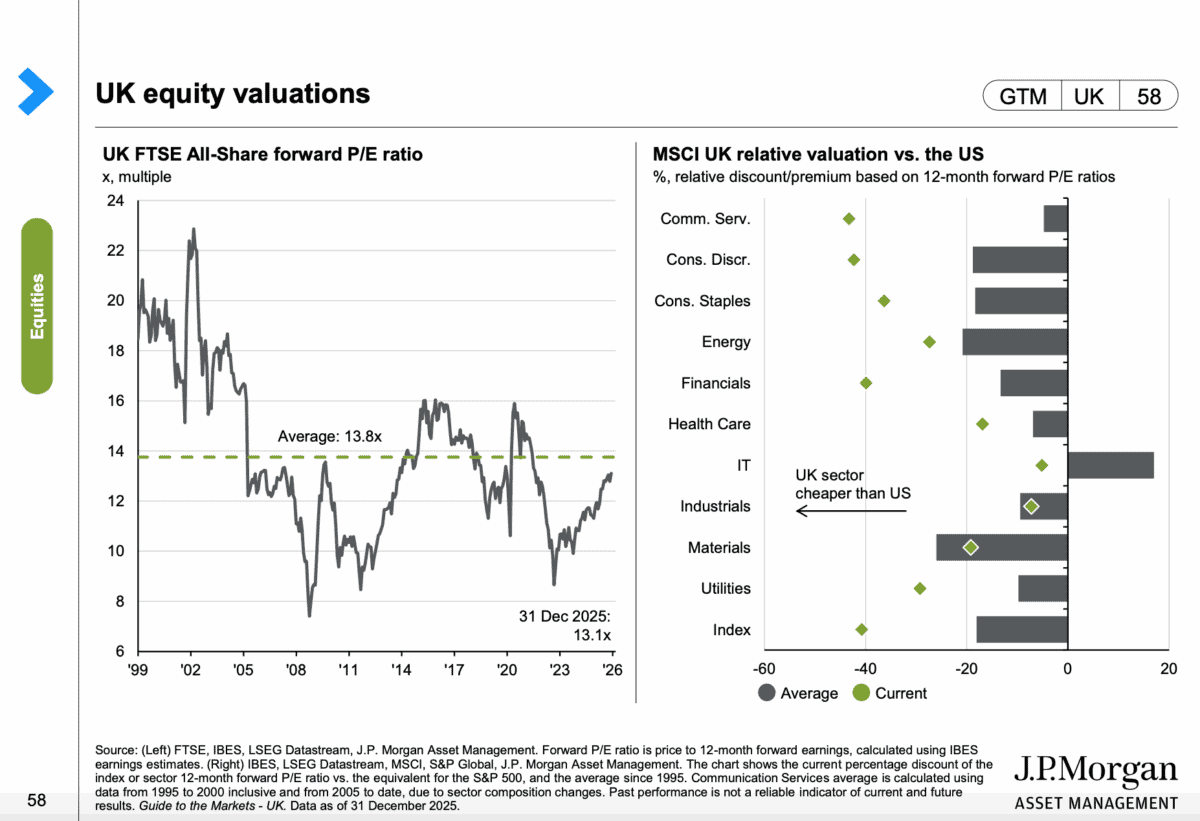

Regardless of the FTSE 100 outperforming the S&P 500 in 2025, UK shares nonetheless usually commerce at decrease price-to-earnings (P/E) multiples than their US counterparts. That’s true for nearly each sector in the intervening time.

Supply: JP Morgan Information to the Markets UK Q1 2026

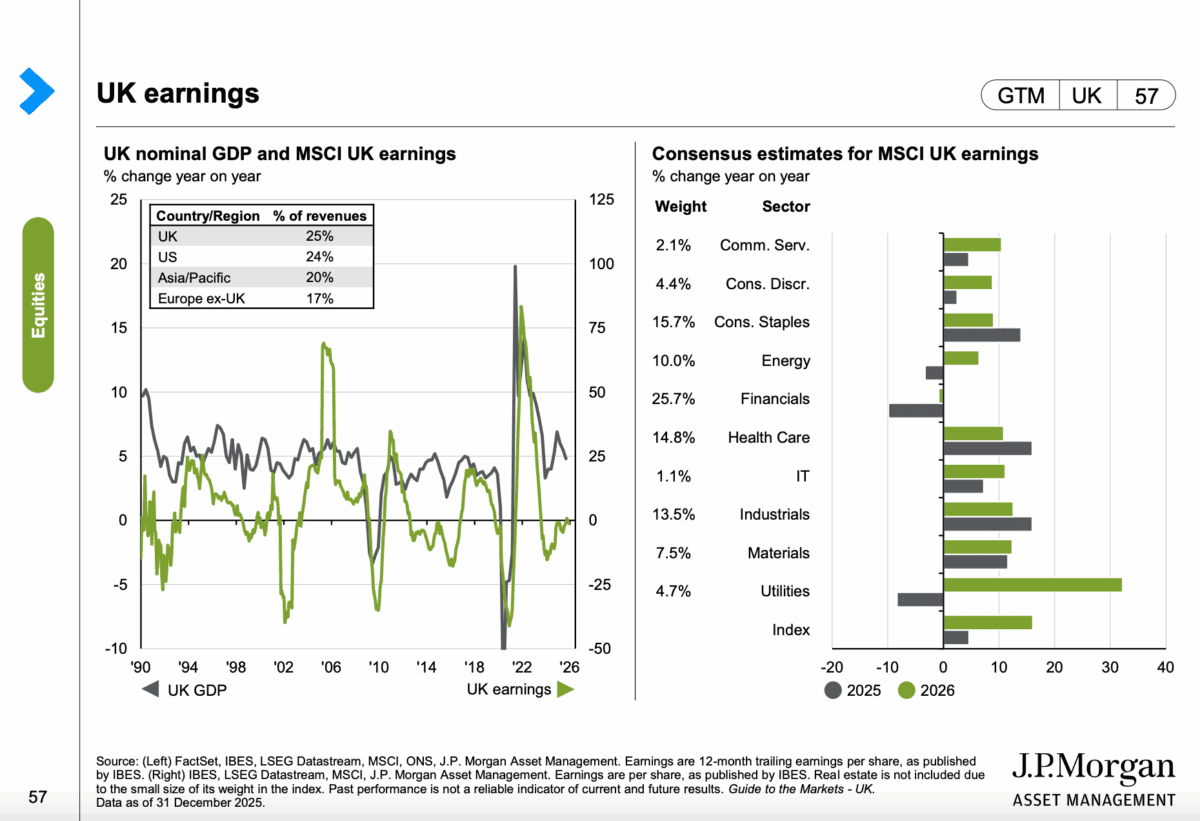

This makes an honest argument for investing throughout UK equities. However when it comes to progress forecasts for 2026, there’s one sector particularly that stands out.

Unusually, it’s the utilities sector. The regulated nature of their companies typically makes them dependable earnings investments, however an incapability to lift costs restricts their progress potential.

Supply: JP Morgan Information to the Markets UK Q1 2026

Analysts, nevertheless, expect an enormous enhance in earnings from UK utilities in 2026. And there are good causes for this, coming from the regulatory framework.

RIIO-T3

The massive increase is about to come back from the transition from RIIO-T2 to RIIO-T3 initially of April. In different phrases, Ofgem’s earlier regulatory framework is changed by a brand new one.

These frameworks specify the returns utilities companies are allowed to generate on their belongings going ahead. And importantly for Nationwide Grid, issues are set to search for.

The return on its electrical distribution belongings is about to extend from round 4.55% to six.12%. That’s a big shift that ought to lead to a considerable increase to earnings.

To some extent, the inventory market has been capable of see this coming. However the firm hasn’t had a lift like this within the final 10 years and valuations are nonetheless beneath their historic averages.

Lengthy-term investing

Nationwide Grid plans to take a position as much as £35bn over the following 5 years. And whereas that’s more likely to contain debt, so long as the price of that’s beneath the allowed return, the agency ought to do nicely.

There may be, nevertheless, a longer-term danger. Regulatory modifications can take returns down in addition to up and there aren’t any ensures about what would possibly occur past 2031.

If the following framework reduces the allowed return (which occurred in 2021) issues may develop into a lot trickier. And that’s the large danger buyers trying on the inventory must weigh up.

In the end, Nationwide Grid shareholders have to suppose in five-year cycles. So it’s price noting that whereas the outlook till 2031 is optimistic, issues develop into unsure after that.

A once-in-a-decade alternative?

Buyers haven’t had an opportunity to purchase Nationwide Grid shares earlier than a extra beneficial charge framework within the final 10 years. That’s price listening to.

On prime of this, UK shares are nonetheless buying and selling at an uncommon low cost to their US counterparts – even after final 12 months’s efficiency. And this consists of utilities.

Regulation means competitors is a non-issue, however it additionally limits returns. So whereas there’s an fascinating alternative proper now, formidable buyers would possibly take into account trying elsewhere.