Picture supply: Getty Pictures

On the time of writing (1 December), Lloyds Banking Group (LSE:LLOY) shares are altering palms for round 95p. This implies they’re simply 5.3% away from reaching the psychologically necessary barrier of £1.

Will they get there? Or might they go in the wrong way? Let’s assessment the proof.

The bearish view

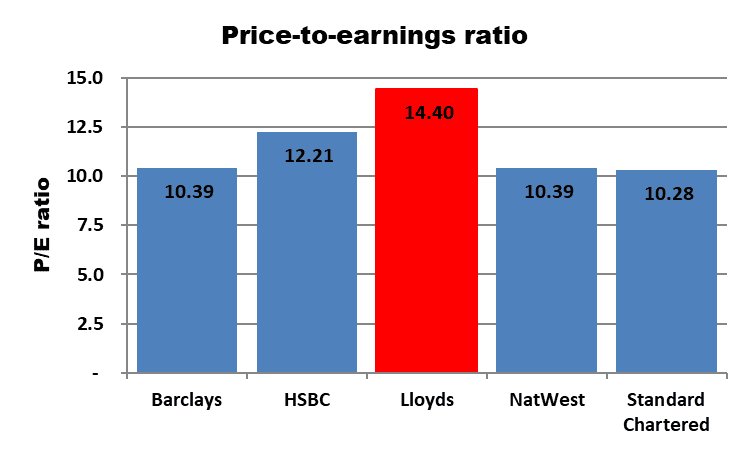

Primarily based on the ahead (2025) price-to-earnings (P/E) ratios of the FTSE 100’s 5 banks, Lloyds’ shares are the costliest. In the event that they had been rated consistent with the typical, they might be round 25% cheaper, at 76p.

Supply: London Inventory Trade Group/firm stories

Supply: London Inventory Trade Group/firm stories

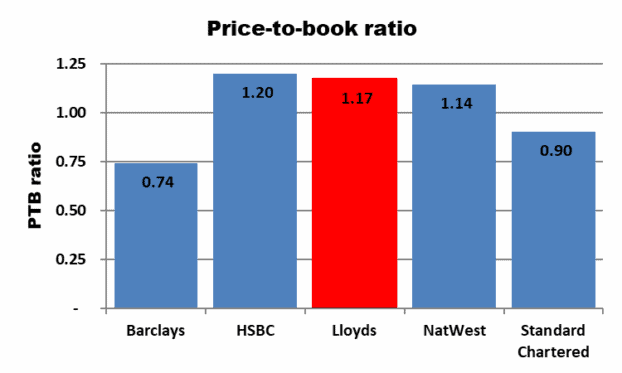

Wanting on the stability sheets of the 5, Lloyds is the second costliest. It has a price-to-book (PTB) ratio of 1.17. In keeping with McKinsey & Firm’s newest analysis on the worldwide banking trade, the typical PTB for the sector is one. In different phrases, banks are typically valued consistent with their web asset worth.

Supply: London Inventory Trade Group/firm stories

Supply: London Inventory Trade Group/firm stories

This may sound affordable however many industries entice far greater valuations. McKinsey’s report cautions that buyers seem like questioning the “sustainability of bank’s recent highs”. It blames “declining interest rates [and] shifts in technology and consumer behaviour”. The administration consultancy additionally notes that fintechs, non-public credit score corporations, and wealth managers are gaining clients from extra conventional monetary establishments.

So Lloyds may not have the ability to command a inventory market valuation considerably greater than its accounting worth.

Additionally, its near-total reliance on the UK financial system for its revenue may very well be an Achilles’ heel. Final week’s Finances noticed progress forecasts for 2026 and past downgraded.

The bullish view

If the analysts are right, the financial institution’s latest share worth rally isn’t over but. They’ve a median 12-month share worth goal of 99.5p. Okay, that’s in need of the magic three figures but it surely’s shut sufficient. Essentially the most optimistic forecast suggests 110p is a good worth.

This rosy image is underpinned by an expectation that, in comparison with 2024, earnings per share can have grown 79% by 2027.

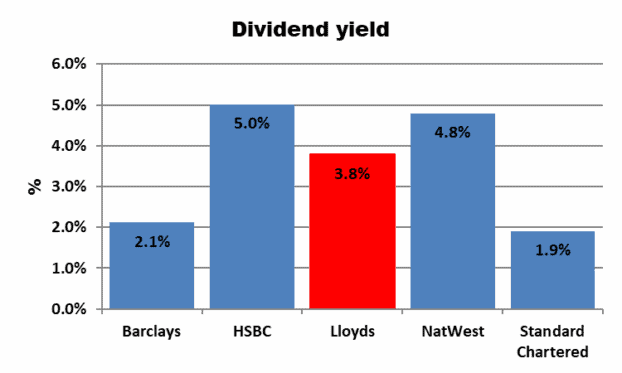

And the inventory’s good for revenue too. Primarily based on the previous 12 months, it’s yielding 3.8%. Though it’s at present not the best of the 5, brokers expect its dividend to extend by 51% over the subsequent three years. This provides it a ahead yield of 5.1%.

Supply: London Inventory Trade Group/firm stories

Supply: London Inventory Trade Group/firm stories

My view

On reflection, I’m leaning extra in direction of the bearish arguments. I already suppose Lloyds shares are on the costly facet so I reckon the scope for additional progress’s restricted. That’s why the inventory’s not for me.

Having mentioned that, I wouldn’t be stunned if the shares did attain 100p earlier than the tip of 2025. However for them to go a lot greater, I believe one thing pretty important has to occur. Nevertheless, the one main occasions I can see occurring are unfavourable ones, centring on the UK financial system, which seems fragile.

Regardless of my issues, I don’t suppose the shares will fall as little as 76p. The financial institution stays standard with smaller buyers – it has extra shareholders than every other firm within the nation – and its earnings are rising. This could assist help its share worth.

And though I’ve issues about Lloyds’ valuation, I nonetheless suppose it’s a well-run high quality firm. I simply suppose the FTSE 100’s different banks look a bit cheaper in the intervening time.