Picture supply: Getty Pictures

The time to take a look at shopping for shares is once they’re low-cost. And Gamma Communications (LSE:GAMA) inventory is at a five-year low proper now.

The agency’s replace from Tuesday (24 March) isn’t robust. However there are causes to suppose the long run seems to be a lot brighter.

Development(?)

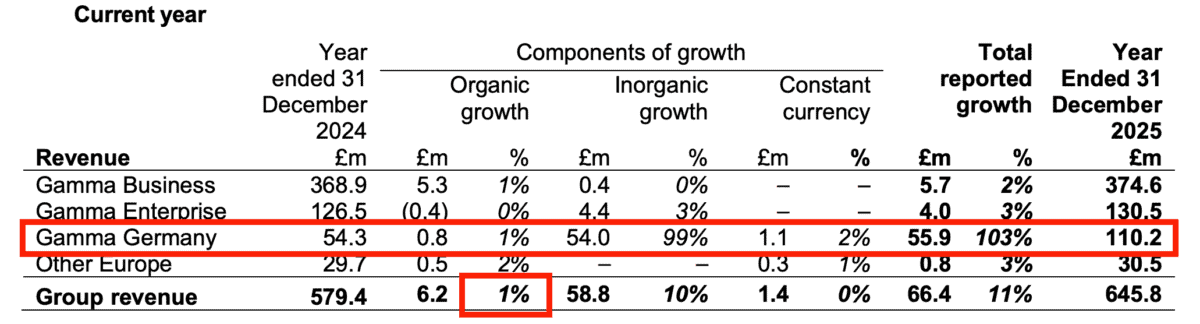

Gamma’s outcomes are sophisticated. The headline variety of 11% income development is robust, however there’s extra to it than this.

The vast majority of the rise is from current acquisitions in Germany. And this received’t be repeated going ahead.

The acquired companies are doing nicely, attaining 10% natural development. However they’re solely a small a part of the general firm.

Supply: Gamma Communications Full 12 months 2025 RNS

In consequence, probably the most significant gross sales development quantity might be between 2% and three%. And that’s a lot decrease.

The UK a part of the corporate is dealing with huge challenges. The copper community swap off is weighing on revenues and rising prices.

That’s why the inventory fell 10% after the agency’s outcomes. However whereas the outlook for 2026 isn’t significantly better, one thing huge might be on the best way.

Up to some extent, Lord Copper

The UK switching off its copper cellphone community on the finish of this 12 months is each good and dangerous for Gamma. However I feel it’s extra good than dangerous.

Within the quick time period, it means the tip of enterprise line rental and broadband providers the agency has offered for years. That’s dangerous for gross sales. On the identical time, Openreach is rising line rental costs for remaining prospects. That additionally threatens the agency’s margins.

Ultimately, although, corporations are going to have to maneuver their cellphone providers to the cloud. And Gamma is the UK chief on this.

The vast majority of small companies nonetheless want to modify over. Meaning the potential alternative forward is a considerable one. Firms typically don’t change their suppliers fairly often. So the advantages of profitable new prospects may final for many years.

Competitors

There’s an enormous change coming and Gamma may nicely be set to learn. However the firm received’t have issues all its personal manner.

The large danger is that the agency has to compete with some a lot bigger operators. An apparent one is Microsoft. By way of competing for cloud prospects, Gamma can’t match Microsoft’s scale. But it surely does have some benefits of its personal.

The obvious is that it’s capable of provide higher buyer assist. This comes with having a longtime community of channel companions. It’s additionally the results of proudly owning the infrastructure. Meaning it may possibly provide the flexibility to intervene to repair issues in ways in which Microsoft can’t.

For small companies that depend on cellphone numbers working, this might be vastly necessary. And that’s why the swap is a chance for Gamma.

Time to purchase?

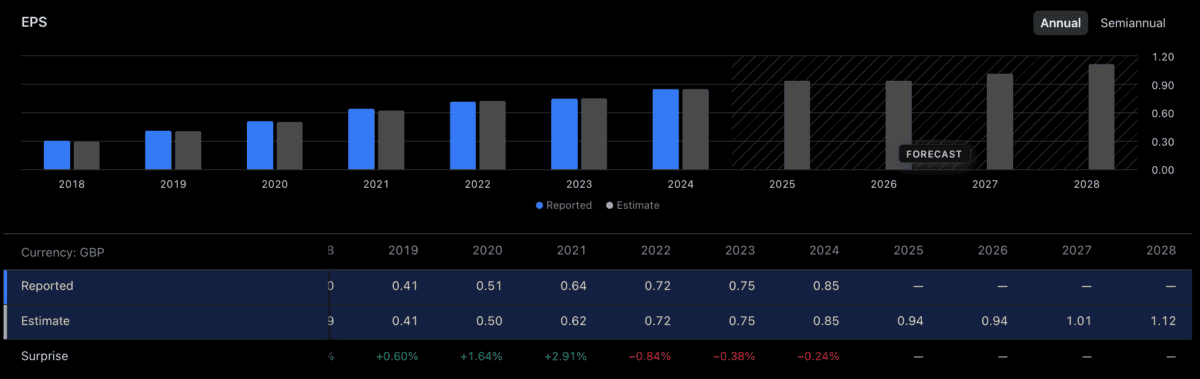

The inventory is at a five-year low and buying and selling at a price-to-earnings (P/E) ratio of eight. That’s additionally unusually low for the corporate.

In consequence, £1,000 is sufficient to purchase 128 shares. And that’s what I’m planning on doing once I’m subsequent able to speculate.

Analysts aren’t anticipating something in the best way of development for 2026. However they’re extra optimistic additional forward.

That matches with the best way I see issues unfolding for the corporate. And that’s why I see the decrease share value as a chance to think about.