Picture supply: Getty Photos

FTSE 250 buyers will know Greggs (LSE:GRG) shares have been a dumpster fireplace over the past 12 months. I actually have had my fingers burned within the chaos — I opened a place within the battered baker in November 2024, and added to my place two months later.

Since 1 January, Greggs’ share value has crumbled like one its pastries, to £16.41. That represents a 42% decline, and means a £5,000 funding at first of the 12 months would now be value simply £2,900.

Challenges stay as UK customers preserve their purse-strings tightened. Nevertheless, if Metropolis analysts are right, the corporate may very well be on the verge of a spectacular restoration.

So simply how a lot money may buyers make by this time subsequent 12 months?

29% value rise?

Greggs shares are adopted by a big listing of analysts. Considered one of these is JP Morgan, which started protection this month and — encouragingly — connected an Obese ranking to the inventory.

It predicted a rebound in earnings and free money movement from 2026, pushed by bettering shopper spending energy. It additionally praised Greggs as a “structural winner” that enjoys quite a few market-leading metrics together with

gross revenue per sq. foot, underlying revenue per sq. foot, income per working lease, and gross revenue per working lease.

The baker’s valuation is now at “trough” ranges, JP Morgan stated, because it approaches the underside finish of its income cycle. With the outlook brightening, a pointy rebound in Greggs shares is tipped.

It set a two-year share value forecast of £21.10 on Greggs. This implies a possible rise of 29% from present ranges.

Dust low cost

Based mostly on this forecast, somebody shopping for £5,000 of Greggs inventory in the present day would make £6,426 (excluding dividends).

Wanting on the rock-bottom valuation JP Morgan mentions, it’s simple for me as cut price lover to get excited.

Right now Greggs’ price-to-earnings (P/E) ratio (on a forward-looking foundation) is 13 instances. That’s considerably under the 10-year common of twenty-two.4 instances.

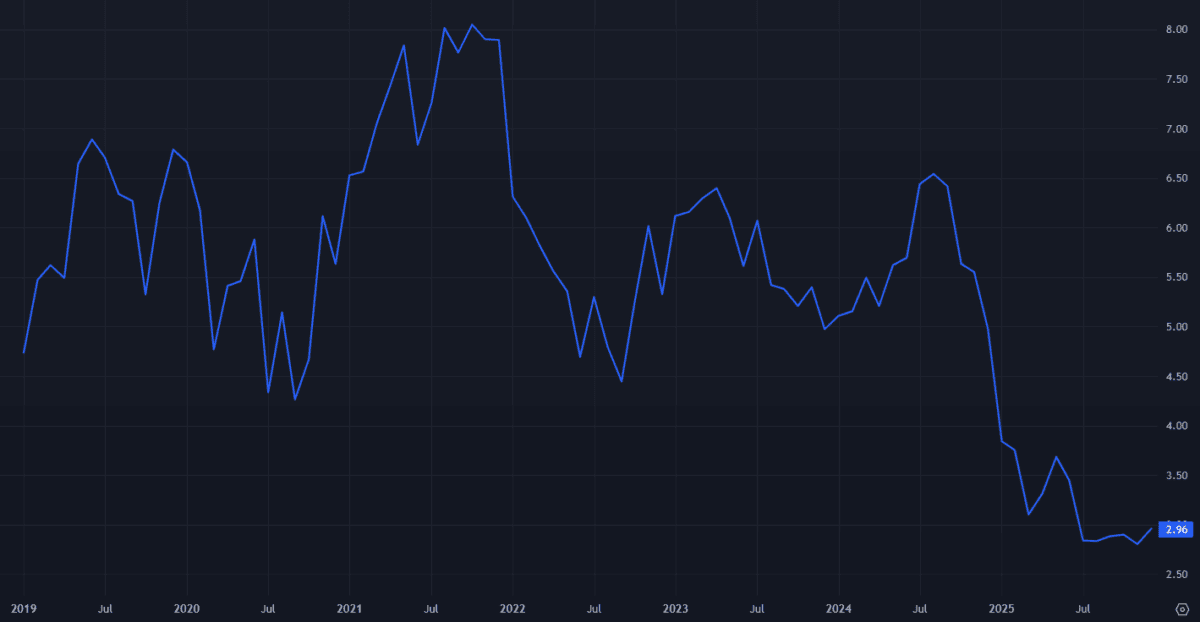

In the meantime, the corporate’s price-to-book (P/B) ratio has toppled to round thrice. It suggests Greggs nonetheless trades at a premium to its asset values — this displays partly its industry-leading metrics.

However as you may see, that is additionally spectacularly low from a long-term perspective.

The P/B ratio of Greggs shares. Supply: TradingView

The P/B ratio of Greggs shares. Supply: TradingView

Is Greggs a Purchase?

There are clear dangers to Greggs’ restoration, from the difficult shopper panorama to intense market competitors. Rising prices are one other downside it must navigate.

But I’m assured gross sales and income will spring increased from subsequent 12 months. I believe hikes to the minimal wage may increase demand for its sausage rolls and candy treats. Ongoing retailer growth — and particularly in high-footfall areas like journey hubs — must also help earnings progress subsequent 12 months and past.

My possession of Greggs shares hasn’t obtained off to a very good begin. However I’m assured my funding will ship glorious returns over the long run. Whereas not with out threat, I believe it’s a prime inventory to contemplate.