A widening hole has emerged between the Federal Reserve and monetary markets over the trajectory of US rates of interest in 2026. Whereas the Fed indicators warning on additional cuts, markets are betting on two to 3 reductions this 12 months.

On the coronary heart of this disconnect lies an uncomfortable paradox: President Donald Trump’s push for decrease charges could also be undermined by the very inflation that threatens his political survival.

Markets Are Betting on Fee Cuts by Mid-12 months

In response to prediction market platform Polymarket, the chance of a charge minimize on the January Federal Open Market Committee (FOMC) assembly stands at simply 12%. Most members anticipate charges to stay unchanged this month.

However the image shifts dramatically over an extended horizon. The chance of a charge minimize by April rises to 81%, and by June it reaches 94%. For the total 12 months, a two-cut situation instructions the best chance at 24%, adopted by three cuts (20%) and 4 cuts (17%). Mixed, the chance of two or extra cuts exceeds 87%.

Sponsored

SponsoredSupply: Polymarket

The CME FedWatch software, which displays expectations embedded in rate of interest futures, paints the same image. The chance of a January maintain stands at 82.8%, carefully matching Polymarket. The chance of a minimum of one minimize by June is 82.8%, whereas the chance of two to 3 cuts by year-end reaches 94.8%.

The market consensus is obvious: maintain in January, start slicing within the first half, and ship two to 3 reductions by December.

Fed Hawks Sign No Rush

Contained in the Fed, nevertheless, a special narrative is taking form. On January 4, Philadelphia Fed President Anna Paulson indicated that additional charge cuts is probably not acceptable till “later in the year.”

Paulson, who holds a voting seat on the 2026 FOMC, acknowledged that “some modest further adjustments to the funds rate would likely be appropriate later in the year” — however provided that inflation moderates, the labor market stabilizes, and progress settles round 2%. She described the present coverage stance as “still a little restrictive,” suggesting it continues to work towards reducing inflation pressures.

Her remarks stand in stark distinction to market expectations of a first-half charge minimize. The message from the Fed’s hawkish camp is obvious: don’t anticipate motion anytime quickly.

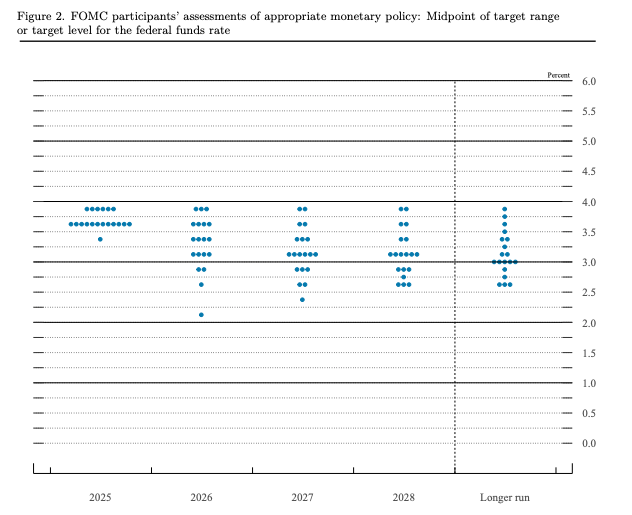

December FOMC: A Divided Committee

The December FOMC assembly revealed simply how fractured the Fed has turn out to be.

The committee minimize charges by 25 foundation factors, bringing the goal vary to three.5-3.75%. However the vote break up 9-3, a wider margin than the earlier 10-2 resolution. Two members, Schmid and Goolsbee, most popular to carry charges regular. On the opposite finish, Miran — broadly considered as aligned with the Trump administration — pushed for a 50-basis-point minimize.

or goal degree for the federal funds charge. Supply: FedSponsored

Sponsored

The dot plot advised an much more revealing story. Whereas the median projection pointed to only one minimize in 2026, the distribution was in depth. Seven officers projected no cuts in any respect, whereas eight noticed two or extra reductions. Essentially the most dovish projection prompt charges might fall as little as 2.125%.

The Fed’s official steering says one minimize. Markets are pricing in two. Why the persistent hole?

Why Markets Are Betting on the Doves: The Trump Issue

The first purpose markets refuse to just accept the Fed’s hawkish steering is President Donald Trump.

Since returning to the workplace, Trump has constantly pressured the Fed for decrease charges. The December FOMC vote — the place a Trump-aligned official pushed for aggressive easing — exemplifies this dynamic.

Extra importantly, Fed Chair Jerome Powell’s time period expires in 2026. The facility to appoint his successor rests with the President. Market members broadly anticipate Trump to nominate somebody extra sympathetic to his desire for looser financial coverage.

Structural elements reinforce this view. The Fed has traditionally pivoted to charge cuts when the labor market weakens. FOMC divisions are deepening. And there are issues that tariff insurance policies might gradual financial progress, including stress for financial easing.

The market’s wager is simple: Trump’s stress, mixed with a possible financial slowdown, will ultimately power the Fed’s hand.

Sponsored

Sponsored

The Midterm Paradox: Inflation Is Trump’s Achilles’ Heel

Right here lies the central irony. For Trump to successfully stress the Fed, he wants political capital. However that capital is eroding — due to inflation.

Current polling exhibits Trump’s approval score on financial coverage has fallen to 36%. In a PBS/NPR/Marist survey, 57% of respondents disapproved of his financial administration. A CBS/YouGov ballot discovered that fifty% of People say their monetary scenario has worsened underneath Trump’s insurance policies.

This discontent is already displaying up on the poll field. In final November’s New York Metropolis mayoral race, Democratic state assemblyman Zohran Mamdani gained on a platform of constructing town extra inexpensive. Democratic candidates additionally captured governorships in Virginia and New Jersey by emphasizing cost-of-living reduction.

With midterm elections approaching in November, over 30 Republican Home members have already introduced they gained’t search re-election. Political analysts more and more predict a Republican defeat and a possible lame-duck situation for Trump.

Three Eventualities, No Simple Path

The intersection of financial coverage and electoral politics produces three potential situations for 2026 — none of which give Trump all the pieces he desires.

Situation 1: Inflation stays elevated. Trump faces political dangers, doubtlessly dropping the midterms and getting into lame-duck standing. However excessive inflation additionally means the Fed has no justification to chop charges. Trump’s weakened place additional diminishes his capacity to stress the central financial institution.

Situation 2: The financial system cools sharply. Trump faces an excellent worse political blow as voters punish him for a weakening financial system. Nevertheless, the Fed beneficial properties a transparent rationale for charge cuts to help progress.

Sponsored

Sponsored

Situation 3: Mushy touchdown with moderating inflation. Trump’s political standing could get better as financial anxieties ease. However with the financial system performing nicely, the Fed has little purpose to chop charges.

In none of those situations does Trump obtain each political energy and decrease rates of interest. The 2 objectives are basically at odds.

The Information That Will Determine Every part

Upcoming financial releases will function the decisive variables shaping each Fed coverage and Trump’s political destiny.

Client Value Index (CPI): A decline would strengthen the case for charge cuts and supply Trump with political reduction. An increase would constrain the Fed and intensify voter backlash in opposition to the administration.

Producer Value Index (PPI): As a number one indicator of client costs, a falling PPI would sign future CPI moderation. Rising PPI might point out that tariff-driven worth pressures are materializing.

Employment knowledge (NFP, unemployment charge): Weakening labor markets would enhance stress on the Fed to chop — however would additionally injury Trump’s financial file. Secure employment would give the Fed cowl to take care of its cautious stance.

Conclusion

The Fed is signaling one charge minimize in 2026. Hawks like Paulson recommend even that won’t come till the second half. But markets proceed to cost in two to 3 cuts, betting that Trump’s stress and the Powell succession will finally push the Fed towards easing.

However right here’s the paradox: persistent inflation erodes Trump’s political standing, which in flip weakens his leverage over the Fed. The very situations that make charge cuts politically fascinating for Trump additionally make them economically unjustifiable — or strip him of the facility to demand them.

“It’s the prices, stupid” applies to Trump, to the Fed, and to market members alike. In the long run, inflation and employment knowledge will concurrently decide the trail of US rates of interest and the end result of November’s midterm elections. Trump might want each political survival and decrease charges, however the financial system is unlikely to grant him that luxurious.