Picture supply: Getty Photographs

After rising practically 500% in a decade, Greggs‘ (LSE:GRG) shares began crashing in direction of the top of 2024. This coincided with new authorities plans to extend enterprise tax.

Since October 2024, when Chancellor Rachel Reeves introduced a hike in Employers’ Nationwide Insurance coverage and lowered the edge, Greggs’ shares have crashed 42%. This may have turned a £5,000 funding into £2,900, excluding dividends.

Not solely did the Finances enhance Greggs’ staffing prices, it arguably had a chilling impact on the UK financial system. Many companies paused hiring, pushing up unemployment, which now stands at a five-year excessive.

In 2023, Greggs’ complete and like-for-like (LFL) gross sales jumped 19.6% and 13.7% respectively. In 2025, these figures had been 6.8% and a couple of.4%, with underlying working revenue falling 4% to £188m.

Greggs below stress

Within the first 9 weeks of 2026, LFL progress slowed even additional, to 1.6%. And Greggs can’t appear to catch a break, with the Iran conflict now anticipated to ship vitality, meals and gasoline prices increased.

And regardless of the FTSE 250 firm opening 121 web new shops final 12 months, and planning an identical quantity this 12 months, buyers concern we’ve reached ‘peak Greggs’. Can the model actually hit 3,000+ areas with out cannibalising current retailer gross sales? The market clearly isn’t satisfied.

On high of this, the rise of GLP-1 medicine akin to Mounjaro is forcing the corporate to adapt its menu. In consequence, there are as many egg pots within the fridge in Greggs these days as there are sausage rolls behind the glass counter.

The rising use of GLP-1 medicine for weight reduction is reshaping consuming habits and lowering demand for calorie-dense meals. We analysis these developments and innovate with merchandise that help satiety and balanced vitamin, together with objects which can be excessive in fibre, plant-based and protein-rich.

Greggs 2025 annual report.

Is the baker vulnerable to shedding its identification with this push in direction of more healthy meals? It’s doable.

To summarise then, there are a mess of issues weighing on the share value at present:

- Slowing progress.

- Earnings below stress.

- Rising UK unemployment.

- Ongoing price of residing pressures.

- Peak Greggs considerations.

- Declining excessive road footfall.

- Potential GLP-1 impression.

Attributable to a few of these elements, Greggs is at the moment the UK’s third most-shorted inventory behind Ibstock and Wizz Air. So refined buyers are betting there’s extra ache to come back.

Not all doom and gloom

Regardless of the apparent challenges, Greggs nonetheless has many enticing qualities. It possesses a singular model, sturdy steadiness sheet, and industry-leading revenue margins (even after current stress).

Plus, there’s a well-covered ahead dividend yield of 4.2%. That’s above the FTSE 250 common.

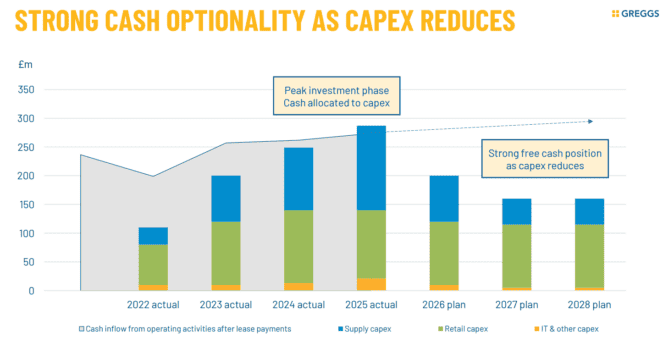

It’s additionally price mentioning that capital expenditure peaked final 12 months, which ought to end in considerably improved money stream transferring ahead. And robotic order selecting in considered one of its two new state-of-the-art distribution centres opening quickly ought to enhance effectivity.

Supply: Greggs

Supply: Greggs

One other factor I like is that round 20% of outlets are actually franchised (managed by third-party companions). These are inclined to outperform company-managed outlets, as they’re primarily centered on roadside areas. They usually additionally choose up the day-to-day working prices (hire, electrical energy, and so forth).

Lastly, the shares look low-cost now. Primarily based on forecasts for 2027, the forward-looking price-to-earnings ratio’s 12.5.

For affected person buyers with a multi-year investing horizon, I believe the inventory’s now a shopping for alternative price desirous about.