Picture supply: Getty Pictures

Aviva (LSE:AV.) shares have delivered a powerful long-term return. As soon as seen as a boring revenue inventory, the share value has risen 56% over 5 years, turning a £7,500 funding into £11,700.

However that’s solely a part of the story. Over the identical interval, buyers would even have acquired £3,025 in dividends, lifting the full return to virtually double the unique funding. Not dangerous for a ‘boring’ inventory. The problem now could be whether or not the insurer can maintain compounding from right here.

Rising dividend

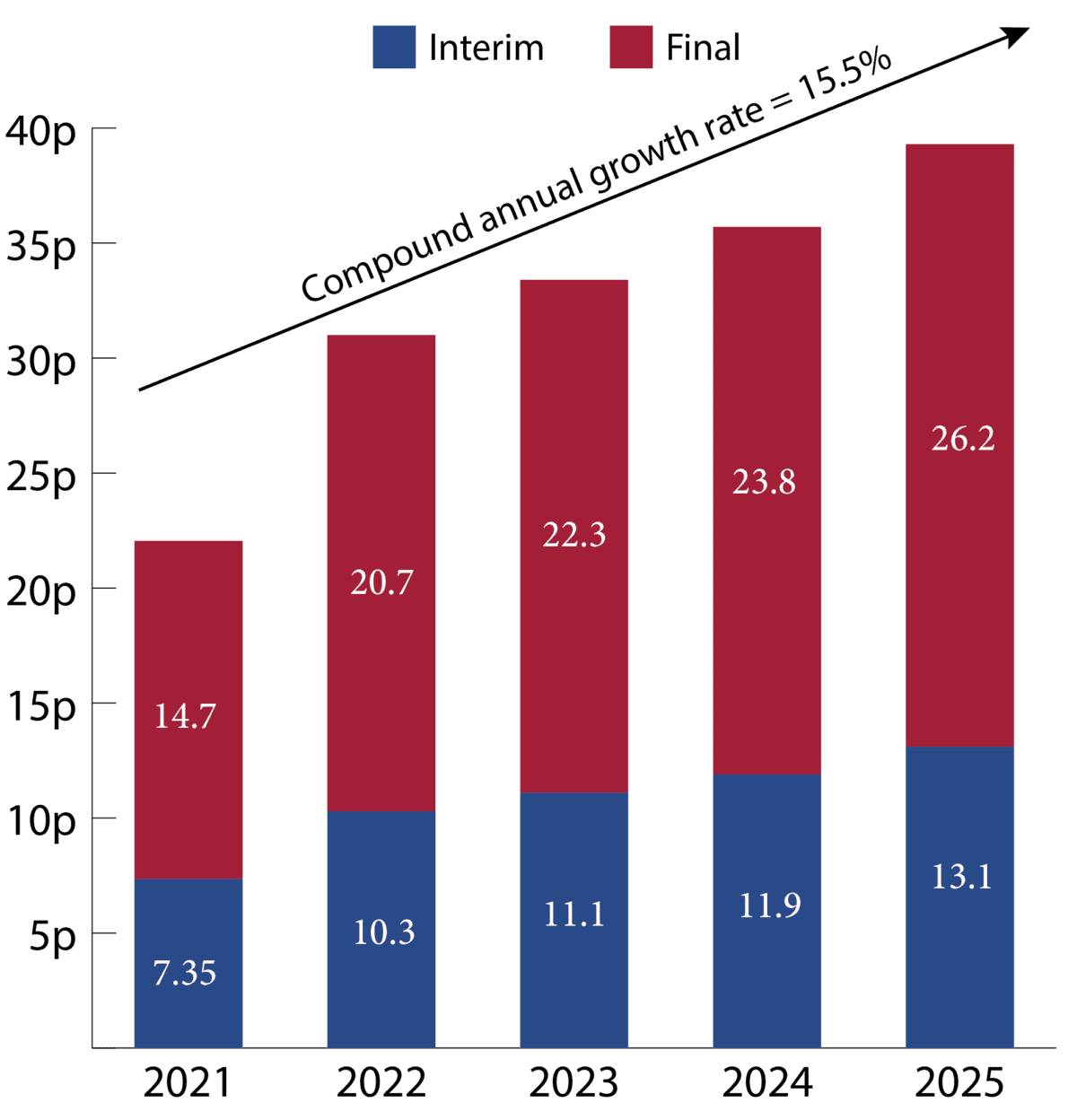

As the next chart exhibits, the corporate has delivered robust dividend compounding in recent times, with dividends per share rising at a compound annual charge of 15.5%.

Chart generated by creator

This has not come from luck or one-off good points. It displays a deeper shift going down throughout the enterprise because it strikes in direction of a extra capital-light mannequin.

That shift issues as a result of it modifications the standard of the earnings base supporting the dividend. Moderately than relying purely on conventional, capital-heavy insurance coverage returns, a rising share of income now comes from wealth, pensions and fee-based companies.

These areas generate extra predictable money flows and require much less steadiness sheet pressure, which in flip helps increased and extra sustainable capital returns over time.

In easy phrases, the corporate isn’t simply paying a dividend — it’s steadily constructing the capability to develop it.

Diversified enterprise mannequin

What stands out in Aviva’s newest replace is how broad-based the progress has change into. Administration has already delivered its 2026 targets a full 12 months early and has upgraded its medium-term ambitions. That issues as a result of it alerts execution is operating forward of expectations.

Crucially, all elements of the enterprise at the moment are firing on all cylinders. Common insurance coverage continues to learn from scale benefits and disciplined underwriting. Wealth is rising strongly, supported by rising inflows and belongings. Retirement and safety additionally proceed to ship regular, recurring earnings.

In different phrases, that is now not a single-driver insurance coverage story.

The important thing takeaway is that efficiency is now coming from throughout the group on the identical time, somewhat than counting on one core engine. That creates a extra resilient and self-reinforcing earnings base.

The result’s a enterprise that’s not simply rising, however compounding sooner than the market presently expects.

What might go fallacious?

The primary danger for Aviva is now not whether or not the enterprise is bettering (it clearly is) however whether or not an excessive amount of of that enchancment is already mirrored in expectations.

The group has already delivered its 2026 targets forward of schedule, which raises the bar for future efficiency. At this stage, even a small slowdown in earnings momentum or capital era might result in volatility in sentiment.

There are additionally extra conventional dangers. Insurance coverage profitability may be impacted by increased claims inflation, notably in motor and well being. Funding returns additionally stay delicate to actions in bond yields and wider monetary markets.

Backside line

Aviva has already delivered a big transformation in recent times, and the monetary outcomes more and more replicate that shift.

The important thing query for buyers is whether or not the corporate’s enchancment is already mirrored within the share value. With earnings momentum, capital power and diversified money era all shifting in the fitting path, it’s actually a enterprise buyers could wish to take a more in-depth have a look at. Nevertheless it’s not the one alternative on my radar proper now.