Practically $2.5 billion in Bitcoin and Ethereum choices expire right now, organising a doubtlessly risky finish to the month as merchants juggle upside bets with deep draw back insurance coverage.

On the floor, positioning seems constructive. However beneath the call-heavy skew lies a placing anomaly: one of many largest open curiosity clusters in Bitcoin sits far under spot — on the $40,000 strike.

Calls Dominate, However Max Ache Sits Increased

Bitcoin is at present buying and selling round $67,271, with max ache positioned at $70,000. Open curiosity exhibits 19,412 name contracts and 11,044 put contracts. This provides a put-to-call ratio of 0.57 and displays an total upside bias. The whole notional quantity tied to the expiry is roughly $2.05 billion.

Bitcoin Expiring Choices. Supply: Deribit

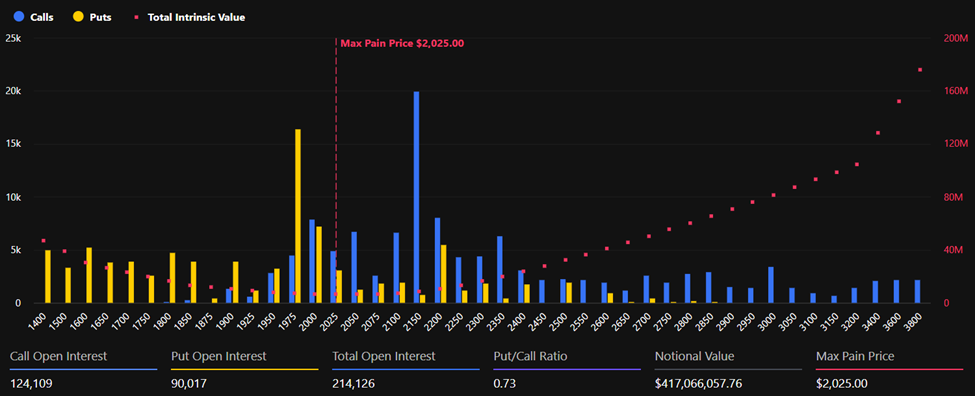

Ethereum mirrors that constructive tilt, although in a extra balanced vogue. ETH trades close to $1,948, with max ache at $2,025.

Calls (124,109 contracts) outnumber places (90,017), leading to a put-to-call ratio of 0.73 and a notional worth of roughly $417 million.

“…positioning skews call heavy across both assets, with BTC showing the stronger upside skew. Max pain levels sit below dominant call open interest in BTC, while ETH positioning is more balanced but still constructive,” analysts at Deribit famous.

Max ache refers back to the value at which the best variety of choices expire nugatory, minimizing payouts to consumers.

With each BTC and ETH buying and selling under their respective max ache ranges, value gravitation towards these strikes into expiry might scale back losses for possibility sellers.

The $40,000 Put: A Tail-Danger Sign

Regardless of the headline bullish skew, a large focus of places on the $40,000 strike has caught market consideration.

The $40,000 Bitcoin put is now the second-largest strike by open curiosity, representing roughly $490 million in notional worth. This comes after Bitcoin’s sharp retracement from prior highs, which reshaped hedging demand throughout the board.

“While aggregate positioning into expiry skews call heavy, one strike stands out: The $40K BTC put remains among the largest open interest strikes ahead of February expiry. Deep OTM downside protection demand remains visible on the board, even as headline put/call ratios lean constructive,” Deribit analysts indicated, highlighting the weird measurement of the place.

In brief, merchants could also be positioned for upside, however they’re unwilling to rule out one other volatility shock.

Hedging, Premium, and Structural Implications

The dynamic suggests a broader change in Bitcoin’s derivatives market. Choices are more and more used for directional bets, yield methods, and volatility administration.

Analyst Jeff Liang argued that extracting premium from the choices market might scale back structural promoting stress.

“If we can stably extract the premium from the options market and empower Bitcoin HODLers, it means: HODLers no longer need to sell their Bitcoin to improve their lives… Selling pressure on Bitcoin will reduce… This will further drive Bitcoin’s price upward,” he said.

The analyst described choices premium as a “localized pump” pushed by worry and greed, one which redistributes worth to long-term holders with out contradicting Bitcoin’s mounted provide cap.

Total, calls outweigh places throughout each BTC and ETH, signaling that merchants retain publicity to a rebound. But the sheer scale of deep out-of-the-money hedges reveals a market that continues to be cautious.

With billions in notional worth set to run out, the important thing query is whether or not costs drift towards max ache—or whether or not hidden crash-protection demand proves prescient, reigniting volatility simply as merchants count on calm.

Airdrop Exploited by a Sybil Assault?")