Picture supply: Getty Photos

The FTSE 250 index of mid-cap shares has risen 5% in worth in 2025. That’s not dangerous, however it’s under the efficiency of different main world indexes. The FTSE 100 as an example is up 12% over the interval.

This underperformance displays a bleak outlook for the UK financial system, together with growing pessimism over rate of interest cuts as inflation rises. Roughly 40%-45% of the FTSE 250‘s earnings come from Britain, far increased than the internationally flavoured Footsie.

A few of the index’s fine quality constituents have truly fallen sharply since 1 January, which I consider represents a possible dip-buying alternative. Listed below are two such shares I feel demand critical consideration right now.

Bloomsbury Publishing

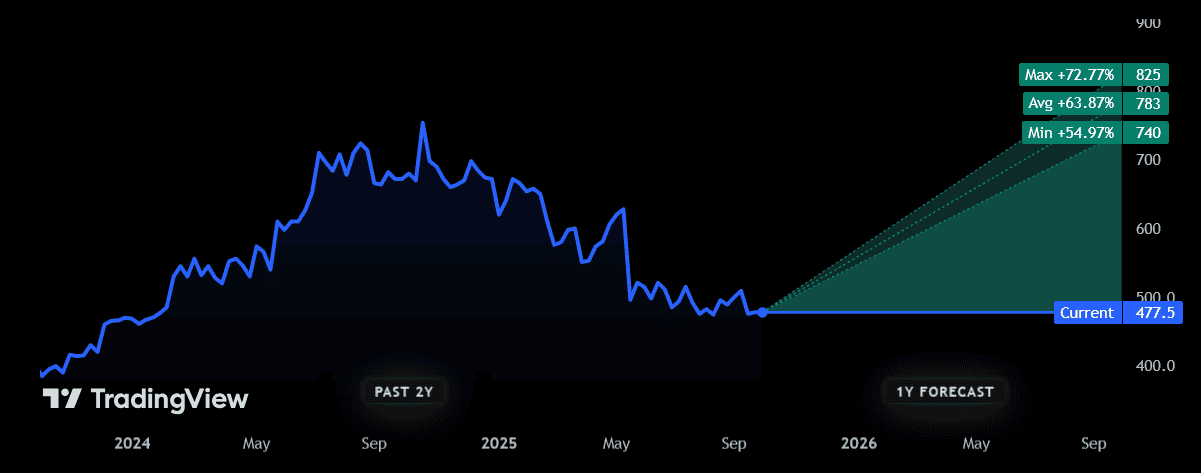

Bloomsbury Publishing‘s (LSE:BMY) shares have dived 29% within the 12 months to this point. Whereas its Harry Potter franchise stays as fashionable as ever, weak spot in different components of the enterprise has pulled the guide producer sharply decrease.

Extra particularly, poor gross sales at its educational publishing division have taken the shine off the agency’s different operations. Natural gross sales right here dropped 10% within the final monetary 12 months, it introduced in Could, due partially to budgetary pressures within the UK and US. The corporate’s didn’t recuperate floor since then.

Whereas these troubles might persist, I feel there’s loads to love at Bloomsbury that makes it price a detailed look. The long-term outlook for its educational publishing unit remians sturdy, helped by its gamechanging acquisition of high-margin operator Rowan & Littlefield.

However what actually attracts me in is the standard of its shopper division, and extra particularly its pedigree within the fast-growing fantasy and sci-fi fiction markets. Harry Potter isn’t the one star sequence in its portfolio — Sarah J Maas’s A Court docket of Thorns and Roses is one other one in every of its bestselling sequence, with 75m gross sales and extra books contracted to return down the pipeline.

Supply: TradingView

Supply: TradingView

Metropolis analysts are united of their view that Bloomsbury shares will rebound over the subsequent 12 months. The consensus view is for a 64% rise from present ranges, to 783p per share.

Ibstock

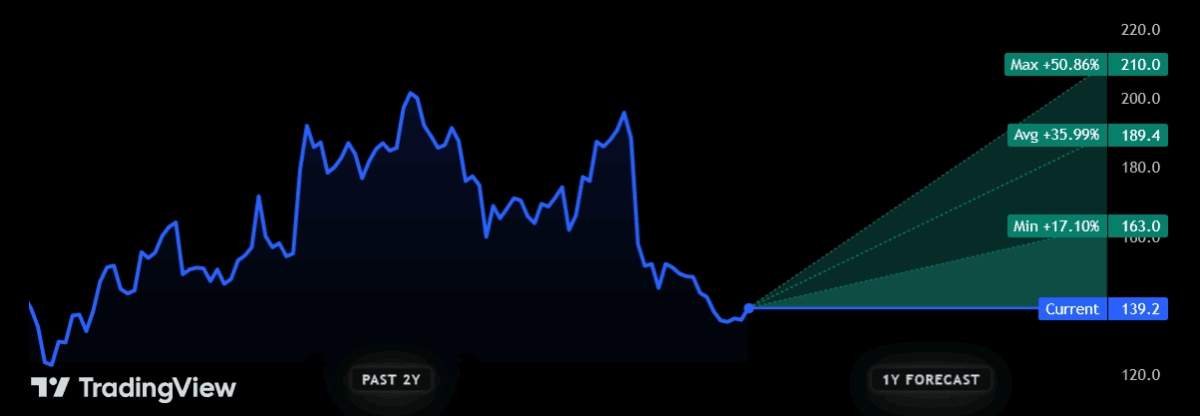

Ibstock‘s (LSE:IBST) share price has dropped 21% since 1 January. It’s fallen on fears that the latest housing market restoration might be flagging because the UK financial system struggles and inflation rises.

For long-term traders, nevertheless, I feel the brick producer’s funding case stays a sturdy one. It’s why I maintain the corporate in my very own Shares and Shares ISA.

Regardless of excessive competitors, the calls for of a rising inhabitants may supercharge product gross sales over the subsequent decade. The federal government plans to construct 3m new properties to 2029 alone. Properly, Ibstock’s invested closely in capability to satisfy future demand.

However that’s not all that’s attracted me, as I feel the corporate may also count on sturdy off-take from the restore, upkeep and enchancment (RMI) sector. The UK housing inventory is likely one of the oldest on the planet, so there ought to be regular demand right here for years to return.

Supply: TradingView

Supply: TradingView

As with Bloomsbury, Metropolis brokers are united of their perception Ibstock shares will rebound over the subsequent 12 months. The typical share value goal amongst them is 189.4p, representing a 36% premium from right now’s ranges.