Picture supply: Getty Pictures

Once I was younger, my father would spend hours on the telephone to brokers discussing share investing. I assumed it sounded terribly boring however little did I do know he was working in direction of a important purpose: constructing a second revenue.

Now, years later, I see the fruits of his labour — he lives a cushty retirement, touring commonly with seemingly no monetary worries.

It’s a preferred purpose amongst UK traders — buy shares in dividend-paying firms and watch the common revenue movement in. For many individuals, that is seen as a solution to complement their pension so that they don’t must preserve working previous retirement age.

However how straightforward is it to really make that occur? Let’s break down how a lot cash is required to retire early and a attainable technique to get there.

Practical targets

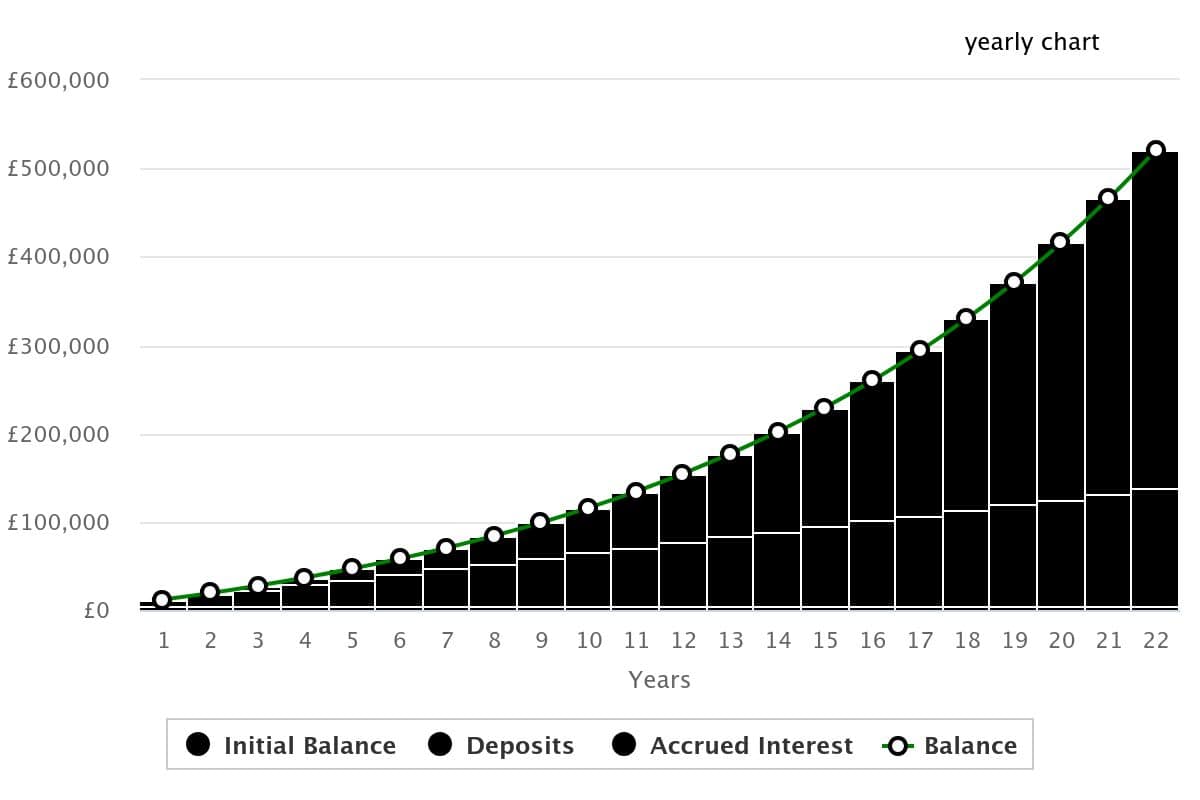

Since dividends are paid as a proportion of cash invested, the very first thing is to work out how a lot is required. For instance, 5% of 500,000 is 25,000. So a £500,000 portfolio of shares with a mean yield of 5% would pay out £25,000 a 12 months.

Engaged on these averages, how lengthy would it not take to avoid wasting £500,000? Even saving £500 each month would take 1,000 months, or 83 years! Fortuitously, the miracle of compounding returns would drastically scale back that timeline.

Good traders with a well-balanced portfolio sometimes obtain a mean return of round 10% a 12 months. With a £5,000 preliminary funding and £500 month-to-month contributions, it will take lower than 22 years to achieve £500,000.

Now that’s extra prefer it!

Created on the thecalculatorsite.com

Created on the thecalculatorsite.com

3 starter shares to contemplate

Over time, I’ve rebalanced my revenue portfolio a number of instances however three shares that stay everlasting fixtures are Unilever, Authorized & Common and HSBC (LSE: HSBA). Collectively, they provide a mixture of defensiveness, excessive yield and world publicity.

As a multinational financial institution with a £182.4bn market-cap and 4.7% yield, HSBC embodies all three of those traits. These days, Lloyds has been outshining HSBC in each progress and dividends, however the long-term outlook paints a special image.

With nicely over 20 years of uninterrupted funds, its dividend observe file beats most rivals. And regardless of weak efficiency this 12 months, its 10-year progress outpaces Lloyds, Barclays and NatWest.

That’s the form of reliability I’m searching for when considering of retirement revenue.

Nonetheless, previous efficiency doesn’t assure something and HSBC nonetheless faces notable dangers. The important thing being its latest makes an attempt to divide East and West operations — a pricey effort that might trigger disruption. Execution is important right here because the transfer has already irked traders and any revenue miss may danger a adverse market response.

However for now, issues look good and I’m optimistic in regards to the eventual consequence.

Closing ideas

When constructing an revenue portfolio, don’t simply purpose for the very best yields. It pays to have a basis of defensive shares in industries that preserve demand even throughout market downturns.

Diversification is equally as essential to cut back the danger of localised losses in a single sector or area. These three firms are good examples of shares value contemplating for a newbie’s portfolio.

They’ll function a place to begin to discovering firms with related traits, with the purpose to construct up a portfolio of 10-20 shares.