Picture supply: Getty Photos

Defence shares have recorded gorgeous share value good points since Russia’s invasion of Ukraine virtually 4 years in the past. BAE Programs’ (LSE:BA.) share value is up a whopping 200% since then. And it’s exhibiting no indicators of slowing.

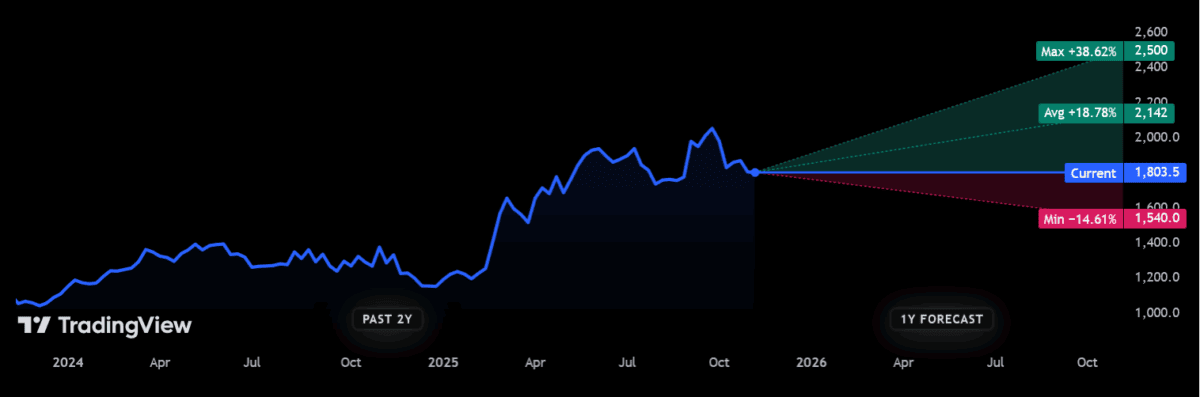

At £18.04 per share, the FTSE 100 weapons builder has risen 56% thus far in 2025. If Metropolis brokers are appropriate, BAE shares will proceed to soar throughout the subsequent yr.

£21 goal

As we speak, 12 analysts have scores on the defence large, offering a very good vary of opinions. The consensus amongst them is that its shares will rise by double-digit percentages over the following yr:

Supply: TradingView

Supply: TradingView

The 12-month value goal on BAE shares is £21.42, representing an 18.8% premium from present ranges. If dealer estimates for dividends are additionally correct, traders can count on a complete return a shade under 21% over the following yr.

However in fact share value and dividend forecasts are by no means assured. As you may also see from the graph, there are additionally some considerably completely different viewpoints from Metropolis analysts regarding BAE’s share value.

Can the corporate actually hit the heights that brokers anticipate?

Robust numbers

BAE mentioned that it continues to get pleasure from “positive momentum in order intake,” racking up £27bn value of contracts within the yr thus far. It commented that additional agreements are anticipated earlier than the top of 2025.

The weapons maker added that “our order backlog, pipeline of labor on incumbent positions and increasing alternatives for brand spanking new work present good visibility for long-term progress“.

The corporate mentioned it’s on the right track to hit its full-year targets that have been upgraded in July. The enterprise has tipped gross sales progress of 8%-10%, and underlying EBIT progress of 9%-11%.

Nice reception

BAE’s replace — maybe unsurprisingly — drew constructive reactions from Metropolis brokers.

Garry White, analyst at Charles Stanley, mentioned BAE’s replace “reinforced its status as one of the FTSE 100’s standout performers, with strong revenue growth and a bulging order book underscoring the global surge in defence spending.”

He famous that “BAE’s challenge is not demand, it is delivery [while] management needs to keep costs under control and deliver on time.”

But White added that, regardless of these execution dangers, the corporate’s third-quarter replace “reinforces the positive investment case surrounding its shares.”

Is BAE a purchase?

BAE’s replace underlines the robust momentum the defence share continues to expertise going into 2026. As White describes, provide chain and value points stay issues it must maintain a decent leish on. The corporate additionally faces vital competitors on contracts, significantly from US friends.

However on stability, I imagine BAE seems to be in nice form to file additional value good points, making it value severe consideration.

As a important provider to armed forces within the West, it’s within the field seat to get pleasure from sustained demand progress by the following decade. NATO members have pledged to steadily increase core defence spending to three.5% of their GDPs by 2035, up from 2% as we speak. This implies lots of of billions extra kilos flooding into the trade.

BAE’s share value seems to be costly by historic requirements. The agency’s ahead price-to-earnings (P/E) ratio is now 24.1 instances, above the 10-year common of 14 instances. Nonetheless, I believe this ranking pretty displays the FTSE agency’s generational earnings alternatives proper now.